April 2, 2024

2 ETFs to Pay Your Skyrocketing Insurance Premiums

Dear Subscriber,

|

| By Gavin Magor |

Known as one of the most hated industries, insurance companies face a never-ending battle to gain consumers’ trust.

And there’s not a whole lot being done to help the situation. In fact, it’s getting worse.

Now, I usually write about the current crisis facing homeowners in states most at risk for natural disasters (Florida, California, Texas and others). Many are increasingly unable to secure property & casualty policies or can’t afford skyrocketing premiums.

Some insurers have literally pulled out of states and left residents in a lurch. Just last week, California’s largest insurer, State Farm, announced that it will discontinue coverage for 72,000 houses and apartments in the state this summer.

The company pulled the rug from right under these homeowners, who assumed that paying their insurance bill every month earned them a semblance of safety or peace of mind. Instead, homeowners are more at risk than ever, while insurance companies take risk off their plates.

There’s plenty wrong with this picture. However, we’re doing everything we can here at Weiss Insurance Ratings to contribute to your peace of mind.

It’s the very reason we monitor the “wellness” of insurance companies (and banks), rate them accordingly and provide you with warnings about solvency, health or trustworthiness.

It’s come to my attention recently, though, that auto insurers are the latest to breach an already-eroding trust with consumers.

Unfortunately, I found out the hard way.

Insurance Hits Home for Me

I’ve always been under the impression that auto insurers base rates on driving records, accidents, age, car make and model, annual mileage and other factors that determine risk.

The more risk, the higher the premium, right? That would make sense.

I always assumed that if I were to go a year without any tickets or accidents, not make a single claim and add very few miles on my 2020 Volvo XC-60, the cost to renew my policy would stay the same. Or it might be slightly higher to cover the rate of inflation.

I get a renewal notice twice a year from my insurer, and it’s paid automatically through my checking account. Normally, it doesn’t even dawn on me to check the monthly premium.

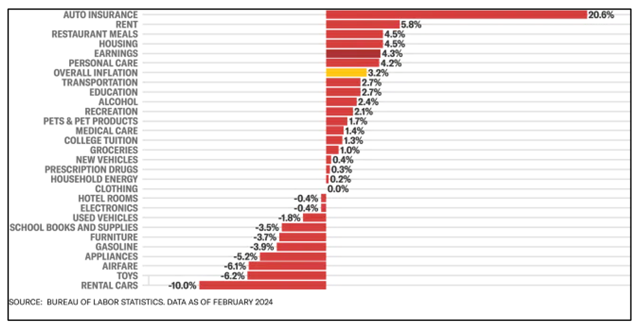

But that’s the first thing I did after stumbling on the below chart. I could barely believe my eyes. Costs of auto insurance rose a whopping 20.6% from Feb. 2023-Feb. 2024 — more than anything else on the list.

Sure enough, I tracked my payments over a year, and the cost went from $104 in January 2023 to $126 six months later. Today, it’s $133.

My policy shot up 27.9% in a year, and I didn’t even realize it. You might want to dust off yours, too.

Apparently, since far fewer people drove during the height of the pandemic, accidents and claims also fell. Now drivers are back on the road … and acting riskier than ever with a 10.5% increase in road fatalities since the height of the pandemic in 2021, while most Americans stayed at home.

The resulting accidents are costing a whole lot more in car insurance claims thanks to pricier parts, labor and medical bills.

So, insurance companies are fighting inflation with inflation. And you and I get to foot the bill on both ends.

They even have the backing of regulators, who recently allowed Allstate (ALL), and many others, to make 30% increases in California, 17% in New Jersey and 15% in New York.

For example, The Travelers Companies (TRV) pointed to more bodily injury claims for a reason it increased premiums in Q4 2023, especially for customers renewing their policies.

Travelers’ renewal premium price rose 16.7% in its auto business, contributing more than $2 billion of additional premium compared to the same quarter last year.

The second-largest auto insurer in the U.S. behind only State Farm, Geico was hit by six consecutive quarters of underwriting losses beginning at the height of the pandemic.

Geico eventually earned $3.64 billion before taxes from underwriting in 2023. But the trend toward bigger claims remains for all coverages including property damage (14-16%), collision (4-6%) and bodily injury (5-7%).

The company sought rate increases in numerous states in 2022 and 2023 in response to accelerating costs due to claims.

I hate to be the bearer of bad news, but there’s not a whole lot we can do to reduce our premiums. Even safe drivers are being thrown under the bus. And since it’s illegal to drive without insurance, you can’t just drop it.

You can, however, profit by investing directly in the markets … more specifically, insurance stocks or ETFs.

2 Insurance ETFs to Combat Your Own Premium Hikes

That’s where insurers go to make most of their money — the markets themselves — unlike the obvious way most people think: by selling policies and bringing in more money in premiums than they pay out as claims, also known as an underwriting profit.

This profit stream is just icing on the cake for most companies. Many are perfectly fine breaking even in that respect.

The second and more important way insurance companies profit is by investing funds from premiums before they are paid out for claims, called the float. Reserves are a huge component of success.

Just how much? Billions. Where do insurers keep that money? In conservative investments that probably return 2% a year as safely as possible. Remember, 2% of hundreds of billions of dollars is still billions of dollars.

Since they’re using your money to invest and ultimately profit, piggy banking on the idea and becoming a shareholder sounds like a solid plan to me. You can even use our Weiss Stock (and ETF) Ratings tool to find a good investment.

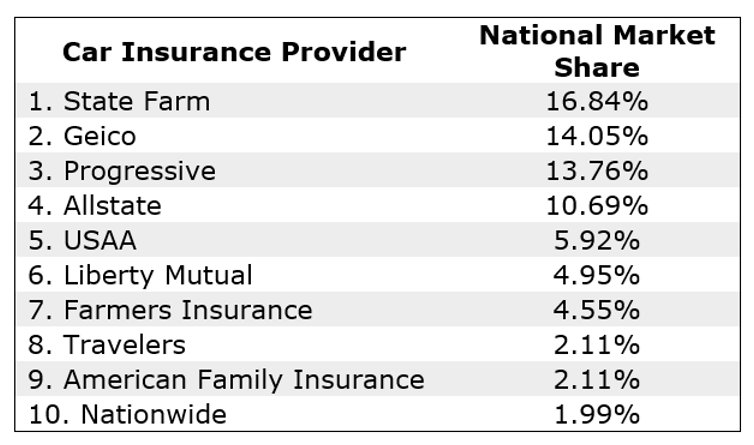

Here’s what the $155 billion auto insurance market looks like. According to the National Association of Insurance Commissioners (NAIC), the 10 largest car insurance companies account for 77% of the total U.S. market.

The largest auto insurer in the U.S. is State Farm, accounting for 16.84% of the car insurance market. Geico, Progressive (PGR), Allstate and USAA round out the nation’s top five largest car insurance companies.

One of the purest ways to invest in the overall insurance industry is with ETFs. I recommend taking a look at the iShares Dow Jones US Insurance ETF (IAK) and the SPDR KBW Insurance ETF (KIE).

They both include companies such as Allstate, Progressive, AIG, MetLife, Prudential, Travelers, Hanover Insurance Group, First American Financial Group and Chubb Corporation.

Year to date, IAK and KIE are up 13% and 15%, respectively. Both currently yield around 1.5%.

Insurance may not be sexy or all that trustworthy. But it’s an industry that can produce solid long-term returns and dividends without too much volatility.

Cheers!

Gavin Magor

Tidak ada komentar:

Posting Komentar