February 23, 2026

Another Way to Hedge Against Dollar Weakness

Dear Subscriber,

|

| By Nilus Mattive |

For the last couple of months, I’ve mostly been writing about two major themes — metals and dividend stocks.

I have been bullish on metals for several reasons.

The two most important are:

- Their ability to diversify (and thus hedge) traditional stock portfolios and …

- The protection they offer in people heavily invested in U.S. dollars and dollar-denominated assets.

Meanwhile, as I explained last week, I like dividend stocks because they can also provide some degree of comfort in trying markets …

Not to mention steady income through thick and thin.

Today I want to talk about two different places where all these things intersect.

The first one is pretty obvious — the relatively small group of metals-related stocks that also happen to pay good dividends.

In fact, one of the very first recommendations that Mandeep Rai and I just made for Martin’s new Weiss Income Multiplier portfolio just so happened to be exactly that.

It’s a gold mining company that has not only made consistent payments for many years now but recently changed its dividend policy to be far more generous going forward.

This particular stock ticks all the boxes — some leverage to gold prices … soaring cash flows … equally soaring dividends …

Plus, another short-term catalyst in its underlying business that could unlock even more shareholder value before the year is over.

That connection to gold also makes it a bit of a dollar hedge.

Of course, there is another group of stocks that can hand you bigger income streams …

Not just from growing dividends … but anytime the U.S. dollar loses more value — foreign companies that trade here on U.S. exchanges.

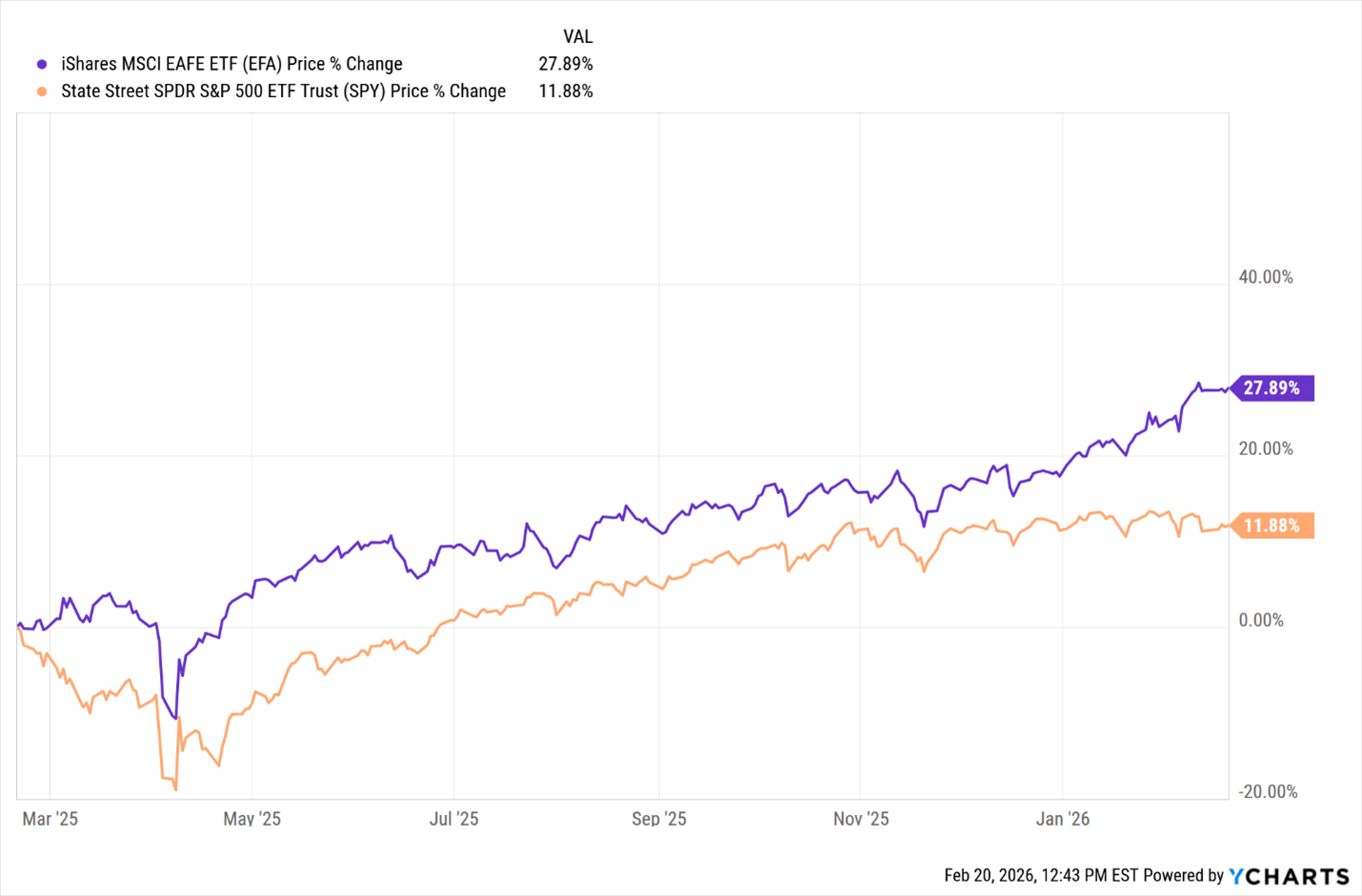

On a broad basis, foreign stocks have already been outperforming U.S. equities for a while now.

This is for several reasons.

For starters, they were generally trading at more reasonable valuations. And even after recent strength, that remains true.

For example, the MSCI EAFE index — which is comprised of companies based in developed countries outside the U.S. and Canada — is currently trading at a forward price-to-earnings (P/E) multiple of 15.9.

In contrast, the S&P 500 is trading at a forward P/E of 21.5.

Second, in some countries and/or sectors, there is also higher growth potential … which makes lower valuations even more attractive on a relative basis.

A good example might be European defense firms, which stand to benefit from rising domestic arms sales.

Most importantly, as we’ve been discussing, investors around the world have been looking to further diversify away from U.S. dollars and also hedge against U.S.-specific risks.

That last one is especially advantageous for U.S.-based investors.

Most big foreign companies trade on U.S. exchanges as American Depositary Receipts (ADRs).

That means their ADR shares are priced in U.S. dollars but reflect changes in the equivalent domestic stocks, including fluctuations in exchange rates.

When ADRs pay dividends, the same idea also applies.

The dividends are initially declared in the company’s home currency. But they are paid out to ADR holders in U.S. dollars.

So, if the greenback is weakening, the payments effectively go up in dollar terms.

Obviously, the inverse is also true. If the dollar strengthens, then both ADR share prices and dividends get negatively impacted.

However, for all the reasons we’ve covered, it at least makes sense to have a small allocation to foreign dividend-paying stocks (and bonds!) in your portfolio.

Best wishes,

Nilus Mattive

P.S. I’m actually recommending a foreign dividend fund and a foreign bond in Safe Money Report …

Plus, I also just told readers to swap out a U.S. pharmaceutical firm for one based overseas.

Martin tells you how to get details on all those picks at the end of this new video he just posted on the web.

Tidak ada komentar:

Posting Komentar