Editor's Note: Please see the following from Dr. David Eifrig, a former Goldman Sachs Vice President and professional trader. He has just released an urgent investigative exposé on the $7.2 Trillion "Mar-a-Lago Trade" -- an idea Bloomberg has said may cause "a dire shift of fortunes for America."

Shopify Delivers Strong Q2 Results as Revenue and Profit Rocket

Posted On Aug 05, 2026 by Ian Cooper

Shopify (NASDAQ: SHOP)just posted an impressive second quarter, posting strong growth in both revenue and profit as more businesses continued to use its e-commerce platform. The company exceeded Wall Street expectations, driven by higher sales across its subscription services and merchant solutions business.

Table of Contents

During the second quarter, SHOP’s net income came in at $1.5 billion, or $1.16 per share. That’s a significant increase from $906 million, or 69 cents per share, during the same period last year. Adjusted for one-time expenses, the company reported earnings of 42 cents per share. Analysts expected adjusted earnings of 40 cents per share.

Revenue also came in higher than forecast. Total revenue reached $3.58 billion, up from $2.68 billion a year earlier. Analysts had predicted revenue would reach about $3.45 billion, making Shopify’s results another positive surprise.

The company’s growth was fueled by strong performances in both of its primary business segments: Subscription Solutions and Merchant Solutions.

Subscription Solutions, which includes monthly plans and software tools that businesses use to operate their online stores, generated $802 million in revenue during the quarter. That’s solid growth compared with $656 million in the same quarter last year.

Even stronger was Merchant Solutions, Shopify’s largest source of revenue. This division includes payment processing, shipping services, financing, and other tools that help merchants manage their businesses. Revenue from Merchant Solutions climbed to $2.78 billion, up from $2.02 billion a year earlier.

Another important measure of the company’s success is Gross Merchandise Volume (GMV), which jumped to $115.57 billion during the second quarter, compared with $87.84 billion year over year. The increase in GMV indicates that consumers continued spending through Shopify-powered stores despite ongoing economic uncertainty.

Investors also received encouraging guidance for the months ahead.

SHOP expects revenue in the third quarter to grow at a low-thirties percentage rate compared with the same period last year. The company also expects gross profit dollars to increase at a mid-to-high twenties percentage rate, suggesting management remains confident about continued demand.

At the same time, the company plans to keep operating expenses under control. The company expects operating expenses to represent between 33% and 34% of revenue during the third quarter. Maintaining disciplined spending while growing revenue could help support continued profitability.

Building a Broader E-Commerce Platform

In addition, Shopify has spent the past several years expanding beyond its original online storefront business. Today, the company offers payment processing, fulfillment tools, financing options, marketing features, and other services designed to help merchants manage every aspect of their businesses from a single platform.

That strategy appears to be paying off. As merchants adopt more Shopify products, the company generates additional recurring revenue while strengthening customer loyalty.

The latest results also demonstrate SHOP’s ability to outperform market expectations. Beating analyst forecasts on both earnings and revenue is often viewed positively by investors because it signals stronger-than-expected business performance.

Bottom Line for Shopify

With revenue climbing more than $900 million year over year, profit rising sharply, and merchandise sales reaching record levels, Shopify has considerable momentum. If the company delivers on its third-quarter outlook, it could continue rocketing even higher.

Overall, Shopify’s continued growth in online commerce, increasing merchant activity, and greater adoption of its expanding suite of business services make the stock even more attractive. Strong financial results, healthy sales growth, and optimistic guidance suggest the company remains well-positioned for the remainder of the year.

Today’s editorial pick for you

If You Want to Buy AMD Stock, You’ll Statistically Do Better by Waiting

Posted On Jul 31, 2026 by Joshua Enomoto

Since this is the internet, I need to be explicit about this Advanced Micro Devices (NASDAQ: AMD) story: I am not making a permabear argument. With artificial intelligence rapidly becoming our flagship technology, AMD stock over the long run should be a strong investment. However, in the near term, especially for those trading AMD options, a cautionary approach is best.

Table of Contents

Sure, I’m coming late to the game. On Wednesday, AMD stock dropped 5.51%. In the trailing five sessions, the ticker has sank more than 21%. If you look at the situation from the perspective of technical analysis, you can’t help but notice that the security has fallen off a sideways consolidation channel. With sellers apparently panicking, the fallout could get ugly.

I would also venture to say that the consensus among retail traders is to let the selloff fully die out before engaging. I’m not going to put too much faith in my chart-interpreting abilities but Advanced Micro Devices stock does look like a falling-knife scenario. But what’s fascinating is that the market may have already provided a clue as to our current juncture.

Back in early July, I discussed the trading narrative for AMD rival NVIDIA (NASDAQ: NVDA). Specifically, I mentioned that I was intrigued by the 205/210 bull call spread expiring Aug. 7. Now, unless a miracle happens, this trade will almost certainly get blown up (in a bad way). But keep in mind that up until the close of July 22, this trade was very much in the money.

Just as importantly, take a look at the Markov simulator that I provided in that article. Because NVDA stock was projected to decline in performance in the fifth week following the flashing of the underlying quantitative signal, I chose the Aug. 7 expiration date to cut off my exposure. Unfortunately, reality pushed up projected events to week 3 — but the key takeaway is that the downturn did eventually come.

Larry Benedict — who beat the S&P 500 by 18X in 2025 and made clients $95M during the 2008 crisis — says Trump installing a new Fed chair is triggering the most significant shift in U.S. markets in nearly 20 years.

Readers had chances at 62% in 2020, 117% under a month in 2022, 89% in 17 days after Jackson Hole. One ticker at the center.

For AMD Stock, It’s Not About Storytelling but Data

Generally, it’s understood that you can’t precisely predict future market behaviors. For decades, if not centuries, analysts have attempted to scour financial prints, technical charts and more recently, quantitative models to predict where a target security may head next. In arguably most cases, these efforts are nothing more than marketing BS.

However, that doesn’t mean we should give up on the idea of probabilistic forecasting. Just like in the NVIDIA case above, I can’t tell you exactly where AMD stock is going to land with absolute certainty. If I did, I certainly wouldn’t share it with anyone. Instead, I would simply trade this proprietary intelligence and basically print my own money.

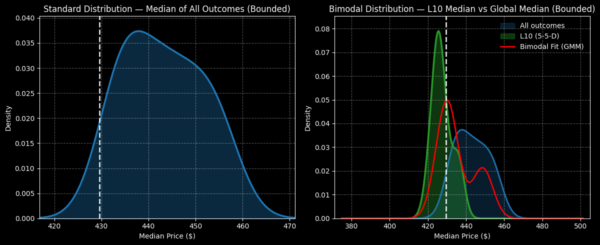

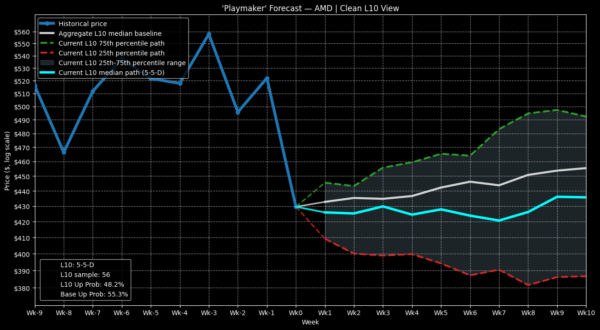

I don’t know where exactly Advanced Micro Devices stock will end up. No one does. But I can tell you — thanks to my Markov simulator — where AMD has historically ended up given specific quantitative conditions.

With NVIDIA, the ticker printed four up weeks over the past 10 weeks, leading to a downward slope. Under this 4-6-D sequence, the next five weeks typically resulted in upside, with the next five weeks usually seeing choppy pessimism. Of course, the laws of nature are not guaranteed to repeat, but the above scenario has been the median response.

Let’s consider AMD stock. In the past 10 weeks, the ticker has witnessed a 50/50 split between positive and negative sessions; however, the overall slope has been negative. Under this 5-5-D sequence, the statistical expectation is for the median share price to gradually decline to the end of week 7. Then, over the next three weeks, shares tend to pop higher.

Still, the lift would be considered modest relative to how AMD stock usually performs as an aggregate expectation. In other words, if you were bullish on Advanced Micro, you’d be better off waiting as the expected performance under the signal is likely going to be worse than the performance under a random hold.

Don’t Believe Me? Check Out the Volatility Skew

It’s not just the historical data that is clouding the case for Advanced Micro Devices stock; rather, it’s the current hedging behavior among smart money traders.

Take a look at the volatility skew for Sep. 18 options chain. Here, the implied volatility (IV) — or the expectation of market movement — for far out-the-money (OTM) puts stands at an astronomical 1,000%. On the other end of the scale, the IV for far OTM calls is only 88.48%. In laymen’s terms, options traders are heavily prioritizing downside protection over upside convexity.

Granted, no one who studies options-based transactions is surprised by the stark picture in the volatility surface. As I mentioned at the top of this article, AMD stock has suffered heavy losses in recent sessions. If the smart money felt that this was a discounted opportunity, you’d likely see call IV elevated. After all, if most folks are selling, this would be a cheap time to buy in volatility terms.

However, the smart money doesn’t view AMD stock as a discount — they view it as a falling knife that is liable to lacerate unsuspecting bulls who do not look at the data. And that’s the overarching point here. I don’t know jack about the markets, seriously. But what I do know are numbers.

Look, I’m not saying be near-term bearish on Advanced Micro Devices stock because that’s how I interpret the charts. I personally don’t know where AMD is going to go. I’m just saying the data, under the specific condition that I outlined, tends to demonstrate negative performance before a turnaround occurs.

If you want to heed the warning, great. If you have an alternative model that suggests differently, use that instead. I’m just showing you the cards that I’m working with and why I believe what I believe.

How Should We Approach Advanced Micro Devices Stock?

From a conservative standpoint, the takeaway from the above data and inductive analysis is to wait until a little after mid-September to reengage AMD stock. Of course, nobody knows exactly how circumstances will pan out. But based on prior trends, that would be the forecasted time period when AMD may start looking interesting for the bulls again.

For those who actively want to speculate, you may consider the 430/420 bear put spread expiring Sep. 18. No, it’s not the most exciting trade because the maximum payout for AMD stock falling through the $420 strike at expiration is only around 53%. Plus, the net debit per spread is a pricey $655. That’s a direct consequence of the hedging activity that has made put options very expensive.

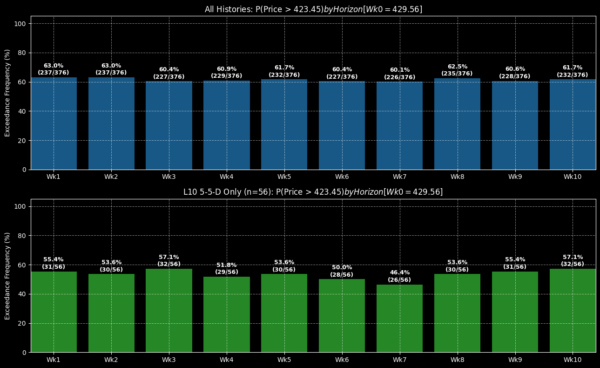

However, what’s enticing here is the breakeven price of $423.45. Right now, Wall Street assigns a probability of profit of 48%. However, the actual odds could be a little bit higher.

Since January 2019, the 5-5-D sequence has flashed 56 times on a rolling basis. Of this count, there have been 26 instances where AMD stock has ended up above the $423.45 breakeven price at week 7 (Sep. 18), meaning that there have been 30 cases where AMD slipped below this threshold. As such, the conditional probability of profit could be 53.6%, not 48%.

Granted, that’s not much of a difference relative to Wall Street’s odds. But you also have to consider that being bearish on Advanced Micro Devices stock is no longer the contrarian wager — it’s the expected outcome. So, the bottom line is, if you’re going to be bearish, be prepared to pay. Otherwise, if you’re looking for a discount, you statistically stand a better chance of waiting.

It shows you when the biggest stock jumps could occur – to the DAY – with 83% backtested accuracy.

If you feel you've received this email in error, please click here to unsubscribe from the TradeSmith Daily, as well as marketing communication from TradeSmith.

As a member of the TradeSmith Daily, you will receive critical market analysis every day from the TradeSmith team. Be sure to whitelist services@exct.tradesmith.com and info@exct.tradesmith.com to ensure you don't miss any updates.

Apple, Amazon, Google, Meta, Microsoft, Nvidia, Tesla

For example, want to see the EXACT DAY Tesla could soar this year?

100% of the time, Tesla has a history of soaring on one particular date – bull or bear market – at a rate fast enough to triple your money over a year if you found trades of this caliber again and again.

TradeSmith is not registered as an investment adviser and operates under the publishers’ exemption of the Investment Advisers Act of 1940. The investments and strategies discussed in TradeSmith’s content do not constitute personalized investment advice. Any trading or investment decisions you take are in reliance on your own analysis and judgment and not in reliance on TradeSmith. There are risks inherent in investing and past investment performance is not indicative of future results.

To unsubscribe or change your email preferences, please click here.

TradeSmith | 1125 N. Charles Street, Baltimore, MD 21201

Price clears a level it's been fighting with for days.

The breakout looks clean.

You buy it…

Then price slides right back under, takes your stop, and keeps going the other way.

Most traders write that off as chop, or bad luck.

It's neither.

Think about the problem a fund has when it needs out of a large position.

Every share it sells has to be bought by somebody.

Sell into a thin market and price collapses against them the whole way down.

So they need thousands of retail orders stacked in one place at one time.

And the crowd makes that easy, because the crowd always stands in the same spots.

Stop orders from the shorts. Buy orders from the breakout traders. All piled within a few ticks of each other, just past the level everyone's watching.

That pile is the liquidity they need.

Price pushes through, the pile fills, the seller is gone… and then price slides back under.

Professional traders call it a liquidity grab.

Raghee Horner calls it a volume sweep, and it leaves a footprint on the chart every single time.

She's been trading for 37 years, profitable every single year, and has never blown out an account. Since December, she's added $366,000 to one swing account that started the year at $450,000.

*note: trading is hard, results not guaranteed and should not be expected to be replicated typically.

You'll see:

● How to tell a real breakout from a liquidity grab

● Why the free volume histogram on your chart can't answer the question that matters

● The updated toolkit built for today's faster, more volatile markets

● The 65% win rate and 5-to-1 average win-to-loss behind her 2026 results

Questions or concerns about our products? Contact support@ragingbull.com / 1-800-380-7072

DISCLAIMER: This entity is owned by RagingBull LLC (RB). Full disclaimer https://ragingbull.com/disclaimer/. We are a financial publisher, not a registered investment advisor. Our content is for informational purposes only and should not be considered personalized investment advice. All trading involves substantial risk of loss and you may lose some or all of your invested capital. Past performance does not guarantee future results.

*Sponsored content: This email may contain affiliate links, as identified by language such as “together with,” “In partnership with, “sponsored by,” etc. This means if you click their link, we may earn a commission at no extra cost to you. We are not responsible for any content hosted on third-party sites or your experience with third-party advertisers. It is the third party's responsibility to ensure compliance with applicable laws. We may hold positions in securities discussed and may trade without notice. We make no guarantees or warranties about what is advertised and have no fiduciary duty to subscribers. Always consult a qualified financial professional before making investment decisions.

P.S. The Trump administration has taken a direct stake in MP Materials, Lithium America, Trilogy Metals, and USA Rare Earth. Each time, shares sprinted higher.Click here to see why I believe this one is next.

Market Signal Report

Three buyouts, two biotech wins, and one Boeing deal worth watching tomorrow.

The S&P 500 came into Monday off its best week since April and spent the session giving a little back. Oil did the damage: crude pushed back above $80 after Iran attached new demands to reopening the Strait of Hormuz. Energy led the tape, REITs and utilities got sold.

Quiet day for data. That ends midweek when CPI and PPI hit. Here's the signal from today's session. 👇

📈 TODAY'S TOP 5 GAINERS

1 · BWMN +55% Bernhard Capital is taking Bowman Consulting private at $43/share in cash, a deal worth about $1B with debt.

2 · VREX +48% Teledyne agreed to buy Varex Imaging, the X-ray component maker, for $18.90/share. Roughly $1.1B, all cash.

3 · HZO +45% Blackstone's Safe Harbor is acquiring MarineMax for $53/share in a $1.5B all-cash deal.

4 · SLN +41% Silence Therapeutics' Phase 2 SANRECO trial hit its primary and secondary endpoints. Biotech data winners on real volume tend to stay on scanner watchlists for days.

5 · ABCL +36% AbCellera's mid-stage data showed its hot-flash drug ABCL635 beat placebo after a single dose.

🎯 THE SIGNAL Three of the five are all-cash buyouts. Deal stocks gap to the offer price and pin there. The entire trade happened in the opening minutes, and chasing a stock pinned at its deal price is collecting pennies with no upside left. The tradeable names on this list are the two biotechs, where price discovery is still happening.

🛢️ THE HEADLINE THAT MATTERED

Oil back above $80 as the Hormuz reopening stalls

Last week's rally leaned partly on hopes for a quick deal to reopen the strait. Iran's new conditions pushed crude up more than $2 on the session, and that single move explains most of Monday's tape: energy up nearly 3%, rate-sensitive sectors down, and indexes slipping off record highs.

It also raises the stakes for the inflation data coming midweek, because oil feeding into CPI is exactly what this market doesn't want to see right now.

👀 ONE TO WATCH TOMORROW

✈️ Archer Aviation (ACHR)

Archer is buying Boeing's electric aircraft unit Wisk Aero plus two subsidiaries, SkyGrid and Insitu, and Boeing is taking an equity stake in Archer. The stock opened up 20% and settled around +12% on heavy volume.

Why it's the watch: this is a real catalyst, not a press-release pump. Archer just absorbed autonomous flight technology and a defense-adjacent drone business while getting Boeing on its cap table.

Day two is the tell. If ACHR holds the gap and builds above Monday's range, that's institutions accumulating and the move can extend. If it fades back into the gap, the news is priced and the trade is over. Watch the open, watch the volume, and let the stock prove it first.

See you at the next signal. 📡

Market Signal Report powered by StocksToTrade

Signal over noise. Every trading day.

This message was sent as part of your Market Signal Report subscription. Market Signal Report is powered by StocksToTrade, and you are receiving it because you registered through StocksToTrade. If you did not request this email or believe it was sent in error, please reply directly so our team can review.

Subscription Status and Delivery Details Your subscription is confirmed and your delivery preferences are up to date. You are currently receiving content based on the schedule and frequency associated with your registration. If you need to adjust your delivery window, change your email frequency, or pause updates temporarily, reply to this message and our team will process your request within one business day. As a subscriber, your current access includes daily market briefings, top percentage mover watchlists, trade idea alerts, and periodic market research reports. These are delivered according to the preferences set at enrollment, and a confirmation of your original registration is available upon request.

A Note on Payments and Fraud Protection We will never ask you to provide payment card numbers, bank account details, or login credentials via email. Any message requesting this information should be considered fraudulent and reported to our team immediately. If you have a question about any purchase made through us, reply to this email within 30 days of the transaction date and a member of our team will provide your records.

How We Make Money Market Signal Report is free to read. We keep it that way by including paid advertisements and affiliate links in some emails. If you click a link or make a purchase, we may receive compensation from the advertiser at no cost to you. Sponsored placements never change our editorial views, and we only run offers we believe are relevant to traders and investors.

Managing Your Preferences You can unsubscribe at any time using the link at the bottom of this email, and it takes effect on the first click. If you would rather adjust what you receive instead of leaving entirely, reply to this message with the word PREFERENCES and our team will help you tailor your delivery.

Privacy and Data Handling We do not sell your personal information. Your email address is used to deliver the content you signed up for and to maintain your subscription records. For full details on how your data is collected, stored, and used, see the Privacy Policy linked below.

Reporting Suspicious Emails If you receive a message claiming to be from Market Signal Report or StocksToTrade that looks suspicious, do not click any links in it. Forward it to our support team so we can investigate and protect other readers.

Contacting Support Questions about your subscription or anything you read here? Reply to this email or write to contact@guardian.pub. Mail can be sent to Stable Financial Publishing, 1013 Centre Road Suite 403-D, Wilmington, DE 19805. We read every reply.

Content Disclaimer Market Signal Report is for informational and educational purposes only and is not investment advice, a recommendation, or an offer to buy or sell any security. Trading involves substantial risk of loss and is not suitable for everyone. Past performance does not guarantee future results. If you spot an error in anything we publish, reply and tell us — we correct mistakes promptly.

This email may contain paid advertisements and affiliate links. StocksToTrade may receive compensation if you click a link or make a purchase.