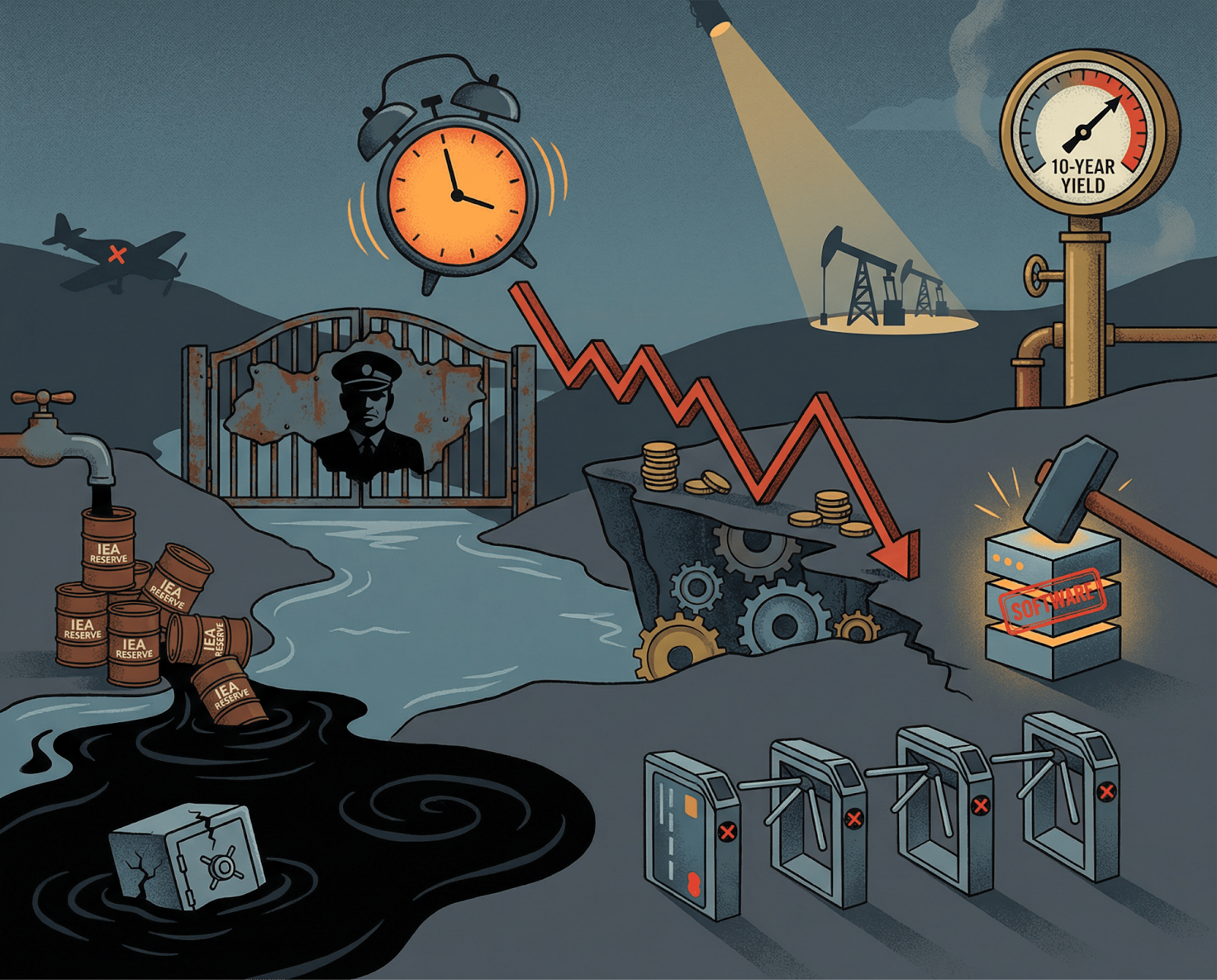

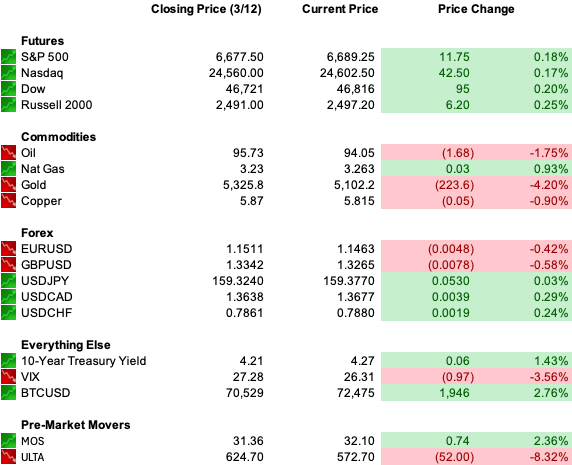

| TQ Morning Briefing | January PCE lands this morning, the Fed's last inflation read before Tuesday's FOMC decision. Brent closed above $100 for the first time since August 2022 after Iran's new supreme leader declared the Strait stays shut. The IEA's record 400-million-barrel release was absorbed in a single session. Four private credit funds have gated in four weeks. Today's PCE number was routine three weeks ago. Now it answers one question: does the Fed have any room left. | | | | | | | The market that closed at its 2026 low and didn't bounce | The S&P 500 settled Thursday at 6,672. The Dow broke below 47,000. Selling accelerated into the close. Futures flat to slightly negative premarket. The 10-year at 4.28%, VIX at 27.03. The market in suspension. | Market Implication | If PCE prints soft and futures hold 6,650, this session is digestion ahead of Tuesday. If PCE prints hot and 6,650 breaks, the S&P tests 6,600. That is the kind of round number where funds start reassessing positions. |

| |

| | |

| | | | | WHAT ACTUALLY MOVED MARKETS |

| |

|

| | | | One supply shock, one credit signal, and a Fed with no room | Mojtaba Khamenei stated the Strait of Hormuz would remain closed as a "tool of pressure." Brent gained 9.2% to close at $100.46, WTI settled at $95.73. The IEA's 400-million-barrel release was absorbed by noon. Drawdowns cannot move ships through a closed Strait. Goldman now assumes Hormuz flows at 10% of normal for 21 days, with recovery beginning around March 21. CME FedWatch has taken September off the table. One cut priced, in December. | Morgan Stanley capped North Haven Private Income Fund withdrawals after investors sought to redeem 11% of assets, returning $169 million, or 45.8% of requests. Blackstone, BlackRock, Cliffwater, and Blue Owl have flagged similar pressure. JPMorgan wrote down software-sector loans. These borrowers cannot get relief from rate cuts that are not coming. | Structural Setup | If Goldman's March 21 timeline holds, energy premiums begin unwinding and the Fed gets a narrow relief window. If Khamenei holds through next week, energy stays embedded. The dot plot shifts toward zero cuts Wednesday. Rate-sensitive sectors reprice at the same time. |

| |

| | |

| | | | | $1,000 into $556,454. Impossible? | I want to show you something that might make you upset. | For decades, the biggest banks in America have been using a secret account to collect an average of 29% per year, without ever telling the public. | Since 2000, this single account has turned $1,000 into over $556,454. | Not by picking stocks or timing the market. Just by parking money in an account that's averaged 29% year after year. | The big banks knew about it. You didn't. | That changes today. | Click here to see how "The 29% Account" works. |

| |

| | |

| | | | | Energy bid, everything else repriced | XOM gained 1.3%, CVX added 2.9%, OXY received a Wells Fargo double upgrade on Permian productivity. The only consistent bid all session. Airlines recorded the inverse: Delta fell 5.7%, United and American lost more than 4%, Southwest dropped over 7%. The XLE-JETS spread is the cleanest read on where this shock lands in actual cash flows. | MS fell 4.1%, BX dropped 3.6%, BLK fell 2.5%. Each private credit gate has been a separate increment of repricing. | Sector Read | Integrated energy names absorb the oil premium across production revenue and refinery margins. If partial Hormuz resumption arrives near Goldman's base case, refinery margin expansion follows. Financials with direct private credit exposure remain in the early rounds. |

| |

| | |

| | | | | The data that arrived before the war | January PCE reflects conditions before oil moved from $60 to $95 and before private credit gates appeared. December came in at 3.0% core year-over-year, above consensus. A similar print confirms inflation was re-accelerating before the supply shock. If the dot plot shifts to zero cuts Wednesday, XLRE, IWM, and utilities price that the same afternoon. | Iran began laying naval mines in the Strait from March 10-11. The US destroyed 16 Iranian minelayers, but mines already in the water are a different problem than ships above it. Goldman's March 21 recovery base case assumes physical passage resumes. Mines put that assumption directly into question. | Watch Signal | If JPMorgan's software loan writedowns spread to two or three additional major banks, middle-market software borrowers face a credit availability problem independent of the Fed. Names with 2026-2027 refinancing needs are where it surfaces first. |

| |

| | |

| | | | | | | Four gates in four weeks | Four gates across Morgan Stanley, Blackstone, BlackRock, and Cliffwater, covering more than $45 billion in assets, is not a liquidity event. When redemption requests reach 11-14% of assets, investors have concluded the risk profile has changed. JPMorgan writing down software loans confirms the thesis that repriced public software multiples last year. The wall these borrowers face is not just high rates. It is lenders who are no longer extending. | The Read | Mid-cap software names that relied on direct lending and face refinancing in 2026 or 2027 carry a tightening credit window at the exact moment their AI revenue story is most contested. It surfaces across earnings calls where the refinancing question gets asked and the answer is unsatisfying. |

| |

| | |

| | | | | Economic Data: PCE, GDP, Durable Goods, Personal Income and Spending, JOLTs Job Openings, Michigan Consumer Sentiment | Earnings: No notable reports | Overnight: Nikkei -1.16% | Shanghai -0.82% | FTSE -0.24% | DAX -0.47% |

| |

| | |

| | | | | | | | | January PCE prints before the open. Whatever it shows reflects an economy that did not yet have oil at $95, four private credit gates, or a Strait closed for two weeks. The data is pre-war. The market is not. | If core PCE comes in at or above 3.0%, rate-sensitive sectors that have been holding lose their last argument for patience. | If it prints below 2.8%, the Fed can signal patience. But that debate closes quickly if Khamenei speaks before Tuesday morning. | The question today's number cannot answer is how a supply shock that arrived after the data was collected changes the trajectory the Fed is actually navigating. The market answered in the futures: flat, no conviction. That is not a settled position. It is the market holding its breath. |

| |

| | |

|

|

Tidak ada komentar:

Posting Komentar