Dear Reader, Last year I ran for Mayor of New York City. And lost to a 34-year-old Democratic Socialist. Now I'm convinced what's starting in New York will spread across America. Just for starters:

- The new mayor wants to spend $70 million of taxpayer money just to study whether government-run grocery stores are a good idea.

- He's threatening a 9.5% property tax hike on every homeowner in the city.

- And he wants to raise taxes on every corporation and high earner.

This isn't just a New York story. Nearly 40% of Americans now have a "positive" view of socialism. But what nobody's talking about is WHY this is happening... and where it's all headed. I have my MBA from Harvard and spend my time in correspondence with billionaires like Warren Buffett and Bill Ackman. I've spent 30 years on Wall Street. And there's a specific term for what's unfolding in America right now... one that points to an economic event unlike anything we've seen in over 100 years. I'm not running for office again. But if you care about your wealth, your family, and your future, you need to understand what's really coming. I've put together a free analysis explaining exactly what I see, and the specific steps I recommend you take with your money today. I strongly encourage you to check it out here. Regards, Whitney Tilson

Editor, Stansberry Investment Advisory

Former Hedge Fund Manager

Co-Founder, Teach for America

Harvard MBA P.S. What's happening today will reset the financial system in a way most of us can't imagine. If I'm even half right, it's going to have a huge impact on your money and your future. Get the details here...

Thursday's Featured Content

Okta’s AI Moment May Be Bigger Than Investors RealizeAuthored by Thomas Hughes. First Published: 6/16/2026.

Key Points

- Okta's fiscal Q1 2027 results showed revenue of $765 million, growing 11.2% year-over-year, driven largely by rising agentic AI demand.

- OKTA shares surged more than 30% following the earnings release, reaching a four-year high, with analyst consensus price targets rising 18%.

- Institutions own more than 85% of Okta shares and shifted from distribution to accumulation in Q2, while the company's debt-free balance sheet supports ongoing share buybacks.

- Special Report: Understanding what Trump just did

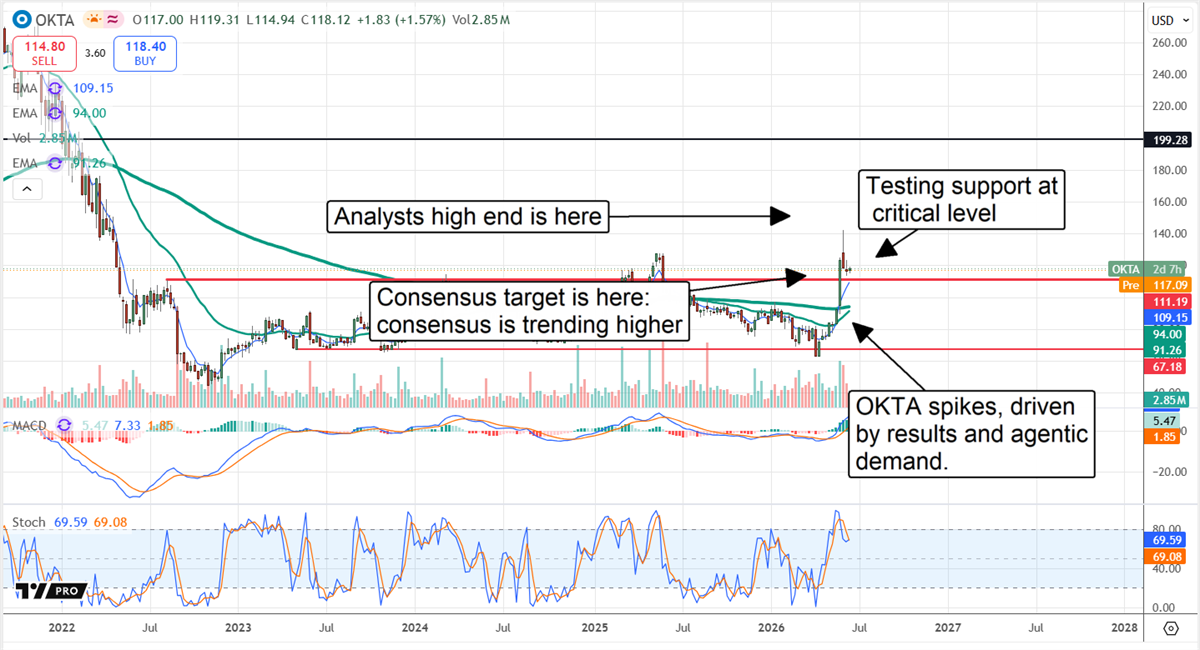

Okta’s (NASDAQ: OKTA) fiscal Q1 2027 earnings report changed the narrative. It showed that the company’s strength and cash flow are being driven by AI-related demand. While AI is disrupting SaaS stocks, the disruption is proving favorable, contrary to expectations, with cybersecurity at the forefront. The need is simple: AI must be secure at every level. Without security, AI is untrustworthy at best and dangerous at worst, and Okta is central to securing the global tech ecosystem. Okta’s cloud-native, vendor-neutral approach to identity security means no vendor lock-in and the largest, broadest addressable market among its peers. The system also integrates seamlessly, has nearly 100% uptime, and offers easy-to-use features that support single sign-on for employees and instant on- and off-boarding for HR teams.

The takeaway is that organizations and enterprises that need to secure identities and access, including agentic AI, can do so with Okta regardless of which vendor provides the technology being secured. Regarding agentic AI, it drives an exponential increase in access requests, which in turn drives demand for Okta’s services. Okta’s AI-Driven Price Spike Supported by AnalystsOkta’s price spike itself is telling. The market surged by more than 30% in the week of the release, indicating robust support at a cluster of moving averages. That cluster is significant, suggesting a market with aligned forces and a solid floor in price action. OKTA’s price has broken to a 12-month high and is now at a four-year high, indicating shifting market dynamics and a high probability of a market reversal. As of mid-June, profit-taking has capped gains, but support remains at the high end of the previous range, setting the stage for another rally this summer.

Analyst trends are also central to the stock price outlook, and they strengthened following the Q1 release. MarketBeat tracked 25 revisions in the first week, and all but four were price target increases. Three of the four outliers were reaffirmed targets, aligning with a forecast for consensus-or-better pricing, while the lone downgrade was offset by a price target increase to an above-consensus level. The critical takeaway from the analyst data is that the consensus of fresh targets is just over $118, an 18% increase from the pre-release level, including the new high target of $150. The $118 consensus implies modest upside relative to the critical support target, while the $150 high suggests that another multiyear high could be set. In this scenario, the consensus trend supports price action, while the high end leads the market. Assuming upcoming releases extend the trends revealed in Q1, analysts' price target forecasts will likely continue to strengthen and lead this market higher. Institutional data suggest downside risk is limited this summer. The group owns more than 85% of the stock, providing a solid support base, and it shifted from distribution in Q1 to accumulation in Q2. The shift aligns with the April stock price bottom, reinforcing it as a support target and contributing to the May and June advance. The likely outcome is that this group maintains its bullish posture in 2026, potentially accelerating accumulation as subsequent reports are released. Okta Builds Momentum in Q1: Raises Guidance, but Guidance Remains CautiousOkta had a solid quarter in Q1, with revenue of $765 million, up 11.2% year over year and slightly ahead of MarketBeat’s reported consensus. Strength was driven by agentic demand and reinforced by forward-looking metrics that suggest acceleration in upcoming quarters. Remaining performance obligation, a measure of contracted business, grew by 16%, suggesting the Q2 and full-year guidance updates were cautious. Management expects growth to continue and remain above consensus, but only 9% in the current quarter and 9.5% for the year. Margins and earnings were also strong. The company managed costs and spending well, resulting in adjusted earnings growth that exceeded forecasts by more than 600 basis points. More importantly, strong earnings and cash flow bolster the capital return outlook through aggressive share buybacks. Q1 activity reduced the share count by more than 2.2% on average, providing investors with significant leverage; the Q1 results and cash flow suggest the pace will continue in upcoming quarters and may accelerate. Okta’s balance sheet shows no red flags in 2026. The company operates without debt, has ample cash, and offers value for investors. Q1 highlights include increased cash and equivalents, reduced liabilities, and steady equity despite reinvestment and buybacks. Looking ahead, cash flow and free cash flow should continue to support growth and capital returns while maintaining fortress-like balance sheet metrics.

This ad is sent on behalf of Stansberry Research, 1125 N Charles St, Baltimore, MD 21201. If you would like to optout from receiving offers from Stansberry Research please click here.

. |

Tidak ada komentar:

Posting Komentar