| | | | There is a quiet room in lower Manhattan — fluorescent light humming, coffee going cold. An analyst stares at a number that fits no past template. Private sector AI spending in 2026 is set to top $700 billion. As a share of GDP, that beats the combined peak yearly spend on 1930s public works, the Manhattan Project, the postwar electricity boom, the Apollo program, and the Interstate highways. | Nothing like this has happened before. If you feel very sure how it ends, you are likely wrong. | The debate over whether AI is a bubble has run for two years. Most of it has asked the wrong question. The right question is not if a correction comes — it is where the damage lands when it does. That answer depends on plumbing, not story. It depends on who funded what, with whose money, and against which revenue streams. Here is what we see when we follow the wiring. |

| |

| | |

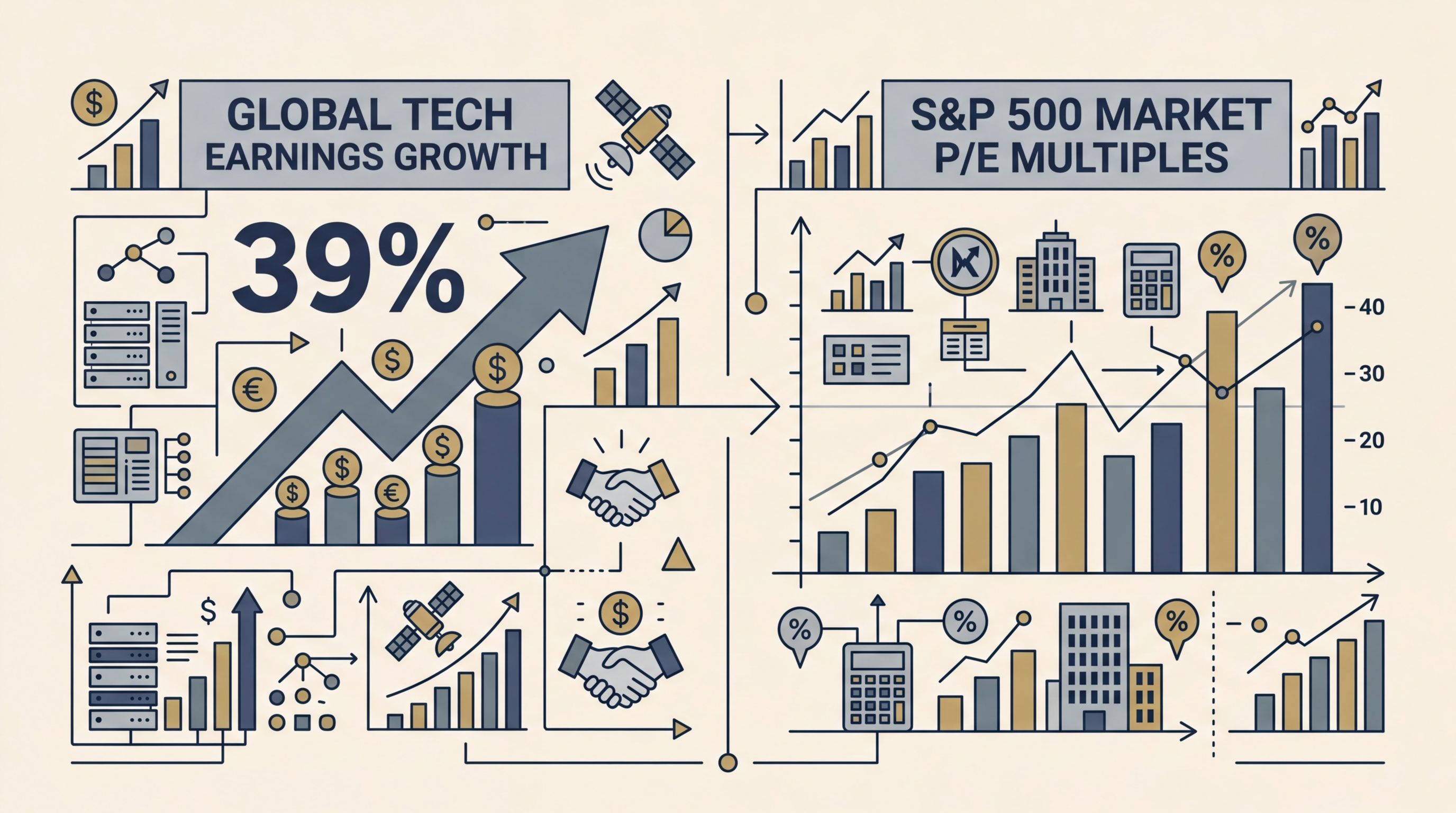

| | | | | The Earnings Story That Breaks Every Bear Case | The simple bubble thesis goes like this: hype lifts prices, capital floods in, reality catches up, everything crashes. It is a clean story. Right now, it is also incomplete. | ClearBridge Investments' Jeff Schulze made the case plainly. In the final year before the dot-com peak in March 2000, 87% of tech returns came from multiples expanding — investors paying more for each dollar of earnings. In 2025, that flipped. Earnings drove over 100% of tech returns. Multiples actually shrank. At the index level, earnings powered 82.5% of S&P 500 returns last year. P/E ratios rose by less than one turn. | This is not a small gap. It is the difference between a market running on facts and one running on faith. The Mag Seven ex-Tesla trade at a forward P/E of roughly 27.4x — a steep discount to both the Nifty Fifty and the dot-com darlings at their peaks. Lombard Odier's March 2026 review backed the picture: the MSCI US IT Index trades at 23x forward earnings, well below late-1990s levels. Global tech earnings are set to grow 39% in 2026 versus 15% for the broader market. | The revenue surge at the frontier labs is just as hard to wave away. OpenAI and Anthropic together run at over $44 billion in yearly revenue as of March 2026. Stripe, with its wide view across thousands of firms, says AI companies are growing revenue faster than any group it has ever tracked. Generative AI is still less than 1% of GDP — hinting that the spending wave has room to run before it nears the 3% share reached during the dot-com era. | The earnings story is real. It is the strongest defense the bulls have. And it is the very argument that needs the hardest stress test. | |

| |

| | |

| | | | | The Rational Bubble — Where Every Actor Makes Sense and the Outcome Still Doesn't | Here is where the first signal appears. Something more complex is stirring beneath the surface. | Investor and writer Paul Kedrosky, in a March 2026 talk with Derek Thompson, was blunt: "Yes, AI is a bubble. There is no question." His case was not that the tech is fake. It was that the mix of loose credit, real estate bets, government policy, and a huge buildout has never hit all at once in modern history. Every time even two of those forces have met, a bubble followed. | This is what finance calls a rational bubble. Each actor — the hyperscaler signing a lease, the utility building a substation, the credit fund lending to a data center REIT — acts wisely in their own frame. But all those wise choices add up to a result no single player controls. The hum of cooling towers across Virginia and Texas is the sound of good logic stacking into something no one planned. | Kedrosky flagged a detail most coverage missed: the stock-based pay loop. Oracle, Microsoft, and Google pay as much stock-based pay as ever. But buybacks — the tool that offsets dilution — have shrunk sharply. Cash that once funded $6–8 billion in yearly buybacks now flows into GPU clusters. The money is not idle. It is being rerouted, quietly, from shareholder returns into hardware. That is a regime change in how capital gets spent. Most investors have not priced it in. | | Sponsored by Brownstone Research

The Federal Reserve chair recently told the press that this AI frenzy is not like the dot-com bubble for one simple reason: These companies actually have earnings. | However, former hedge fund manager Larry Benedict pushed back on this argument in a recent interview. | He said that there's always a reason to justify absurd valuations: | | Larry pointed out that Lehman Brothers posted record profits in the years leading up to its collapse. | He also pointed out here that the companies leading the AI revolution have a major financial flaw that could soon lead to their "Lehman Brothers" moment. | When this flaw is exposed, it could trigger up to a 80-90% crash in any of the Mag Seven stocks. And it would be wise to not dismiss this warning as hyperbole. | Larry is one of the most successful hedge fund managers of our time. | From 1990 to 2010, he had a historic run without a single losing year. That means he profited through the Long-Term Capital Management bailout, the dot-com crash, the 9/11 recession, and the 2008 financial crisis. | So whenever Larry steps forward with new research, smart investors always pay attention. | | |

| |

| | |

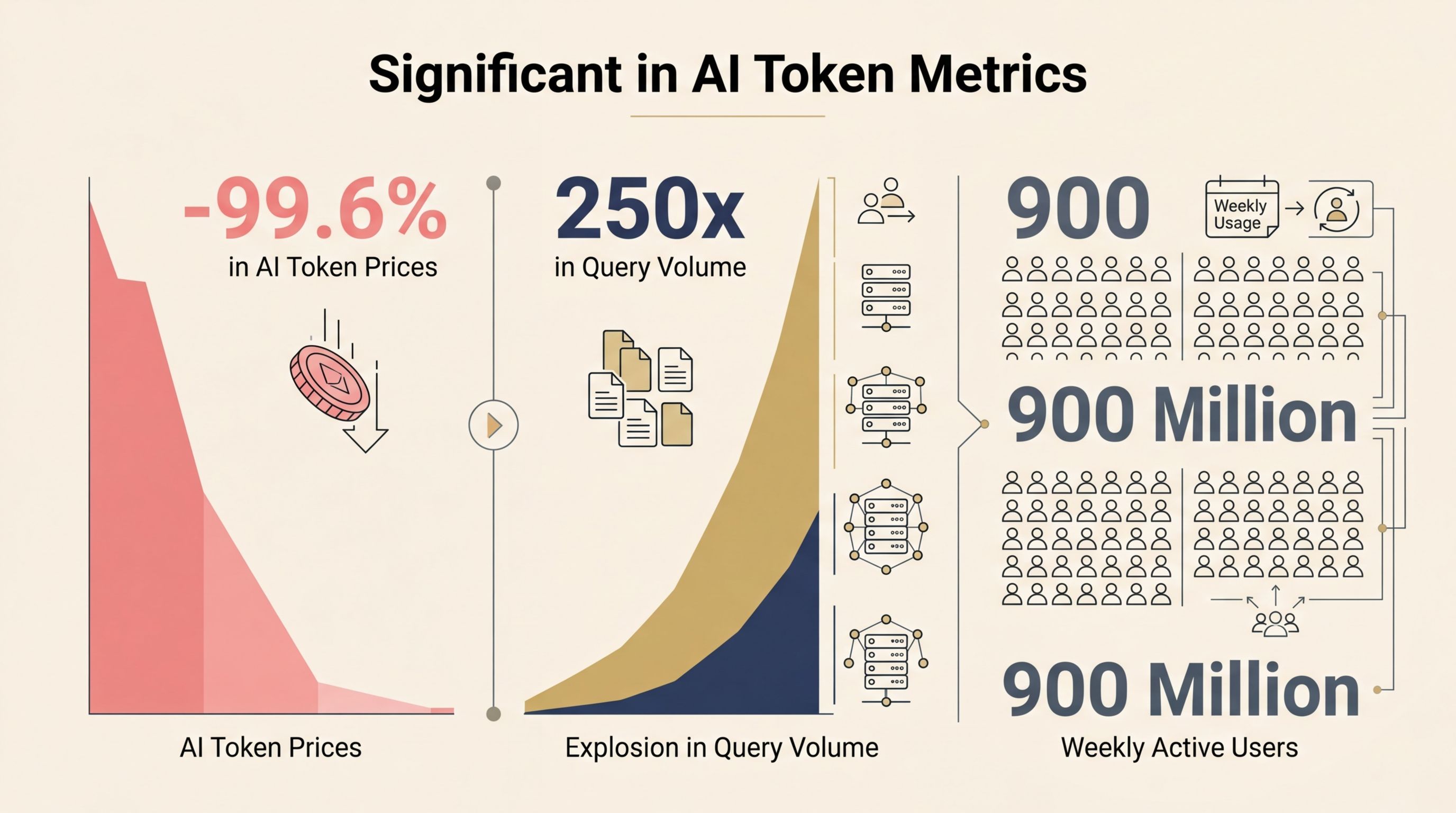

| | | | | The Contagion Path Runs Through Disruption, Not the Builders | The dot-com crash was a story of builders going broke. Fiber-optic firms borrowed against users who never showed up. Banks held the paper. Losses spread fast. | The AI correction, when it arrives, will follow different wiring. The Big Four hyperscalers — Microsoft, Alphabet, Meta, Amazon — funded their 2025 capex fully from cash flow. Fidelity's February 2026 review found none of the usual bubble red flags: no shrinking free cash flows amid heavy spending, no rising debt ratios. JPMorgan ran a five-factor test in December 2025 and said the sector looks more like a utility than a bet. | The caveat is real and growing. Big tech firms have sold $100 billion in bonds so far in 2026 to fund AI builds. OpenAI has pledged $1.4 trillion over eight years against roughly $25 billion in ARR. The "funded by earnings" story holds for the big hyperscalers — and cracks for the pure-play AI firms outside the Big Seven. | Here is the key shift for your portfolio: the credit risk sits not in the companies building AI, but in the companies being disrupted by AI. Think legacy software firms in private credit funds. Think SaaS companies watching renewal rates drop as AI agents replace whole workflows. The damage runs through the disruption of old players, not the failure of new builders. That is a very different risk map — and it calls for a different kind of watch. | Financial historian Edward Chancellor put it simply on Bloomberg: "History teaches us that speculative bubbles, however advanced their premise, always burst." The question is not if. It is where the scaffolding gives way. | The Mental Model That Survives the Correction | So where does this leave you — the exec placing bets, the builder picking a platform, the investor sizing a position? | Satrix head of portfolio solutions Nico Katzke offered a frame worth keeping: the dot-com crash did not kill the internet. It simply came before a huge growth era for the firms that survived. The cables — those fragile undersea fiber-optic lines that analysts mocked in 2001 — became the invisible rails of a $50 trillion digital economy. You are reading this on those rails right now. | The AI cycle will rhyme. Token prices have fallen 99.6% since GPT-4 launched. Demand moved just as Jevons predicted — query volume up 250x, revenue growing because volume rose faster than price fell. ChatGPT has 900 million weekly active users. Two Fed officials said in late February that workers seem helped by AI, not replaced. The plumbing is being laid for a utility, not a gamble. | But utilities still have correction cycles. The Case-Shiller P/E ratio for the U.S. market has topped 40 for the first time since the dot-com crash. The top five S&P 500 firms hold 30% of the index — the highest share in half a century. Sam Altman himself has said he thinks an AI bubble is underway. | The mental model that lasts: treat the tech as plumbing and the prices as weather. Plumbing endures. Weather shifts. The builders with cash flow will ride out the storm. The pure-play firms burning capital against trillion-dollar pledges will face the worst wind. Act on that — not with panic, not with hype, but with the quiet focus of someone who knows the pipes outlast the noise every single time. | | |

| |

| | |

| | | | |  | | | Brownstone Research | |

|

|

|

|

|

|

| |

| | |

| |

|

Tidak ada komentar:

Posting Komentar