March 23, 2026

The Fed Has No Clue What to Do

Dear Subscriber,

|

| By Nilus Mattive |

Life would be a lot easier if all fats were unhealthy …

It was always incorrect to wear anything white after Labor Day …

And our monetary policymakers knew exactly what was happening and what they should do next.

But as it turns out, things are a bit more complicated than we would like.

In fact, Fed Chairman Powell summed it up nicely in his post-meeting speech last week …

“In the near term, higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy.

“We will continue to monitor the risks to both sides of our mandate.

“We are well positioned to determine the extent and timing of additional adjustments to our policy rate based on the incoming data, the evolving outlook and the balance of risks.”

This is a very fancy way of saying, “We really have no idea what will happen next or what we will do about it.”

The Fed is now pointing to Iran as the big wildcard … which it is.

However, the central bank was already caught between a rock and a hard place before the first bomb fell.

Here’s the proof …

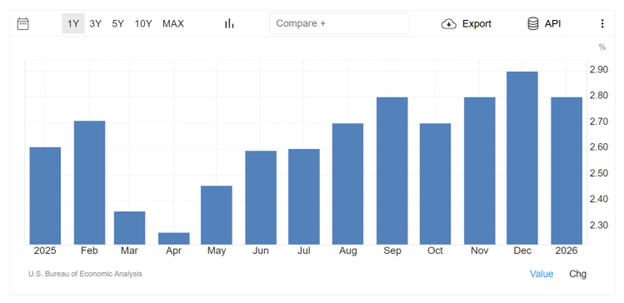

First off, inflation was ALREADY running hotter than the central bank’s stated target.

We’ve been running on delayed and/or partial inflation data because of the (last, full) government shutdown.

But based on the Fed’s favored measure — the Personal Consumption Expenditures (PCE) index — prices jumped 2.9% year over year in December and 2.8% year over year in January.

These levels are almost 50% higher than the Fed’s stated target of 2% and higher than what we were seeing a year ago.

We won’t get February numbers until April 9. But I can’t see any reason they won’t be in the same neighborhood or higher.

And again, this is all BEFORE the war began or oil prices started moving up.

If you were looking for one single input that affects the cost of nearly everything we consume, oil is it.

It fuels our cars, factories and delivery vehicles.

It is turned into the fertilizer for our food.

It becomes the materials we make our products from.

It is everywhere and in everything.

So yeah, the Fed is right to be worried about rising oil prices. It is literally gasoline on an inflationary fire that was already cooking.

Of course, people (and businesses) will also start altering their behaviors if prices stay elevated.

Which brings us to the Fed’s other mandate — propping up the economy and the jobs market.

Second, economic growth was ALREADY slowing before the war, too.

U.S. gross domestic product (GDP) rose at a 0.7% annualized rate in Q4 2025.

That number was after a significant downward revision from an initial 1.4% estimate … below forecasts … and sharply lower than the 4.4% increase we saw a quarter earlier.

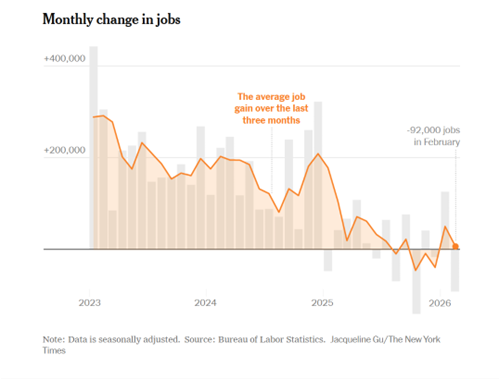

Meanwhile, the latest jobs numbers were equally rough.

The U.S. economy lost 92,000 jobs in February, a sharp reversal from prior months and a weaker result than economists anticipated.

Of course, we also got downward revisions for prior months as well. As the New York Times summarized it:

“Revisions to previous months bolstered the case that the job losses in February were consistent with a broader trend rather than a blip.

“Employers shed 17,000 in December, and hiring figures for January were also revised downward slightly.

“Taken together, job growth for the last three months effectively slowed to zero.”

The unemployment rate moved up to 4.4%, higher than what we saw in 2023 and 2024 and a continuation of an overall cooling trend.

So, yeah, Powell was technically correct when he told reporters that “unemployment is close to its long-run average, and inflation is not at a level that high.”

But both sides of the equation — and again, this is using data BEFORE the war started — are bad for policymakers and everyday Americans.

Which is why Fed members themselves were ALREADY split about which of those two problems was the more urgent one.

As I explained after the Fed’s December meeting, five votes were all for the quarter-basis cut that happened …

Four more officially supported it but expressed concerns …

Two members voted against the cut …

And then one person voted for an even bigger cut!

We saw similar tension during the next meeting in January.

Ten members voted to keep rates steady, while two members voted for another cut.

This time around? Eleven members voted to keep rates steady, while Stephen Miran (again) argued for a cut.

And I suspect more than one of the 11 were already thinking about the possibility of future rate HIKES.

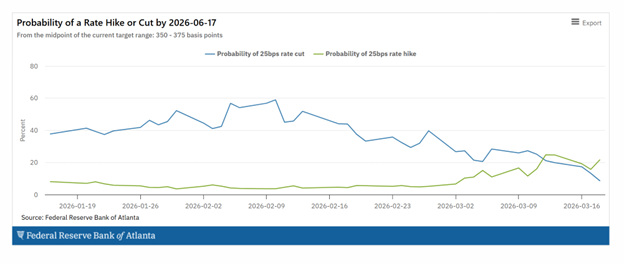

The markets certainly see that divide.

Just look at the Atlanta Fed's Market Probability Tracker, a tool that estimates where markets think rates are going over the next three months.

In late February, there was overwhelming consensus for future rate cuts.

Right before last week’s Fed meeting, the odds had evened out between rate cuts and rate hikes.

And now they are moving in opposite directions, with a much higher probability of interest rates going up.

This is all very bad news.

The Fed didn’t know what to do before Feb. 28.

It seems to know even less now.

And it is highly likely that inflation will only go higher, and the economy will only grow weaker from here.

Yet the stock market is still more richly valued than at almost any other time in history.

That makes absolutely no sense at all. And it’s going to crush millions of portfolios.

Which is why I just recorded this urgent new warning.

It explains why what’s happening right now will pop the massive speculative bubble in technology stocks …

Why that will ripple through the entire U.S. economy and financial system …

And what immediate steps you should take to keep your money safe before it’s too late.

All I ask is that you check out the evidence I present and then decide for yourself if I’m right or not.

Hey, if we learned anything this past week, it’s that the people in charge of U.S. monetary policy have no clue what’s going to happen next.

And that fact alone should scare anyone who’s paying attention.

Best wishes,

Nilus Mattive

Tidak ada komentar:

Posting Komentar