Editor's Note: What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500? Click here to see the details from former tech executive and angel investor Jeff Brown — the man who picked Bitcoin, Tesla, and Nvidia before they exploded higher. Or read more below. | | Dear Reader, | What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500? | Click here to see the details because everyone is talking about Elon Musk's SpaceX IPO. | CNBC called it "the big market event of 2026." | And The New York Times predicted… | This IPO "will unleash gushers of cash for Silicon Valley and Wall Street." | You see, this is NOT about launching rockets to Mars, satellite internet, or anything you've heard from the media. | It's much bigger than that… | Because this IPO is a key part of Elon Musk's secret AI masterplan… | A plan that I believe will unlock the full power of artificial intelligence... | Unleashing what Elon Musk is predicting will be… | A $1 quadrillion new wealth wave. | Just to put that into perspective… | That would be enough to send a check for $2.8 million to every single man, woman, and child in America. | That's how big this opportunity is. | Click here to get the details and I'll show you how to claim your stake… | Starting with just $500. | We have so much to look forward to, | Jeff Brown

Founder & CEO, Brownstone Research | | | | | |  | Fresh Insight for You |

|

|

|

The $265B Private Credit Selloff: Disaster or Discount? |

|

|

|

Before You Scroll Past This One… |

Let's say you had a perfectly good savings account earning 8–10% a year. Solid returns. Clean track record. No drama. |

Then one day, your neighbor starts whispering that the bank might have a problem. A few others hear it. Then a few more. Nobody checks the facts, they just start pulling their money out. And suddenly, your account is marked down 40%, 50%, even 66%… not because anything changed inside the bank, but because the rumor spread fast enough to become the story. |

That's basically what's happening in private credit right now. |

$265 billion in market value has evaporated from some of Wall Street's biggest alternative asset managers. And the question every smart investor is asking this week is the same one you should be asking: Is this real trouble, or is someone ringing the fire alarm in a building that isn't actually on fire? |

Bank of America just weighed in. Their answer might surprise you. |

|

The Panic Is Real. But So Is the Opportunity. |

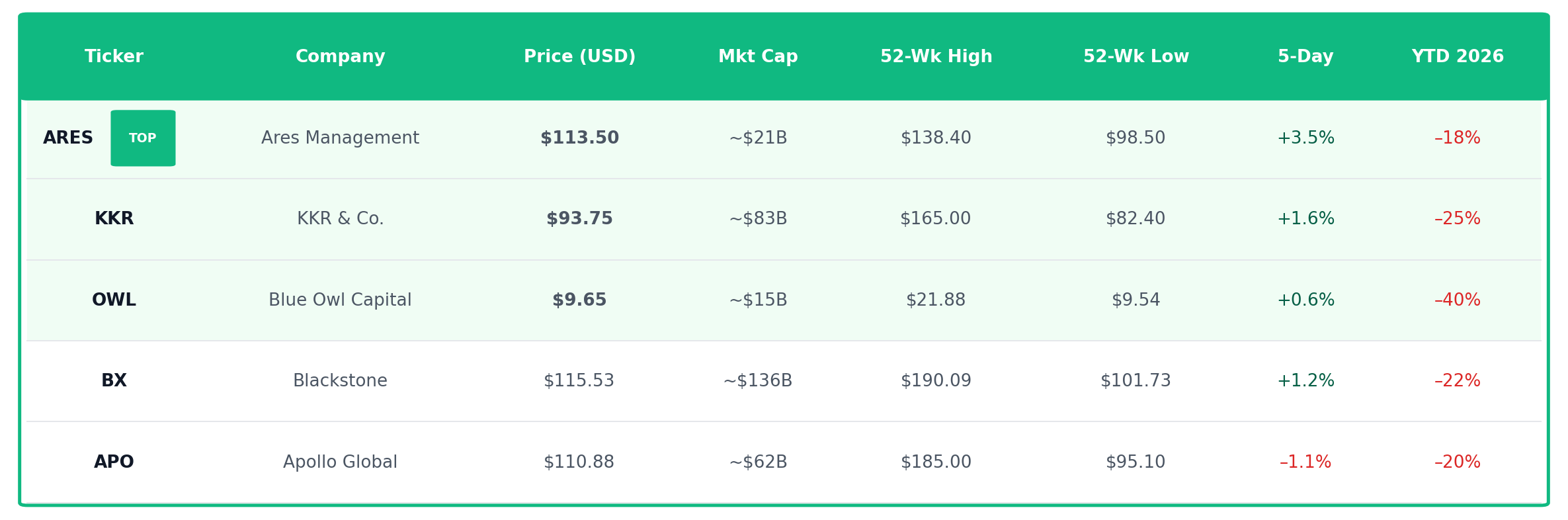

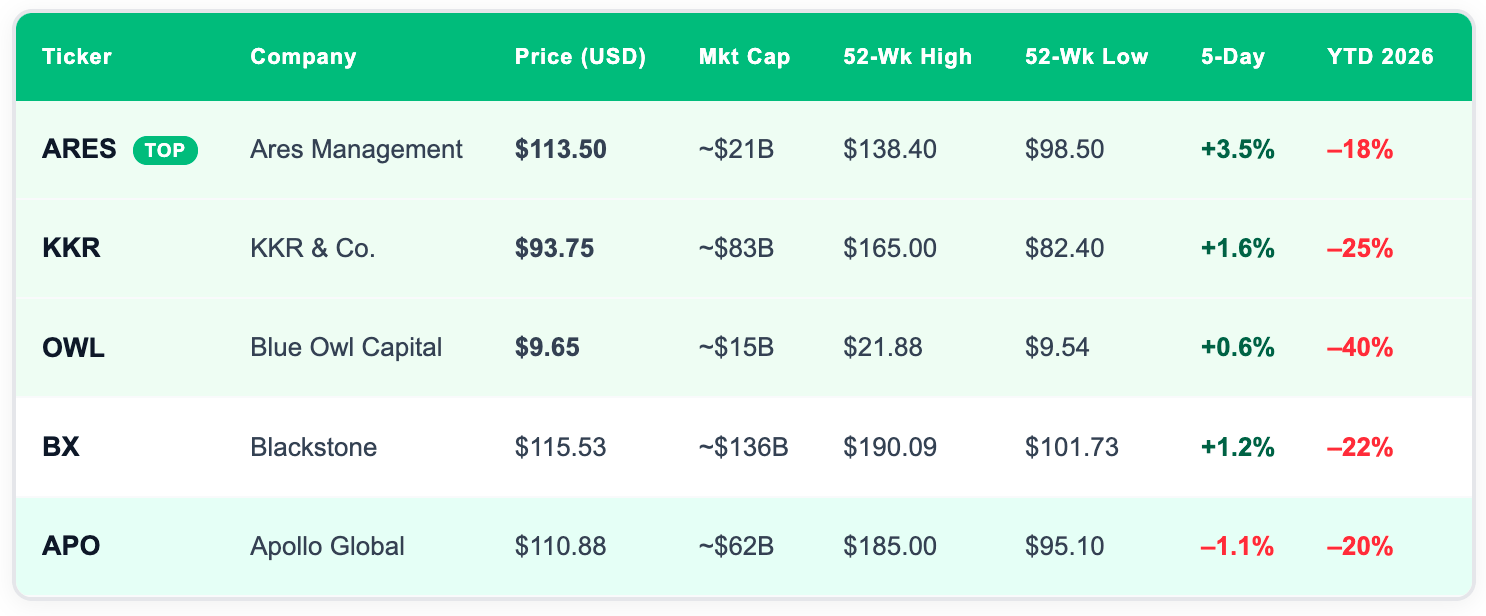

| Price Comparison, ARES, KKR, OWL, BX, APO (March 24, 2026) |

|

Here's a number that'll stop you cold: $265 billion. |

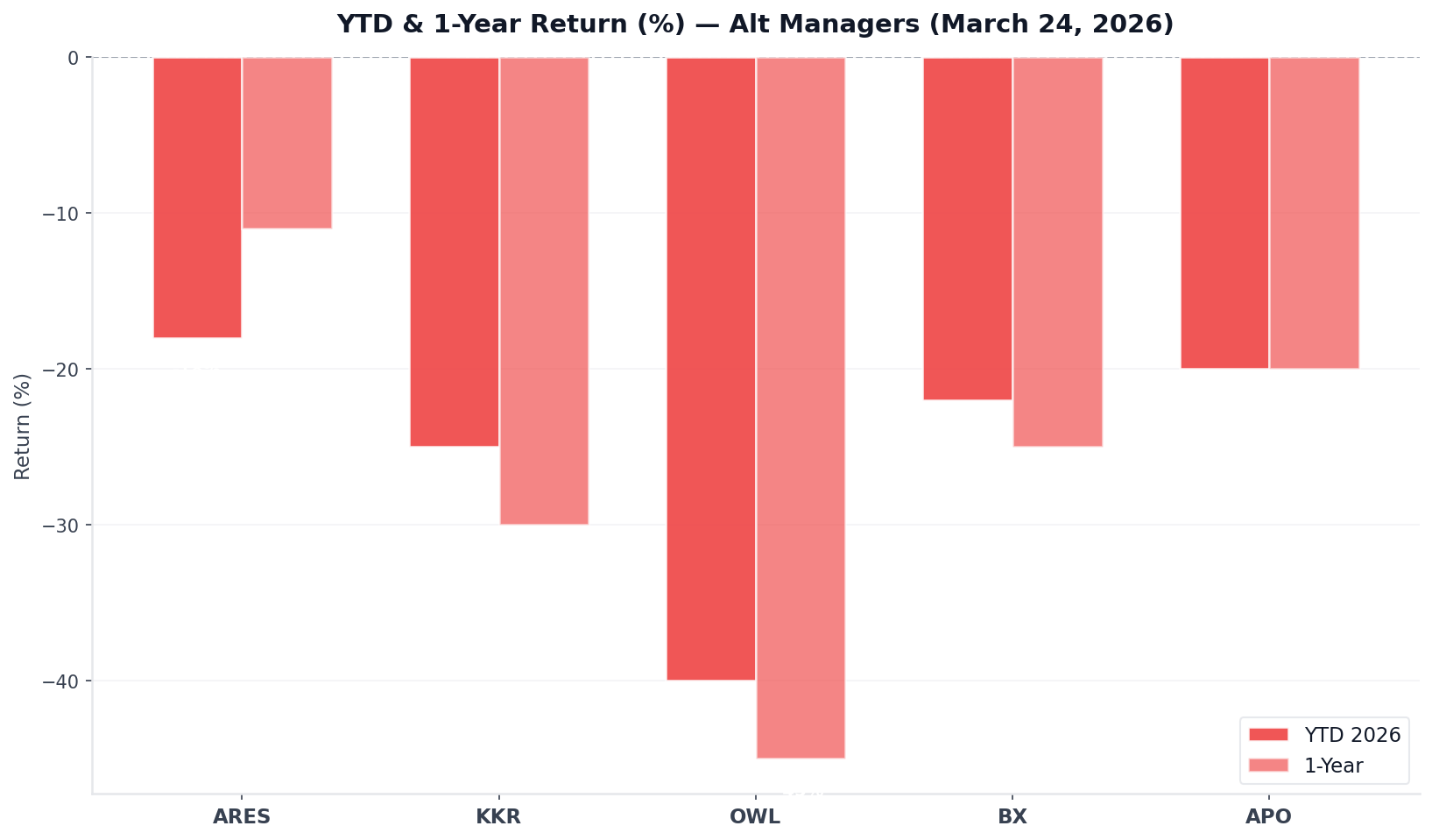

That's how much market value has been wiped off alternative asset managers since their peak in early 2025. Stocks like Blue Owl (OWL), Ares Management (ARES), and KKR (KKR) are down 40% to 66% from their highs. The headlines have been brutal. Words like "meltdown," "liquidity crisis," and "panic" are everywhere right now. |

And honestly? Some of that concern is fair. |

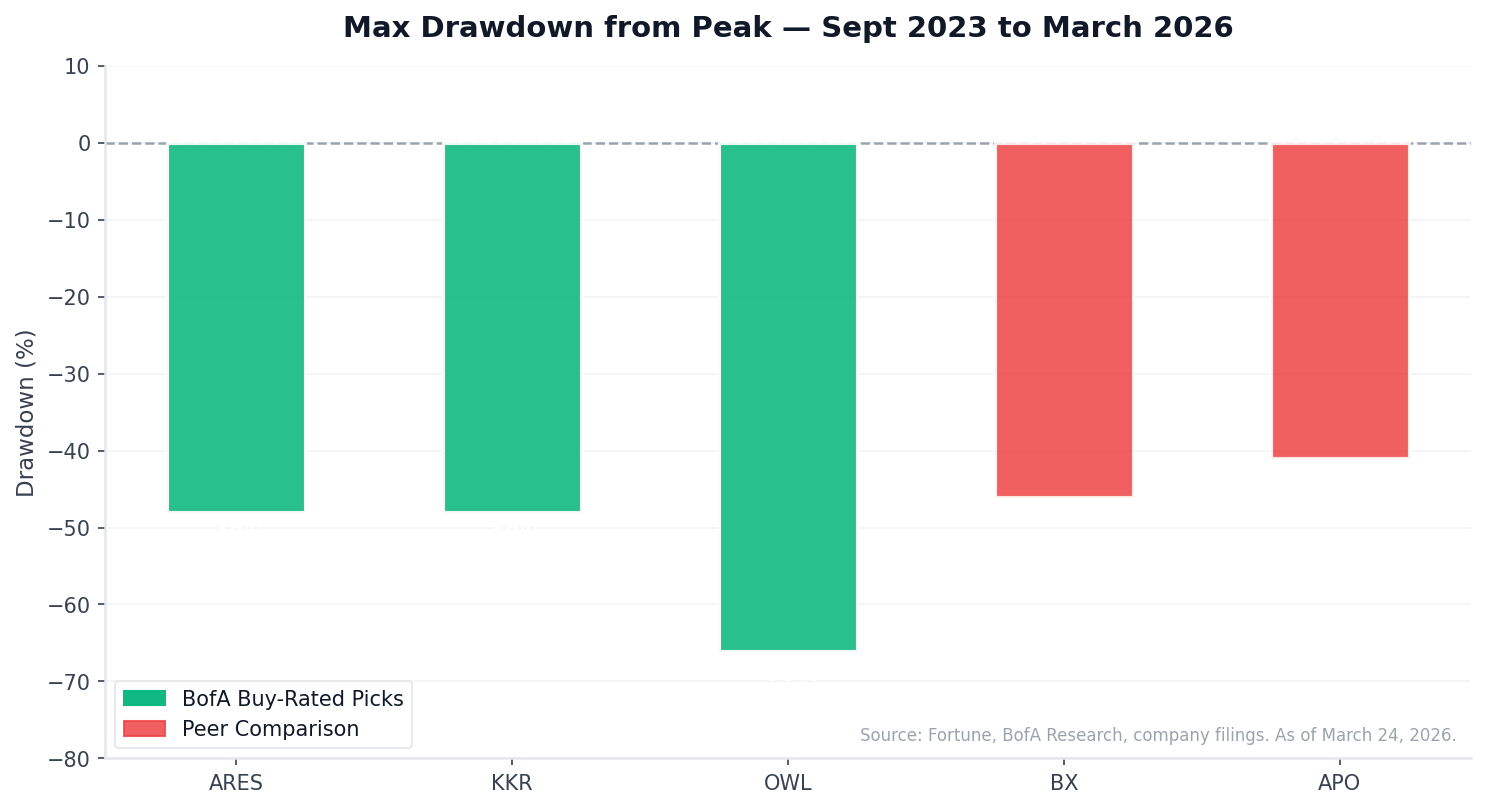

But here's what the headlines aren't telling you: Bank of America just told its clients to buy the dip. |

This week, BofA analysts flagged what they called a "fire sale opportunity" in private credit stocks. They argued the selloff has been driven by "low-value data points" and a "media obsession", creating a real disconnect between these companies' actual fundamentals and their current stock prices. BofA maintained Buy ratings on Blackstone, KKR, and Blue Owl, and bumped Ares up to their top pick. |

That gap between fear and fundamentals? That's exactly where smart investors look. |

|

Wait, What Even Is Private Credit? |

Fair question. This is one of those corners of finance that's been quietly growing for years, mostly out of sight for everyday investors. |

Think of private credit like this. When a mid-size company needs to borrow money, they have a few options. They can go to a bank. They can issue bonds anyone can buy. Or they can go to a private lender, a firm like Ares or Blue Owl, that writes them a custom loan, often for more money, faster, with more flexible terms than a traditional bank would offer. |

That's private credit. And the market for it has grown to roughly $1.8 trillion in the U.S. alone. |

Why did it explode? Simple. After the 2008 financial crisis, banks got more restricted on what they could lend. Private credit firms stepped in to fill that gap. Then came years of low interest rates where investors were starving for yield. Private credit funds were offering 8–12% annual returns, way more than bonds or savings accounts. Money poured in. |

| ❝ | | | "The best opportunities are in markets where people get a little scared." | | | | Jonathan Gray, President, Blackstone |

|

|

|

So What Went Wrong? |

|

A few things collided at once. And understanding each one matters before you look at any stock. |

First: the retail investor problem. Firms like Blackstone and Blue Owl started marketing "semi-liquid" private credit funds to everyday investors, not just big pension funds. The pitch was access to institutional-quality returns. But when markets got choppy, retail investors wanted their money back. And unlike a stock, you can't just sell private credit overnight. Blue Owl had to sell $1.4 billion in loans to meet redemption requests. Blackstone's BCRED fund got hit with $3.8 billion in withdrawal requests and used its own capital to cover them. |

Second: software exposure. A lot of these private credit firms lent heavily to software companies, specifically SaaS businesses. In early 2026, AI disruption fears hit that sector hard. JPMorgan began marking down the value of software-related loans. Investors got scared that the valuations private credit firms were putting on their portfolios weren't accurate. |

Third: headline contagion. When one fund restricts withdrawals, every fund in the space takes the hit. Fear spreads faster than facts. Ares, KKR, even Apollo got sold off, even though their direct exposure to the problem areas was limited. |

| | The #1 Coin Set to Replace Bitcoin? | I revealed something that could change the future of crypto investing forever… | The name of the #1 coin that could replace Bitcoin as the top-performing asset in the market. | This coin is backed by major global players like J.P. Morgan and Blackrock, and it's set to benefit from a massive shift towards real-world assets on the blockchain. | See which coin is poised for 150x gains HERE. | *ad |

| | |

|

|

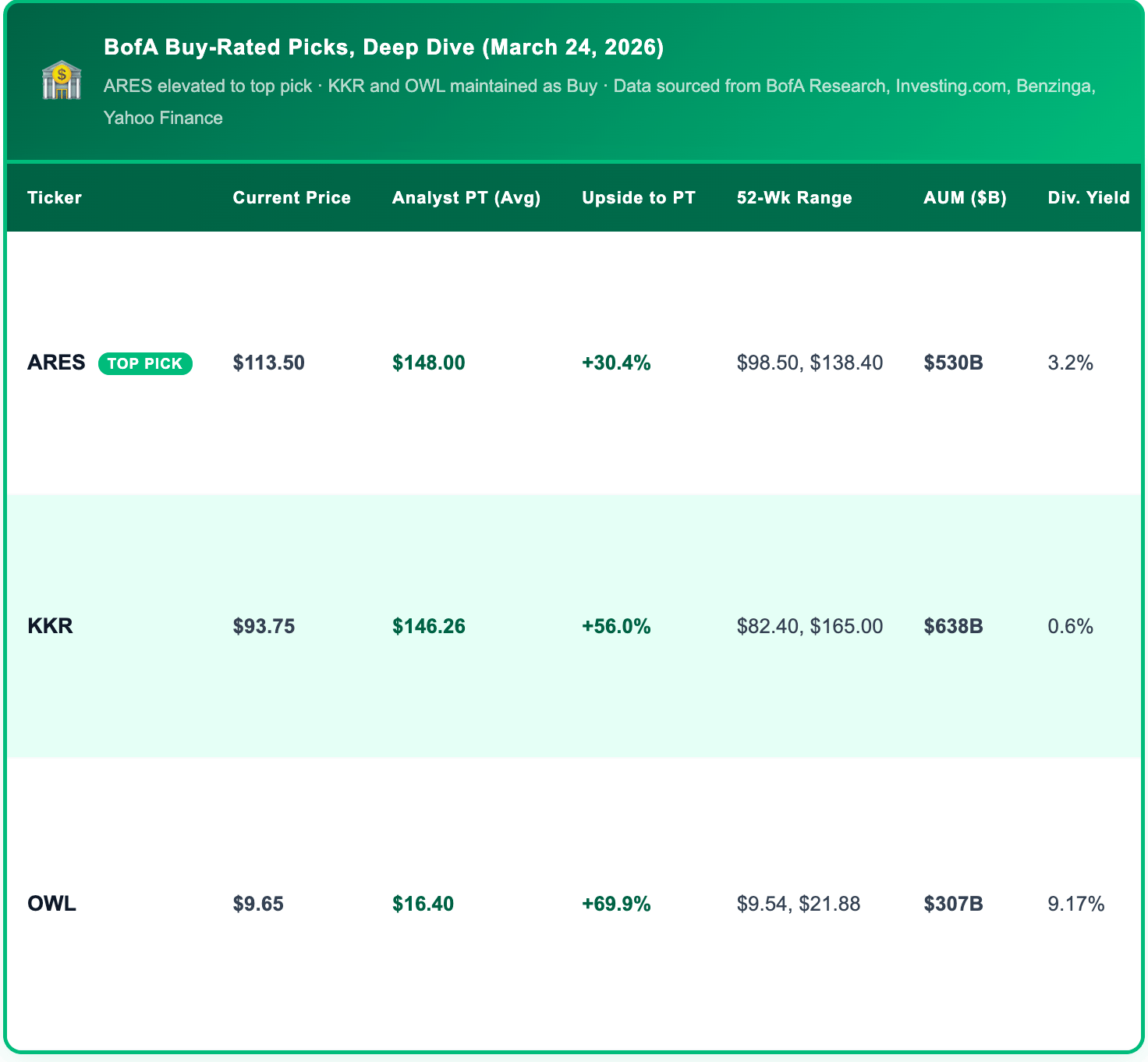

Here's What BofA Is Actually Saying |

| Global space economy projected to reach $1.8 trillion by 2035. Source: McKinsey Global Institute, April 2024. |

|

The BofA analysts pushed back hard on the narrative. Their note called the negative sentiment "driven by misinformation." They pointed to specific data that the market was largely ignoring. |

On Ares ( $ARES ( ▼ 1.52% ) ): Their flagship Business Development Company has returned 12% annually since its 2005 inception, two decades of outperforming peers. Software is only 12% of their direct lending book, and management has characterized it as high-margin "systems of record" businesses, not speculative tech bets. |

On KKR ( $KKR ( ▼ 1.66% ) ): KKR's software exposure is just 7% of its portfolio. Its long-term earnings estimates haven't moved. But its stock has. That kind of divergence, where the price drops but the fundamentals don't, is exactly what value investors look for. The current consensus analyst price target sits at $146.26, while the stock trades near $93.75 today. |

On Blue Owl ( $OWL ( ▼ 2.0% ) ): The loan sales that spooked the market were executed at 99.7 cents on the dollar, essentially face value. If these loans were toxic, that number would look very different. "OWL's investment performance is solid to strong across all of its strategies," BofA wrote. "Credit quality in credit remains above average." The consensus analyst price target is $16.40, against a current price of just $9.65, an implied upside of over 69% if analysts are right. |

|

The Stock Comparison Table |

|

Here's a look at where these names stand right now, as of March 24, 2026, updated with the latest available market data: |

|

|

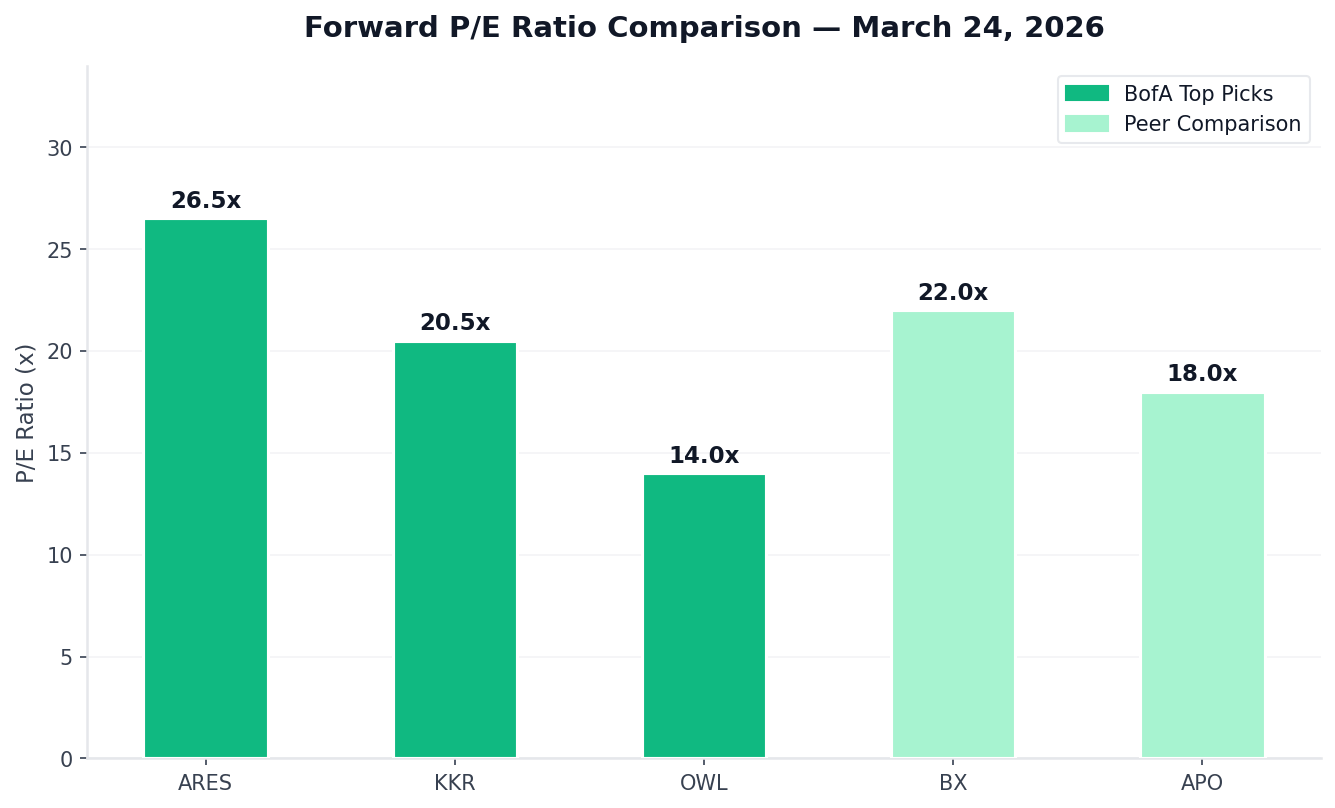

BofA's Top Picks, A Closer Look |

|

The general comparison table tells you where things stand. But for the three stocks BofA actually named as buys, here's the detail that matters, the price targets, the upside, the dividend, and the one-line case for each one: |

|

What the Experts Are Saying |

The debate is real, and the voices are big. |

Mohamed El-Erian, Jamie Dimon, and George Noble have all weighed in recently on private credit risks. The macro concerns, AI disruption, refinancing walls, credit quality, are legitimate topics for serious investors. |

But Blackstone President Jonathan Gray pushed back. He described the liquidity caps in semi-liquid funds as "a feature, not a bug", you're trading a bit of accessibility for higher returns. Blackstone's BCRED has generated a 9.8% return since inception, suggesting the underlying performance story is intact. |

Jim Cramer called private equity stocks "the most toxic area of 2026" in mid-March. But TD Cowen recently said Blue Owl remains a buy, it'll just "remain choppy through Labor Day." |

The honest read here: there is real stress in parts of the market. But there's a difference between a structural problem and a narrative problem. BofA's position is that this is mostly the latter. |

|

What Should You Actually Do With This? |

First, a reality check. These are not simple, low-risk stocks. They're complex financial businesses in a volatile environment. The risks BofA flags as "overstated" are still real risks. Software loan quality, retail redemption pressure, and the 2026 maturity wall are all live issues. |

But the question for investors isn't whether risks exist. It always is: is the price right for the risk? |

BofA thinks yes, especially for Ares, KKR, and Blue Owl right now. Their argument is clear: strong long-term track records, manageable software exposure, solid credit quality, and prices that already reflect a lot of bad news. |

If you're considering this space, here's how to think about it practically: |

Start small. Don't bet the whole portfolio on a sector recovery. A small position in ARES or KKR gives you exposure without overconcentration. Watch the quarterly NAV updates. The next round of Business Development Company reports will tell you whether the markdown fears were real or not. That's the data that matters. Look at the AUM trend. As long as Ares ($530B), KKR ($638B), and Blue Owl ($307B) keep growing assets under management, fee income keeps flowing. That's the engine of the business. Know what you own. These stocks can swing hard. If you'd panic-sell at a 20% drop, this sector isn't for you right now. Consider OWL's 9.17% dividend yield. While you wait for a potential price recovery, Blue Owl is paying one of the highest dividend yields among publicly traded alt managers. That's income in your pocket while the story plays out.

|

|

The Bottom Line |

Private credit is not broken. But it is being repriced. |

The selloff has been real, dramatic, and in some cases, overdone. BofA is saying the market has handed investors a chance to own some of the strongest alternative asset managers in the world at prices that reflect fear, not fundamentals. |

ARES at 30% below its analyst price target. KKR trading at a 56% discount to consensus. Blue Owl yielding 9.17% while trading near its 52-week floor. |

That doesn't mean it's a sure thing. Nothing in markets ever is. But if you've been watching these names thinking "I wish I'd bought before the run-up", you may not be too late. |

The panic created the price. The question is whether the fundamentals justify the bet. |

|

| | | | Quick ratingHow was this one? | |

| |

| | |

|

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions. |

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers. |

|

Tidak ada komentar:

Posting Komentar