|

|

Urgent: On Tuesday, September 24th, at 1 PM ET I'm going live to reveal the secrets behind 23 out of 27 winning trades. These aren't ordinary plays—they're 24-hour Profit Windows most traders miss. |

Want to learn how to spot and capitalize on these fleeting opportunities? |

Click here to reserve your spot. |

____________________________________________________________ |

Don Kaufman here. |

Today, we're diving deep into a crucial market phenomenon that's become even more relevant in recent times: the gamma squeeze, and how 0 DTE options have amplified its impact. |

This isn't just some fancy Wall Street jargon – it's a powerful force that can drive significant market movements, and understanding it can give you a serious edge in your trading. |

Let's break it down: |

First, we need to understand two key concepts: delta and gamma. |

Delta is the rate of change in an option's price relative to the change in the underlying asset's price. In simple terms, if an option has a delta of 0.5, its price will change by $0.50 for every $1 move in the underlying stock. Delta ranges from 0 to 1 for calls and 0 to -1 for puts. |

Now, what the heck is gamma? |

Simply put, gamma is the rate of change in an option's delta. |

It measures how fast delta changes as the underlying asset's price moves. |

|

Here's where it gets interesting. |

The big players in the options market, like Citadel or Virtu, aren't in the game to take directional bets. |

Their goal is to maintain what we call "delta neutrality" – basically, they're trying to balance their books to minimize directional risk. |

So, when a market maker sells a call option to a retail trader, they're left with negative delta exposure. |

To offset this, they immediately buy some of the underlying stock to get back to neutral. |

No big deal, right? |

Wrong. |

This is where the squeeze begins. |

As the stock price starts to rise, those call options begin to move deeper into the money. Their delta increases, which means the market maker needs to buy even more stock to stay neutral. |

This buying pressure pushes the stock price even higher, which in turn increases the delta of those options even more. |

See where this is going? |

We've just entered a positive feedback loop. The more the stock goes up, the more the market makers have to buy, which pushes the stock up even further. |

It's like a snowball rolling downhill, gathering more snow and momentum as it goes. |

This, my friends, is a gamma squeeze in action. It's not about technicals, it's not about fundamentals – it's pure, unadulterated market mechanics. |

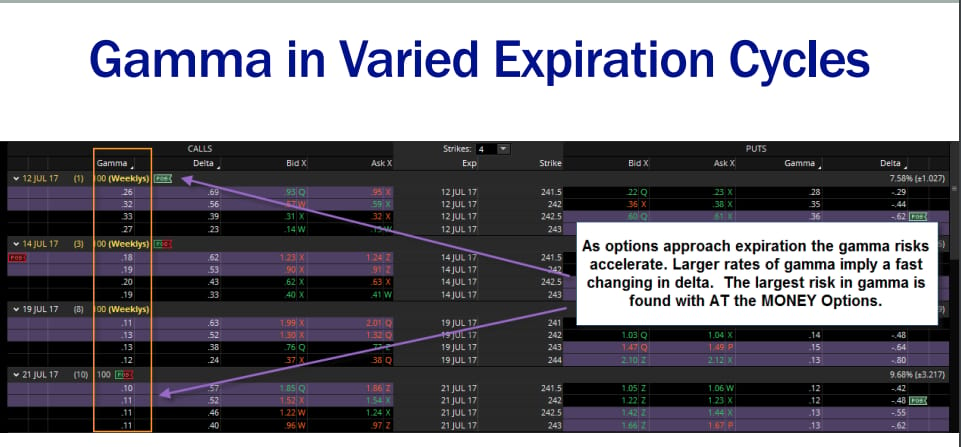

Now, here's the kicker: this effect can be especially pronounced leading up to major option expiration dates, like the triple witching we see quarterly. |

As expiration approaches, gamma typically increases, which can amplify these feedback loops. |

But here's the real nugget of wisdom I want you to take away: when those options expire, all that gamma risk suddenly disappears. |

It's like pulling the plug on the whole system. This is why you often see increased volatility around expiration dates, and why the market can sometimes feel "free" after a big expiration event. |

Now, let's talk about how 0 DTE options have turned this whole dynamic up to eleven. |

|

0 DTE options are options that expire the same day they're traded. They've exploded in popularity recently, and let me tell you, they've made gamma squeezes even more potent. |

Why? |

Because 0 DTE options have extreme gamma. Remember, gamma increases as expiration approaches, and with 0 DTE, you're dealing with options that are hours or even minutes from expiration. |

This means the gamma effect we talked about earlier is supercharged. |

Think about it. |

Market makers selling these 0 DTE options have to hedge their positions in real-time, often leading to rapid, outsized moves in the underlying asset. A small price movement can trigger a cascade of hedging activity, potentially leading to sharp intraday swings. |

This is why you might see the S&P 500 make sudden, seemingly inexplicable moves, especially in the last hour of trading on days when these options expire. |

It's not news, it's not some big fund making a move – it's the mechanics of 0 DTE options playing out. |

But here's the twist: because these options expire so quickly, the effects are short-lived. The market can snap back just as fast as it moved. This creates both opportunities and risks for savvy traders who understand what's happening. |

Now, you might be thinking, "Don, this sounds like a day trader's dream!" |

And you're not wrong. But remember, with great power comes great responsibility. |

These dynamics can create incredible opportunities, but they also amp up the risk. You're essentially trading alongside some of the biggest, fastest players in the market. |

So, how can you use this knowledge? |

Be aware of expiration dates and times, especially for heavily traded indices like the S&P 500. |

Watch for unusual volume in 0 DTE options – it could be a sign that a gamma squeeze is brewing. |

Understand that late-day moves, especially on Fridays, might be more about option mechanics than fundamental factors. |

If you're holding positions overnight, be prepared for potential gap openings as the effects of the previous day's 0 DTE options wear off. |

Remember, the market isn't just about charts and news. It's a complex system driven by the actions and reactions of various players, and 0 DTE options have added a new dimension to this ecosystem. |

By understanding phenomena like gamma squeezes and the impact of 0 DTE options, you're peeling back another layer of the market onion. |

Keep this in mind next time you see a stock or index making a big, seemingly unexplainable move, especially late in the trading day. |

Ask yourself: could there be a gamma squeeze at play here? |

And could 0 DTE options be adding fuel to the fire? |

To your success, |

Don Kaufman |

P.S. I'm going LIVE tomorrow to reveal my favorite strategy for taking advantage during this Fed rate-cut cycle. |

Click here to reserve your spot. |

Tidak ada komentar:

Posting Komentar