Have $500? Invest in Elon's AI Masterplan

Key Points

- Waste removal stocks often perform well in volatile times due to inelastic demand for services and long-term contract agreements.

- While the industry is highly-concentraded, the incumbents have unique advantages due to regulatory compliance hurdles.

- Waste Management, Republic Services, and Clean Harbors are three waste removal companies with upside in the current market environment.

- Special Report: Gold Shock Coming?

If you hate taking out the trash, welcome to an exclusive club called Everyone. Trash removal is always a consideration when renting or buying a new home because we all produce it and need it picked up in one form or another. And since demand for trash removal is inelastic, the companies that provide these services typically offer steady, if unspectacular, revenue. But the waste removal industry has a few other advantages that separate it from typical consumer staples companies:

- Regulatory and Environmental Burden - Removing trash from your home is usually a simple task, but removing it from businesses and governments is another animal altogether. The waste disposal industry is highly regulated, with strict standards and high barriers to entry. Opening a new landfill is a multi-year process, so incumbents operate as an oligopoly with massive pricing power.

- Long-term Revenue Streams - Waste removal companies typically operate on long-term contracts, which lock in consistent revenue that doesn’t dip during economic slowdowns. Businesses typically book waste removal contracts between one and three years in length, although longer terms of five to seven years are common for larger businesses and municipalities. Contracts can be flat- or variable-rate, and often include stipulations for regulatory fees and fuel charges (which are becoming increasingly important as oil prices soar).

This blend of essential demand and regulatory obstacles often makes for a solid defensive investment. Historically, waste management firms have performed well during market corrections and periods of volatility. With the Iran war ongoing and the S&P 500 near its 200-day moving average, fluctuations are likely to continue, making these waste service companies intriguing investment options at this time.

Our investment research analysts are going to be releasing their next investment idea tomorrow morning, around 10:00 AM Eastern time.

Add yourself to the distribution list here.

There are 90 paper gold claims for every real ounce in COMEX vaults. Ninety promises, one ounce of metal. It's like musical chairs with 90 players and one chair. COMEX gold inventory dropped 25 percent last year alone as gold flows East to Shanghai, Mumbai, and Moscow. On March 31st, contract holders can demand delivery. When similar situations arose in the past, markets closed and rules changed. Paper holders got crushed while mining stock holders made fortunes. One stock sits at the center of this crisis.

Get the full story on this opportunity now.

3 Steady Waste Removal Stocks With Upside

The industry’s oligopoly means only a handful of waste removal companies trade publicly on U.S. exchanges, limiting investment choices. With this context, let’s turn to three companies that offer an attractive combination of upside, consistency, and dividend income while also helping limit exposure to fluctuating fuel costs.

Waste Management: The Cashflow King

Waste Management Inc. (NYSE: WM) is the largest waste removal company in the U.S., both by market cap ($94 billion) and by number of landfills, transfer stations, and recycling facilities.

It’s also a very shareholder-friendly company, a trend that's likely to continue after reporting a strong free cash flow of $2.94 billion in Q4 2025.

Management expects additional free cash flow growth of more than 30% in 2026, and they're backing it up with a 14.5% dividend increase and $3 billion in share buybacks.

The company also remains insulated from the Strait of Hormuz crisis through energy surcharges, which pass diesel and compressed natural gas (CNG) price increases through to clients.

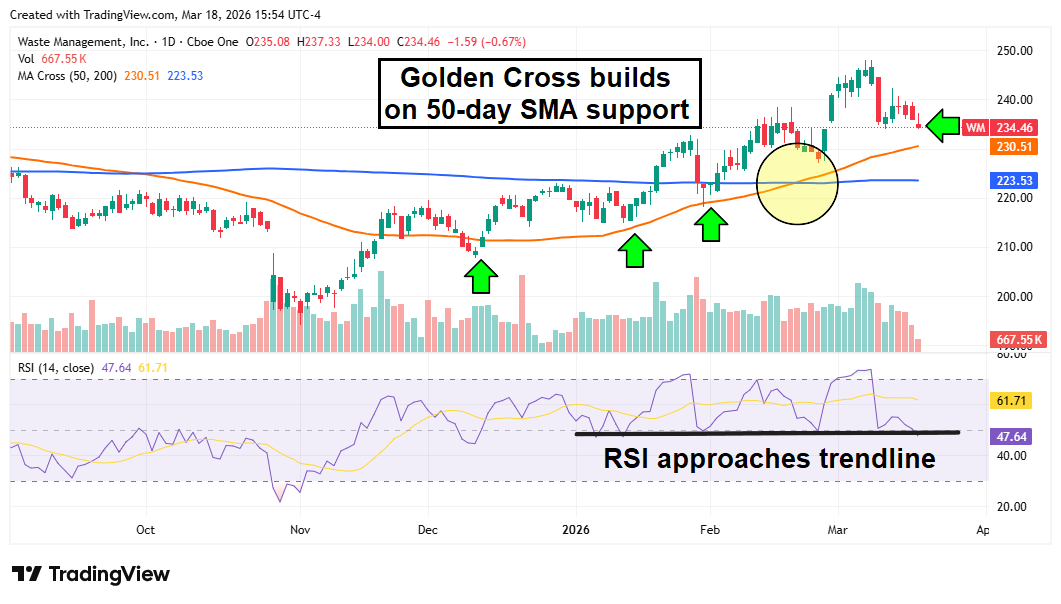

WM shares have the makings of a strong technical uptrend, with a bullish Golden Cross and healthy support at the 50-day moving average.

A trip into overbought territory on the Relative Strength Index (RSI) triggered a brief pullback, but now the share price is again approaching the 50-day moving average support level, which could be a good place to open a position for new buyers. The dividend also now yields 1.62%, with a 56% dividend payout rate (DPR) and a 22-year history of payment increases.

Republic Services: Minimum Balance Sheet Leverage and Dividend Resilience

Republic Services Inc. (NYSE: RSG) often plays second fiddle to WM due to its smaller market cap, lower dividend, and fewer locations.

But RSG boasts a few things that WM cannot: an earnings beat in Q4 2025 and a cleaner balance sheet.

RSG has less debt than WM and less M&A activity, which often leads to slower growth but also lower leverage.

RSG’s dividend yield is lower at 1.13%, but its DPR is a healthy 36%, suggesting more upside for dividend increases.

RSG also has a fuel surcharge model similar to that of its larger competitor, helping blunt rising oil prices.

RSG shares have lagged WM so far in 2026, and the technicals show a bit more conflict between buyers and sellers on the daily chart. But if volatility is the new normal, RSG has a chance to continue the breakout that began last November.

The stock appears to have found support at the 50-day moving average, and the RSI is back to levels that previously marked short-term lows. A sustained move above the 200-day moving average could be the next catalyst.

Clean Harbors: High Upside From Government Contracts

Clean Harbors Inc. (NYSE: CLH) isn’t a traditional waste management company like RSG or WM, but it does have more upside.

More than 75% of the company’s revenue comes from Environmental Services, a more cyclical revenue stream than Collection and Disposal, but Clean Harbors can count on the planet’s best client: the U.S. government.

The company has a multi-year agreement with the Department of Defense for polyfluoroalkyl substances (PFAS) filtration services, with an option to expand each year.

PFAS are dangerous ‘forever chemicals’ that could potentially be in the water at more than 700 military bases. Clean Harbors is the only company capable of all three phases of PFAS filtration, remediation, and incineration, giving the company a deep moat for its services and a leg up on more government contracts.

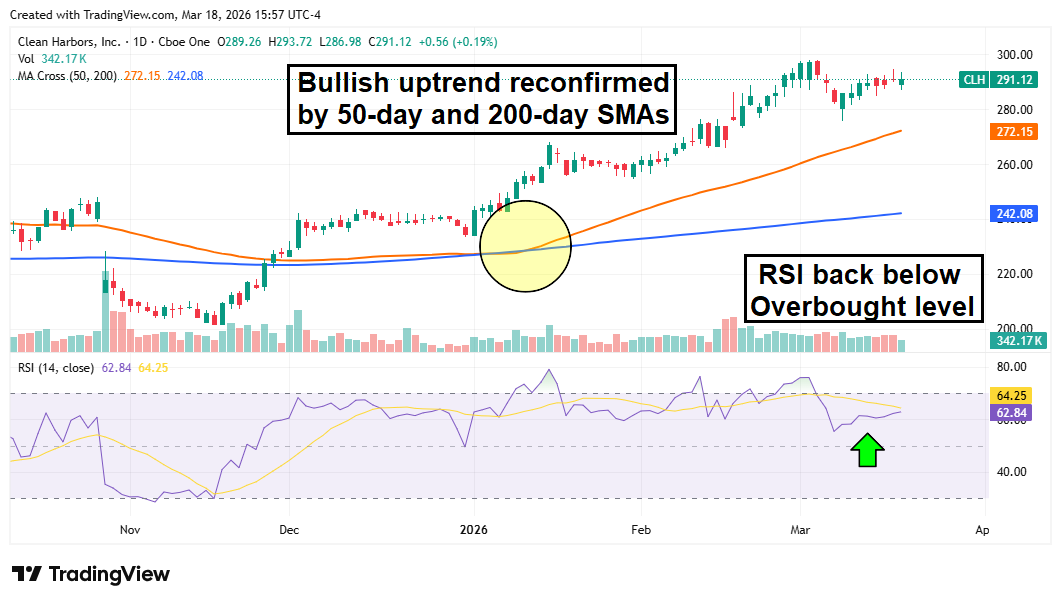

Investors love a company with steady government contracts, and CLH shares have gained more than 20% year to date. Shares are in a strong uptrend, trading well above the 50-day and 200-day moving averages, and the RSI is no longer overbought.

With the DoD now involved in what appears to be a long conflict with Iran, defense budgets are likely to increase even further than the Trump administration’s requests at the start of the year, which could bring even more revenue to Clean Harbor’s coffers.

Read this article online ›

The best investment opportunities don't wait. Get our research and stock ideas delivered straight to your smartphone—so you never miss a market-moving opportunity. Our text alerts ensure you see timely stock ideas and professional research reports instantly, whether you're in a meeting, commuting, or away from your desk.

Get Text Alerts from American Market News (free)

Tidak ada komentar:

Posting Komentar