Dear Reader, The U.S. Government has become one of the most active stock investors in the market.

In less than nine months, its new portfolio is up 278% That's 26 times better than the S&P 500.

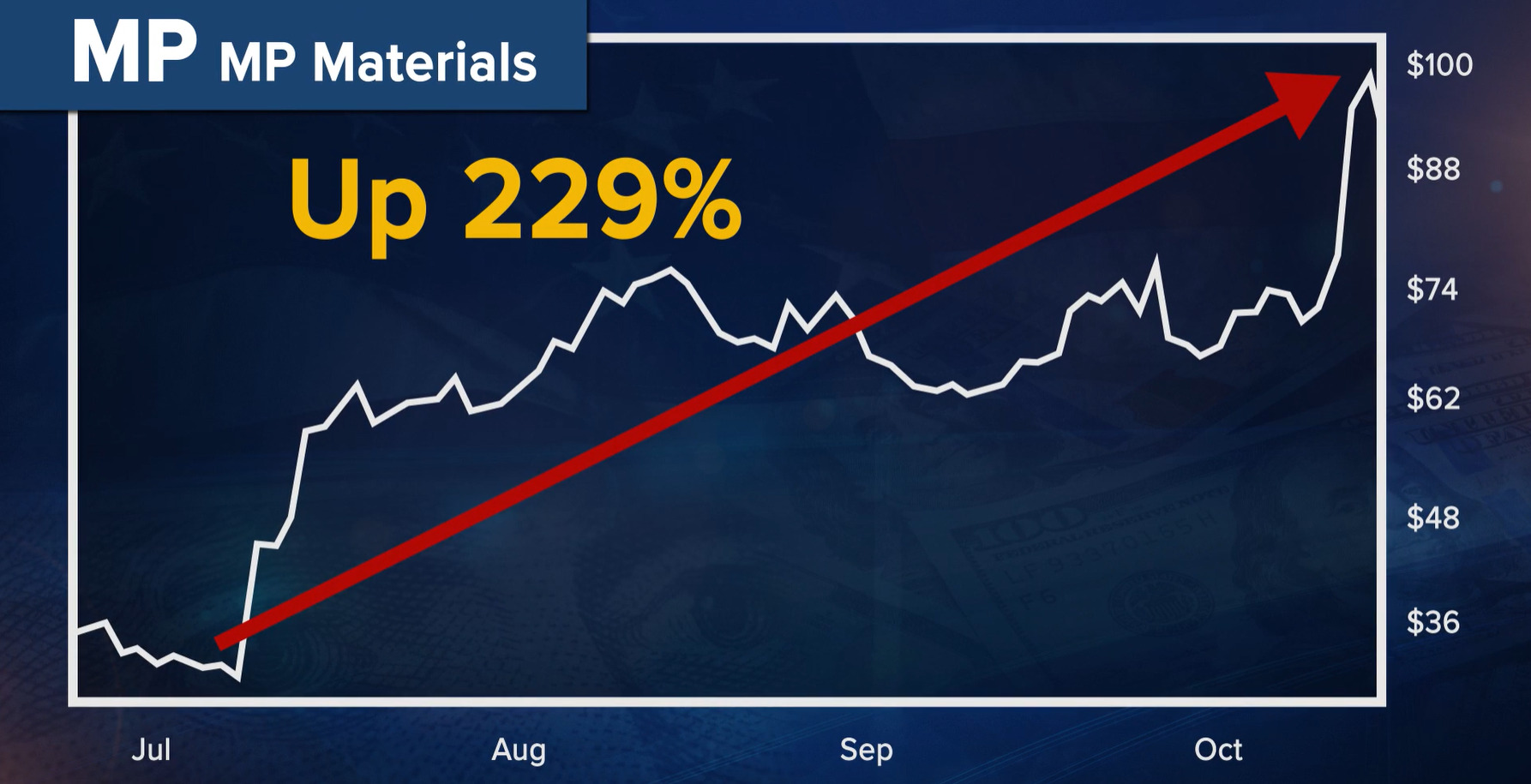

It started with MP Materials. The stock rose 229% after the government bought in.

Then came Intel, which went up 131%.

Lithium Americas jumped 227%.

Trilogy Metals soared 407%. And USA Rare Earth rose 62% in a single day. Every time the government buys a stock, the price goes up fast. This is not luck. It is a clear pattern that keeps repeating. I've studied every move the government has made. After months of research, I believe I've found the next company Uncle Sam is likely to buy. The window to get in early is closing quickly. Click here to see the company I believe is next. Sincerely,

Michael Robinson

Weiss Ratings Tech Investing Strategist

Today's Featured Content

3 Dividend Kings That Earn Their Crown Every QuarterAuthored by Chris Markoch. Article Posted: 5/31/2026.

Key Points

- Johnson & Johnson, PepsiCo, and Becton Dickinson have each raised dividends for more than 50 consecutive years.

- These Dividend Kings combine recession-resistant business models with long-term income growth and strong financial fundamentals.

- Investors seeking reliable dividend growth stocks may find attractive opportunities in healthcare and consumer staples leaders.

- Special Report: Better than SpaceX? Grab this ticker instead.

The Dividend Kings—companies that have raised their dividend for at least 50 consecutive years—represent one of the most exclusive clubs in investing. The entry requirement is a testament to financial discipline. A company must maintain uninterrupted dividend growth through recessions, market crashes, interest-rate cycles, and industry disruption. Fewer than 60 U.S. companies held the title as of 2026. But holding the title alone doesn't make a stock worth owning. Some Kings are slow-growth businesses propped up by yields that have risen mainly because the share price has fallen. The three below are different. Each carries the pedigree and the fundamentals to back it up. The Healthcare Dividend King With a Stronger Post-Spinoff Business

Johnson & Johnson (NYSE: JNJ) has increased its dividend for 64 consecutive years—a track record that stretches back to the early 1960s and has survived oil shocks, the dot-com crash, the financial crisis, and a global pandemic. But what makes JNJ particularly compelling today is the transformation of its business. In 2023, J&J completed the spinoff of its consumer products division into a separate, publicly traded company called Kenvue (NYSE: KVUE), which houses brands such as Tylenol, Band-Aid, and Listerine. The move was controversial at the time, but the strategic logic has played out. The remaining J&J is now a pure-play pharmaceutical and MedTech company. That means the company now has a higher-margin business with a pipeline that management has supported with aggressive R&D investment. The legacy consumer division, while stable, was holding back the multiple. Without it, investors get direct exposure to J&J's oncology, immunology, and neuroscience pipelines. The stock is up approximately 50% over the past year, reflecting the market's belated recognition that the business is fundamentally stronger post-spinoff. The dividend yield sits around 2.3%, modest by Dividend King standards, but it is paired with a balance sheet that is one of only a handful in the S&P 500 to carry a AAA credit rating. For investors who want income growth backed by genuine business quality rather than financial engineering, J&J is the benchmark. The Consumer Staples Giant Built for Long-Term Income GrowthPepsiCo (NASDAQ: PEP) is one of those companies that perpetually underwhelms in bull markets and quietly outperforms over full market cycles. It has raised its dividend for 54 consecutive years and carries one of the most recognizable brand portfolios in the world, including Pepsi, Gatorade, Lay's, Doritos, Quaker, and Tropicana. More than 20 individual brands generate over $1 billion in annual sales each. The underappreciated part of the PepsiCo story is how that diversification functions as a hedge. When beverage volume softens, snack volumes hold up. When North American consumers tighten spending, international growth picks up the slack. The company has demonstrated the ability to push through price increases without devastating volume, a form of real pricing power that not every packaged food company can claim. Organic revenue growth of 1% to 3% per quarter may not sound exciting, but it has stayed remarkably consistent across economic environments while compounding meaningfully over the past decade. The dividend yield is currently around 3.9%, with a recent 4% dividend increase. That extends the company’s multi-decade track record of delivering above-inflation income growth. PepsiCo is not a stock that will make a portfolio double in two years. But it can quietly build wealth over a decade through dividends reinvested, earnings growth, and the kind of durability that makes it a reliable ballast when growth stocks are being repriced. For investors nearing or in retirement, or for anyone who wants income that genuinely grows in purchasing power, PEP belongs in the conversation. The Overlooked Medical Technology Dividend KingBecton, Dickinson and Co. (NYSE: BDX) is the Dividend King that isn’t a household name for most income investors. The company manufactures needles, syringes, infusion systems, diagnostic instruments, and lab automation equipment that hospitals and clinics continuously buy, regardless of the economic environment. That defensive revenue profile creates a firm foundation, but BDX also has a credible growth story layered on top. The company is investing heavily in its diagnostics and medication management businesses, both of which benefit from secular trends in hospital efficiency and infection control. Management has guided for low-single-digit revenue growth in fiscal 2026 and earnings per share of $14.75 to $15.05 at the midpoint, representing modest but steady earnings growth. With a dividend yield of 2.8% that currently sits above the S&P 500 average, 53 years of uninterrupted dividend growth, and a business model that is genuinely recession-resistant, BDX offers something increasingly rare: income that doesn't come with meaningful existential business risk. It is the kind of holding that long-term investors look back on a decade later and wish they had bought more of at prices like these.

. |

Tidak ada komentar:

Posting Komentar