Elon Musk has a habit of being right about the future. He predicted electric cars would take over. He saw the AI boom before the rest of the world caught on. |

And now, he’s saying something big about Universal Basic Income (UBI). |

|

|

“UBI is going to be necessary.” – Elon Musk |

Why? Because automation and AI are replacing jobs. The way people earn money is changing forever. |

Here’s the good news: You don’t have to wait for UBI to start earning money effortlessly. |

Introducing Mode Mobile**—the smartphone that PAYS YOU to do what you already do.

-Listen to music? Paid.

-Browse the web? Paid.

-Charge your phone? Paid.

-Play games? You guessed it—paid. |

It’s not just a new phone. It’s a whole new economy—one that you can own a piece of. |

Smart investors are getting in early before Mode Mobile potentially explodes. Shares are available NOW—but they won’t be forever. |

Analysts estimate the smartphone economy exceeds $1T+ |

This is your moment. Invest before the next big shift happens. |

|

|

|

|

|

|

|

|

|

Fresh Insight For You |

|

|

|

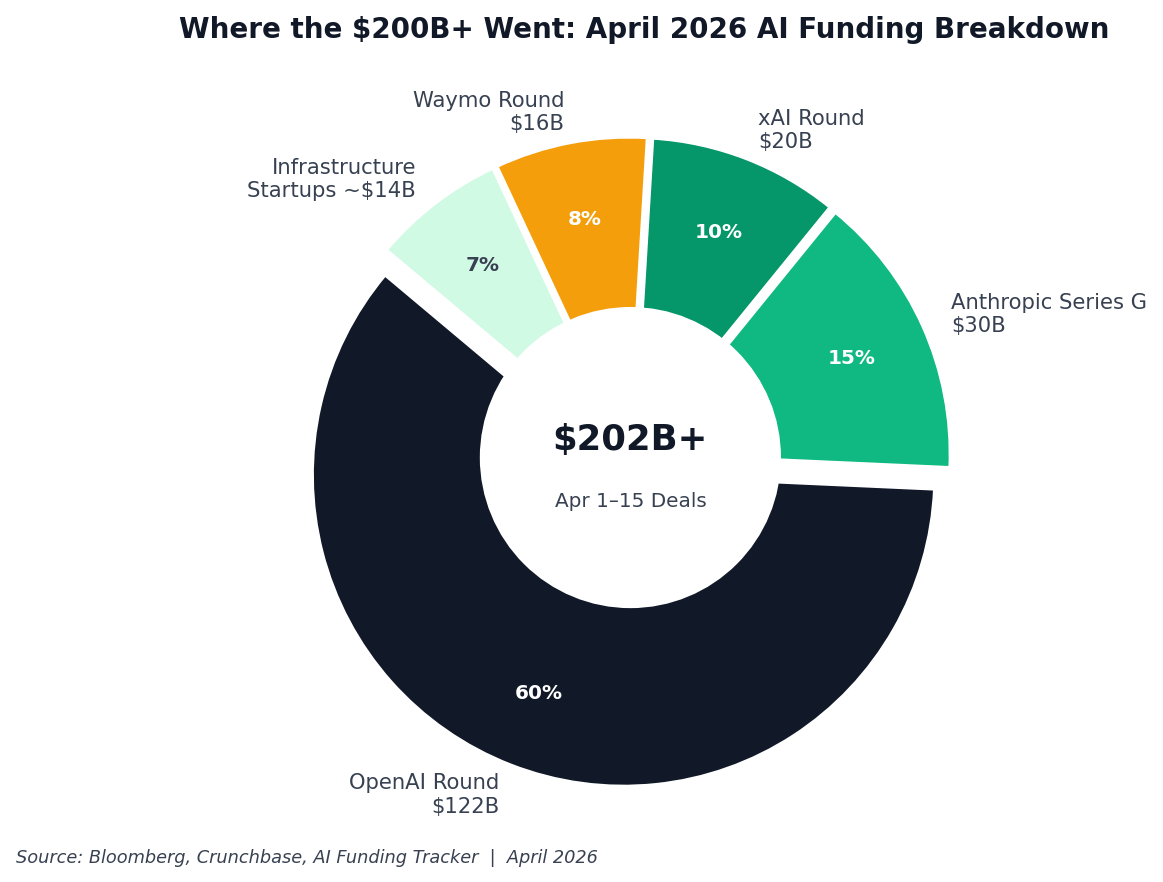

$200B in 15 Days: The AI Funding Sprint That Changed Everything |

|

|

|

|

KEY POINTS |

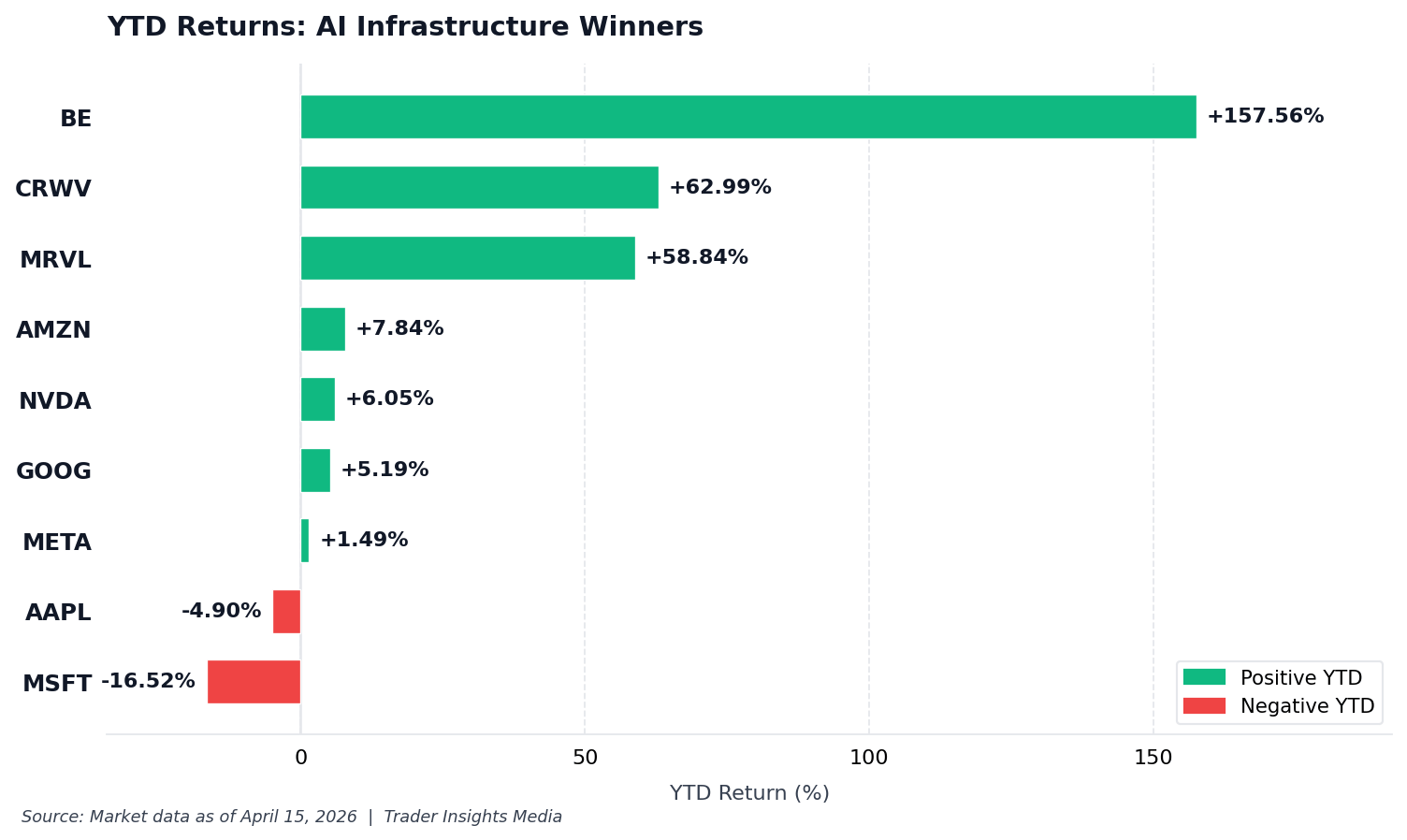

OpenAI closed a $122B round at an $852B valuation. Amazon replaced Microsoft as its primary cloud partner. Four hyperscalers are approaching $700B in 2026 CapEx, more than most countries' entire GDP. Generative AI is on track to become a $1.3T–$1.8T market by 2032, growing at 42–43% annually. Bloom Energy +157% YTD. Marvell +58% YTD. Energy and custom silicon are where the money is moving. Meta launched Muse Spark on April 8, its first proprietary AI model, breaking from its open-source Llama tradition. NVIDIA released open-source AI models, opening frontier capabilities beyond closed, paid APIs. Broadcom and Meta announced a 2nm custom AI chip partnership on April 14, supporting multi-gigawatt compute at scale.

|

|

|

TOP STORY |

OpenAI's $122B Round Changed the Rules |

Here's something most people haven't fully processed: OpenAI is no longer just a tech company. At an $852 billion post-money valuation, it's now the most valuable private company in history. More valuable than most Fortune 100 firms that have been around for a century. |

The round officially closed on March 31, with reporting spreading on April 1. Amazon committed $50 billion, with $35 billion contingent on an IPO or AGI milestones. NVIDIA pledged $30 billion. SoftBank matched that. Traditional asset managers like Fidelity, T. Rowe Price, and ARK Invest joined in. And for the first time in OpenAI's history, $3 billion came from retail investors through bank distribution channels. That last part is new. It matters more than people realize. |

But the bigger story isn't the money. It's what came with it. Amazon was named OpenAI's exclusive third-party cloud partner, with OpenAI committing $100 billion to AWS over eight years. An internal OpenAI memo dated April 13 described AWS demand as "frankly staggering" and acknowledged that Microsoft's prior arrangement had "limited our ability to meet enterprises where they are." OpenAI now generates $2 billion per month in revenue, serves 900 million-plus weekly active users, and is targeting a Q4 2026 IPO at roughly $1 trillion. |

What you might have missed: On April 13, OpenAI also acquired Hiro Finance, an AI personal finance startup. ChatGPT is moving directly into financial planning and budgeting. That's a challenge to every personal finance app on the market, and a signal about where AI is headed next. |

|

|

|

|

|

|

WHY IT MATTERS TO YOU |

Anthropic Isn't Far Behind, and That Gap Is Closing Fast |

While OpenAI grabbed the headlines, Anthropic had one of the most significant two-week stretches any private company has ever had. And most retail investors still aren't paying enough attention to it. |

On April 6, Anthropic locked in a massive 3.5 gigawatt TPU compute commitment through Broadcom and Google, with a long-term supply agreement extending through 2031. The deal was so large it triggered an SEC 8-K filing from Broadcom, the first time an AI startup's compute needs forced that kind of regulatory disclosure. Mizuho analysts estimated the arrangement would generate $21 billion in AI revenue for Broadcom in 2026 and $42 billion in 2027. Think about what that says about the scale of demand. |

Anthropic's revenue hit a $30 billion annual run rate, up from just $9 billion at the end of 2025. Over 1,000 enterprise customers are now spending $1 million or more annually. By April 14, Bloomberg reported the company had received investor offers valuing it at $800 billion-plus, more than double its $380 billion February valuation. Anthropic has so far said no. |

🔬 Expert context: Around April 7, Anthropic launched Project Glasswing, a cybersecurity initiative using an unreleased AI model that identified thousands of zero-day vulnerabilities across every major OS and browser, including a 27-year-old OpenBSD bug. Partners included AWS, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorgan Chase, Microsoft, NVIDIA, and Palo Alto Networks. The model was deemed too dangerous to release publicly. That kind of restraint, paired with that level of capability, is exactly what long-term institutional trust is built on. |

|

|

|

|

THE BIG PICTURE |

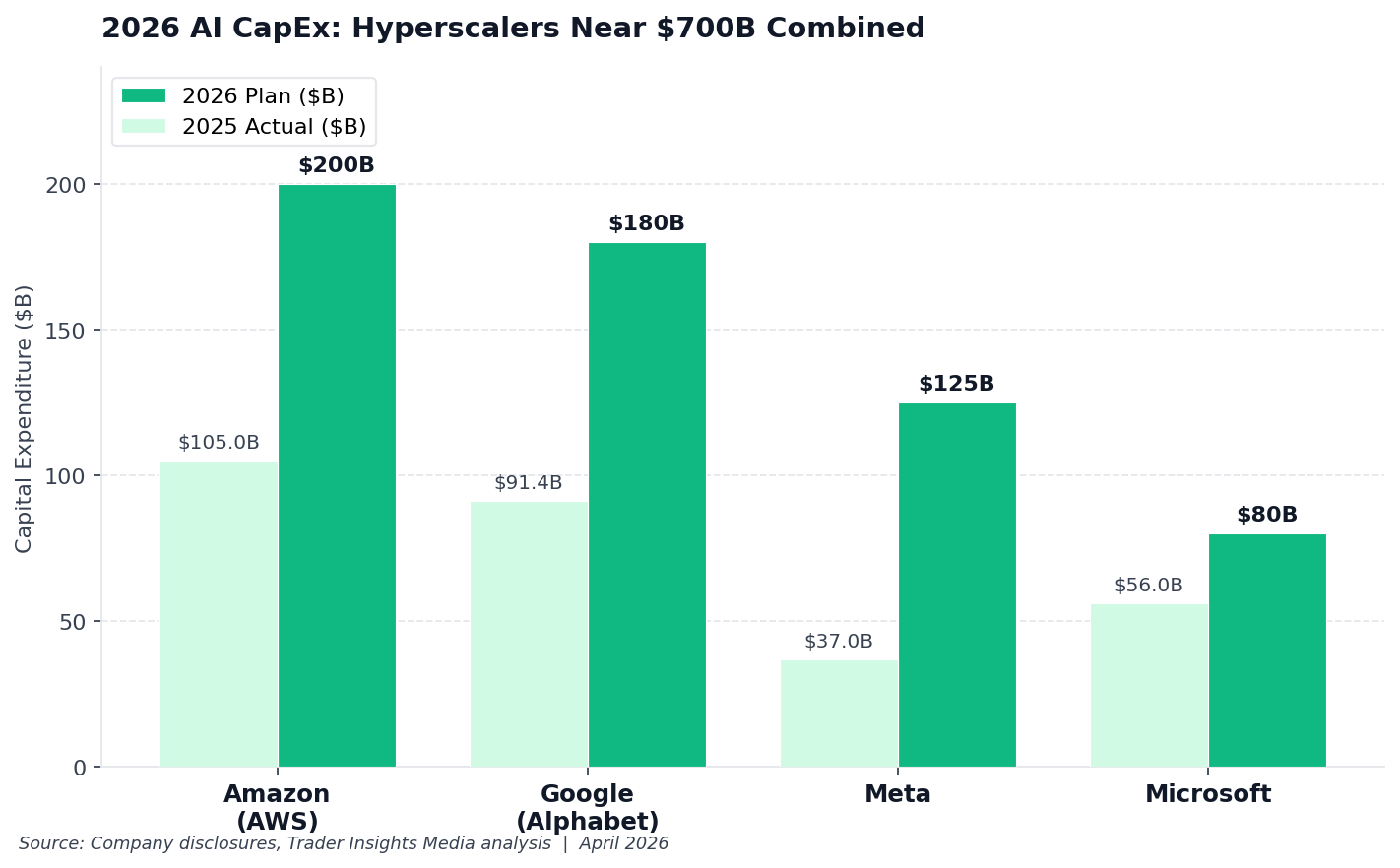

$700 Billion. One Year. Four Companies. |

Let's talk about the hyperscalers, because this is where most retail investors already have exposure, and probably don't realize how significant this moment actually is. |

Amazon plans roughly $200 billion in CapEx for 2026, detailed in CEO Andy Jassy's April 9 shareholder letter. AWS AI revenue already exceeded a $15 billion annual run rate in Q1, and Amazon's custom silicon business crossed $20 billion in annual revenue. On April 14, Amazon also announced the $11.57 billion acquisition of Globalstar, gaining satellite fleet and spectrum licenses, alongside a new agreement with Apple to power iPhone and Apple Watch satellite services through its Leo network. That's a direct counter to SpaceX's Starlink. |

Google is targeting $175-185 billion in CapEx, nearly doubling 2025's $91.4 billion. On April 9, it announced a multi-year chip partnership with Intel, committing to deploy Xeon 6 processors across global AI data centers. Meta budgeted $115-135 billion for 2026 and, on April 14, expanded its Broadcom partnership to co-develop the first 2nm AI compute accelerator under the MTIA program. Microsoft is spending aggressively across Singapore ($5.5B on April 1), Japan ($10B on April 3), and Norway (30,000 NVIDIA Vera Rubin GPUs secured April 14). Together, these four are approaching $700 billion in a single calendar year. |

To put that in context: the entire US defense budget is roughly $850 billion. Four technology companies are collectively spending nearly as much on AI infrastructure as the US government spends on its military. That's not a tech story anymore. That's a structural economic shift. |

|

|

⚠️ Worth knowing: Google's TurboQuant algorithm, released in early April, demonstrated a 6x reduction in memory usage for AI inference. That directly rattled memory chipmaker stocks. Innovation inside the hyperscalers can move the companies that supply them, sometimes in the wrong direction. Watch for that dynamic as the year progresses. |

|

|

|

|

BY THE NUMBERS |

The Data You Need to Know |

|

|

$200B+ in AI deals announced or closed between April 1 and April 15 alone ~$700B combined hyperscaler CapEx committed across Amazon, Google, Meta, and Microsoft for 2026 $852B OpenAI's post-money valuation after the March 31 close, the largest private company ever $30B/year Anthropic's annual revenue run rate as of April 2026, up from $9B just four months earlier $1.3T–$1.8T projected generative AI market size by 2032, growing at a CAGR of 42–43% per year 10–12% share of total IT hardware, software, services, advertising, and gaming spend that AI is expected to represent by 2032 +157.56% Bloom Energy YTD return as of April 15, hitting $223.79 on the Oracle fuel cell expansion deal announced April 13 +58.84% Marvell Technology YTD return following NVIDIA's $2B strategic investment announced March 31 $2.9 trillion combined valuation of AI companies expected to go public in 2026, led by SpaceX/xAI targeting $1.75T and OpenAI at roughly $1T $300B total venture capital deployed in Q1 2026, the largest single quarter ever recorded, with 80% flowing directly into AI $42.4B ASML's revised 2026 sales forecast, raised April 15 and directly citing surging AI infrastructure spending $1.3T–$1.8T projected generative AI market size by 2032, growing at a 42–43% CAGR and expected to represent 10–12% of total global IT, software, advertising, and gaming spend

|

|

|

WHAT TO WATCH |

Three Things That Matter in the Next 90 Days |

SpaceX/xAI IPO |

The roadshow timeline was disclosed April 6, targeting a $75B raise at a $1.75 trillion valuation. If it prices anywhere near that, it would be the largest IPO in history, and the first time retail investors can own Grok AI directly. |

Energy as the Bottleneck |

Data centers need power at a scale the grid wasn't built for. Oracle just expanded its Bloom Energy deal to 2.8 gigawatts of fuel cells. SoftBank broke ground April 7 on what may be the world's largest AI data center, on leased Department of Energy land in Piketon, Ohio. |

The Custom Silicon Race |

Meta is building 2nm chips with Broadcom. Google is partnering with Intel on data center processors. SiFive raised $400M the week of April 7 to challenge ARM's dominance. The chip supply chain is being rewritten in real time, and not everyone in the old playbook survives. |

|

|

THE BOTTOM LINE |

This isn't a bull run in AI stocks. It's a structural reconstruction of the technology industry, funded at a scale that rivals national defense budgets. |

The companies selling infrastructure, power, and chips into this buildout, not just the AI labs writing the press releases, are where the less-obvious opportunities sit. |

The IPO wave coming later in 2026 will give retail investors access that has never existed before. |

The window to understand these companies before they go public is right now. |

Use it. |

|

|

|

|

| |

| |

Quick ratingHow was this one? |

|

|

|

|

|

| |

|

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions. |

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers. |

**Please read the offering circular and related risks at invest.modemobile.com. This is a paid advertisement for Mode Mobile’s Regulation A+ Offering. |

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur. |

The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period. |

Pro forma revenue and EBITDA, includes full year numbers of the businesses acquired throughout 2025. |

|

|

|

Tidak ada komentar:

Posting Komentar