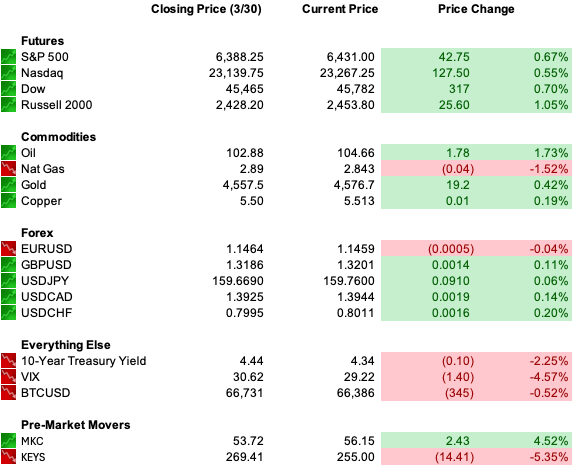

| TQ Morning Briefing | Iran struck a fully loaded Kuwaiti tanker in Dubai's port overnight. Oil jumped nearly four percent. Then the WSJ reported Trump is willing to end the war even if the Strait stays closed. Oil gave it all back. Equity futures are up. Micron (MU) is down in Asia again. The same overnight session produced a ceasefire signal and a tanker attack. The market is going to have to pick one. | | | | | | | Q1 closes with two signals pointing in opposite directions | Futures are higher on the ceasefire headline. European markets followed. Asian markets didn't hold. The Nikkei closed down more than one and a half percent. Chip names led the decline. | Today is Q1's final session. It's ending worse than it started. The Nasdaq and Dow are both in correction. Every Mag 7 name is lower for the year. | Treasury yields stayed lower. Powell told Harvard yesterday the Fed will look through the energy shock. The VIX is still meaningfully elevated. | Market Implication | If Consumer Confidence deteriorates sharply at 10am, the morning's futures gains are on borrowed time. If it's less bad than feared, rate-sensitive names have room through the close. |

| |

| | |

| | | | | WHAT ACTUALLY MOVED MARKETS |

| |

|

| | | | Two contradictory signals in one overnight session | Iran hit the Al-Salmi, a fully loaded Kuwaiti VLCC, at Dubai Port's anchorage just after midnight local time. Oil jumped four percent. Then the WSJ reported Trump told aides he's willing to end the war without first reopening Hormuz. Oil gave it all back. WTI swung nearly six dollars and closed the overnight session barely changed. | That swing is the story. The market tried to price de-escalation. Iran made it impossible. Nobody has an exit.

The WSJ report deserves more attention than the oil reversal gave it. Trump willing to end the war without reopening Hormuz isn't a diplomatic compromise. It's the US potentially accepting a closed or partially tolled Strait as a permanent outcome. | Every energy price model the market is running assumes Hormuz reopens on American terms and the supply premium unwinds. If it doesn't, if the toll booth survives the ceasefire, then the front end of the oil curve isn't pricing a temporary disruption. It's pricing the new normal. | Refiners, airlines, and every industrial with Gulf feedstock exposure don't get their cost structure back. They adapt to it. That's a different set of earnings assumptions than anything consensus has on the tape right now. | Powell told Harvard yesterday the Fed will look through supply shocks. That only works if the shock is short. If the Strait stays closed through April, energy costs start embedding in services inflation. Then the look-through breaks. Bonds priced option one. They haven't priced option two. | Structural Setup | Integrated energy names hold the supply premium. If Hormuz reopens on American terms, that premium unwinds and rate-sensitive sectors reassert. If it doesn't, the bond market's look-through assumption fails and the front end of the curve reprices to match what oil is already saying. |

| |

| | |

| | | | | | | Chips led down; financials held | The rotation isn't new. Monday made it undeniable. Micron's post-earnings slide extended all week into bear market territory. Google's compression announcement is still repricing memory demand. Western Digital and Sandisk followed. Financials, utilities, and energy gained. | Breadth has collapsed. In January, most S&P 500 names traded above their 50-day moving average. Now it's a fraction of that. All Mag 7 names are meaningfully lower for the year. Microsoft has led the decline. Apple has held up best. | Sector Read | Chipmakers are pricing two things at once: last week's AI demand reset and the ongoing Middle East supply chain risk. If it were purely demand, Lam Research and Western Digital wouldn't be moving. But they are. Memory decoupling from the broader chip selloff means demand was the driver. |

| |

| | |

| | | | | Iran hit a tanker in Dubai. Not the Strait. Dubai. | The Al-Salmi wasn't in the Strait. It was in Dubai Port's anchorage zone. Iran's reach now extends well past the chokepoint into the Gulf itself. On the same day, Chinese-flagged vessels were clearing the Strait with Iran's blessing. The terms of passage in the Gulf today depend on who's asking. | Consumer Confidence prints at 10am. The Michigan final showed expectations at multi-year lows. The Conference Board's Expectations component has fallen below 80 before every recession since 1990. When it breaks that level, a downturn has followed within twelve months in each instance. | Watch Signal | If Expectations break hard today, the names that price it first are DAL, UAL, and discretionary retail. Energy and staples hold. |

| |

| | |

| | | | | America's Economist: The #1 Stock Buy This Week | | Ex-CIA Economist says this stock is critical to national security. And predicts a major investment from the Trump administration in the days ahead. Why he personally bought 10,000 shares here. |

| |

| | |

| | | | | The petrodollar crack | Iran isn't just closing Hormuz. It's running a toll booth. Payments run in yuan. And it's working. China, India, and Pakistan are paying it. Every day the system runs, the precedent deepens. This isn't a temporary wartime anomaly. It's a pilot program. | The WSJ report suggests Iran keeps partial Strait control even after the fighting stops. That means the toll booth survives the war. Energy is priced in dollars but settling in yuan at the chokepoint. Two different systems. | The Read | Brent paper futures are up roughly half what Dubai physical prices have moved since the war started. The gap is the tell. Dollar-denominated markets are still taking Trump's de-escalation comments at face value. Physical buyers in Asia are not. If the toll booth survives the ceasefire, that gap closes the hard way. Paper reprices up to meet physical, not the other way around. |

| |

| | |

| | | | | Economic S&P/Case-Shiller Home Price Index, House Price Index, Chicago PMI, JOLTs Job Openings, CB Consumer Confidence, API Crude Oil Stock Change | Fed Speakers: Goolsbee, Barr | Earnings: McCormick (MKC), Nike (NKE) | Overnight: Nikkei -1.58% | Shanghai -0.80% | FTSE +0.48% | DAX +0.45% |

| |

| | |

| | | | | | | | | Nike reports tonight. The setup is bearish. Consumer confidence has crashed. Gas prices are hitting household budgets. China is weak. The EPS bar is well below where it sat a year ago. That's not the interesting question. | The interesting question is whether a beat even matters. Cisco beat every line and opened lower. Nike could do the same. | Consumer Confidence at 10am sets the tone. If Expectations collapse, Nike walks into tonight facing a sentiment wall it can't beat its way through. If the print is less bad than feared, the path opens. | Come back tomorrow. At least one of those forks will have moved. |

| |

| | |

|

|

Tidak ada komentar:

Posting Komentar