February 11, 2026

The Real Engine Behind Gold's Surge

Dear Subscriber,

|

| By Sean Brodrick |

The news babblers are rushing to blame gold’s rocket ride on speculation.

Nope. Gold is doing exactly what it’s supposed to do in uncertain times.

It’s being treated as real money again by the institutions that matter.

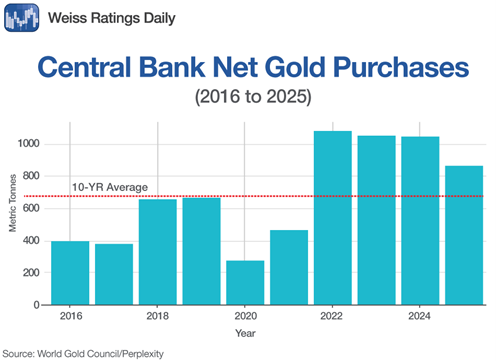

Central banks just finished another massive accumulation year.

In 2025, official sector buyers added 863 tonnes of gold, making it one of the strongest years on record.

Last year’s central bank gold purchases were slightly below the 1,000+ metric tonne buying spree we saw from 2022 through 2024.

Still, it was still nearly double the long-term average.

In other words, this change in central bank gold buying isn’t cyclical … it’s structural.

And that can push gold to much, MUCH higher prices.

BRICs Lead the Charge

The heavy lifting is being done by the BRICS bloc — Brazil, Russia, India, China and South Africa — and an expanding circle of partners.

From 2020 through 2024, BRICS nations accounted for more than half of global central bank gold purchases.

Their combined reserves now exceed 6,000 tonnes, with Russia and China alone holding over 4,600 tonnes.

The goal is independence from the U.S. dollar. Why? Well, that’s a heck of a story.

The “Sovereign Risk” Trigger

Central bank gold buying exploded in 2022 to 1,136 tonnes, the highest since 1950.

The primary trigger was how the U.S. and its allies responded to Russia’s invasion of Ukraine.

What they did was freeze approximately $300 billion of Russia’s foreign exchange reserves held in Western banks.

For China, Turkey and the Middle East, this showed that the dollar was at the mercy of Uncle Sam.

Their solution was to buy gold — a physical asset that is sanctions-proof insurance.

It has no counterparty risk and can’t be frozen.

Central banks understand that in a world where financial systems are increasingly weaponized, gold has real value.

Over time, as U.S. relations with the rest of the world have worsened, de-dollarization picked up steam.

BRICS countries are settling more trade in local currencies, building payment systems that bypass SWIFT and even proposing digital settlements partially anchored by physical gold.

Gold Is Replacing U.S. Debt

Surveys now show most central bankers expect the dollar’s share of global reserves to keep shrinking, while nearly all plan to continue adding gold.

In a milestone moment, gold has overtaken U.S. Treasurys in some central bank reserve mixes for the first time in decades.

Just this week, Chinese regulators advised the nation’s financial institutions to lower their holdings of U.S. government bonds.

China Keeps Stacking

The latest data from the People’s Bank of China confirms the trend is alive and well.

As of Feb. 7, China extended its gold-buying streak to 15 consecutive months, adding another 40,000 ounces — roughly 1.24 tonnes — in January 2026.

On a volume basis, that looks modest. On a value basis, it’s anything but.

The dollar value of China’s gold reserves jumped by more than $50 billion as prices surged.

Why This Doesn’t End in 2026

Wall Street believes the world’s central banks will keep stacking.

- JPMorgan expects 755-800 tonnes of central bank gold buying in 2026 — well below the peak years, but still nearly double the 10-year average.

- Goldman Sachs sees steady purchases of about 70 tonnes per month— or about 840 tonnes — creating what it calls a “structural bid” that limits downside risk.

There is a parade of forces driving demand into next year and beyond:

- Weaponization of the Dollar: Emerging markets continue to hedge against sanctions risk by accumulating neutral assets with no political strings attached.

- U.S. Fiscal Stress: With national debt north of $38 trillion and deficits spiraling, central banks are protecting themselves against long-term dollar debasement.

- Gold Scarcity: Grassroots exploration budgets fell 15% in 2023 and another 7% in 2024. It can take years to find a mine. The discovery pipeline is drying up fast.

There were no major gold deposits— defined as 2 million ounces or more — discovered globally in 2023 or 2024, and preliminary data suggests 2025 is the same.

Even when discoveries occur, they are smaller in scale.

Since 2020, the average new find is about 4.4 million ounces, down from7.7 million ounces a decade ago.

That adds up to a structural supply problem that can’t be fixed quickly, no matter how high prices go.

The Bottom Line

Gold isn’t rising because of speculation. It’s rising because the institutions that run the global financial system are voting with their balance sheets.

Supply is tightening. And central banks — especially in the BRICS world — are telling you, quietly but unmistakably, that gold is back where it belongs: at the center of the monetary system.

I’ve explained why my target for gold is $10,000 an ounce.

I’ve also detailed why that might be low. I guess we’ll see.

In the meantime, investments like the iShares Gold Trust (IAU) and Van Eck Junior Gold Miners ETF ( GDXJ) should double — or more!

Individual miners — leveraged to gold — could do a heck of a lot better.

Hey, if you can’t beat central banks, join ‘em!

They’re stacking gold. Prices will go higher.

That kind of math means gold is one of the smartest, easiest investments you can make.

But there’s a better way to take part than simply owning ETFs or physical metals. I show you exactly how here.

All the best,

Sean

Tidak ada komentar:

Posting Komentar