August 30, 2024

Don't Cheer the Cuts … Yet

Dear Subscriber,

|

| By Juan Villaverde |

Fed Chair Jerome Powell’s recent Jackson Hole speech has everyone buzzing about interest-rate cuts.

To sum up: The Fed wants to shift its focus from taming inflation to boosting employment.

So, those much-anticipated rate cuts could start as soon as September.

Before you pop the champagne, though, let's remember one thing: Inflation is still above the Fed’s 2% target.

While Powell’s pivot might seem like a reason to celebrate, it could come back to haunt them.

My prediction: By early 2026, the Fed could find itself in the hot seat and face tough questions about its credibility as it tries to juggle these conflicting priorities.

But that’s a problem for another day. Let’s stay focused on the immediate future.

There’s a lot of hype around these impending rate cuts. Some folks suggest they could even be a boon for risk assets.

I’m not one of them. Unless you’re into buying bonds, these rate cuts aren’t likely to move the needle at all.

That’s because the Fed doesn’t set rates in a vacuum. It follows the lead of the 2-year U.S. Treasury rate.

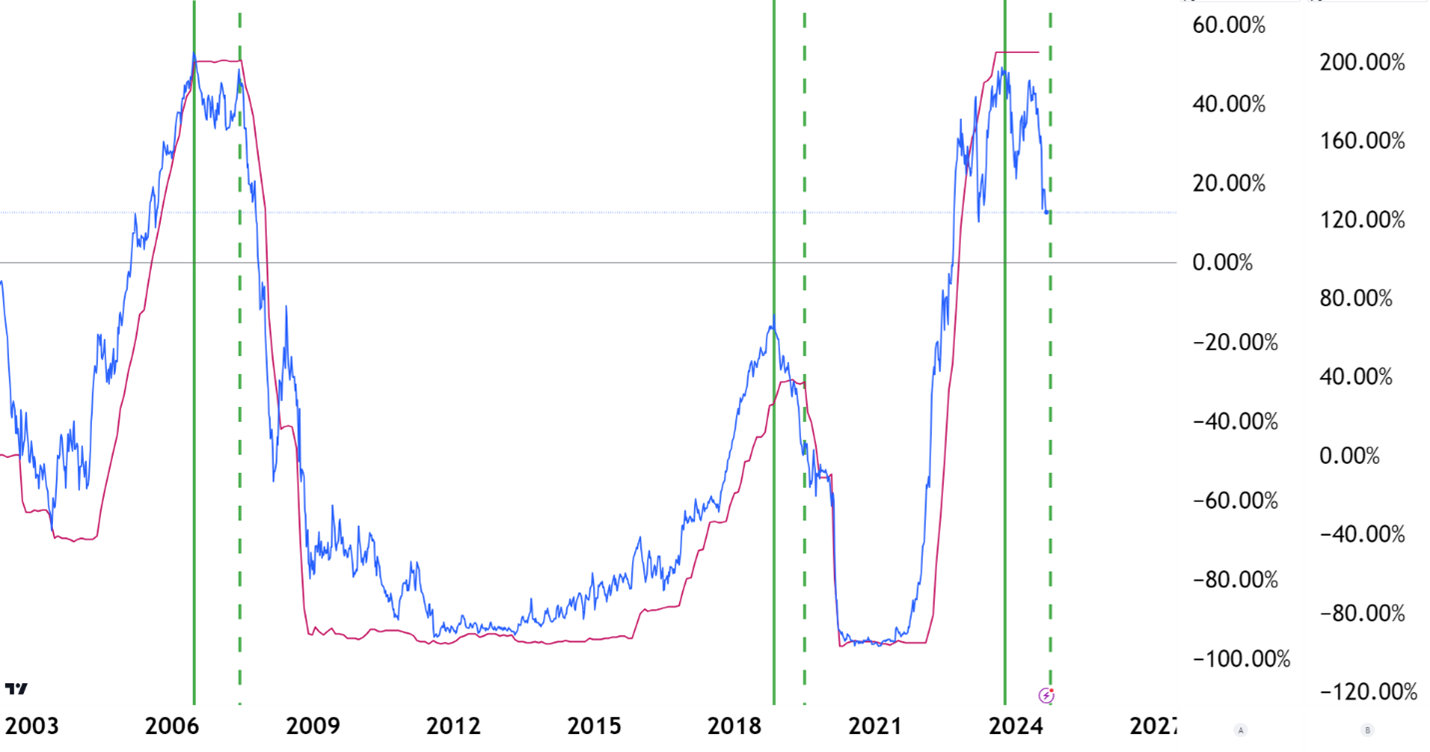

Take a look the chart below. It’s the weekly chart of the U.S. 2-year Treasury rate — in blue — compared to the Fed funds rate in purple.

The green vertical lines? They mark the last three Fed rate-cutting cycles and the peaks in the 2-year Treasury rate, including this one.

Here’s the pattern I see: The Fed starts cutting rates after the 2-year rate tops out.

Every. Single. Time.

The chart above only shows the past 20 years. But this pattern has been consistent since the 1980s.

The Fed isn’t the trailblazer here. It is just following the bond market’s lead. When investors start buying short-term U.S. Treasury bonds and the 2-year rate drops, the Fed inevitably follows suit.

It’s the same story when rates are on the rise. The 2-year rate began its climb in February 2021 — a full year before the Fed started hiking rates.

This isn’t a new phenomenon. It’s just how the system works.

Sure, markets rallied after Powell’s speech. But as crypto analyst Arthur Hayes wisely noted, “That’s just a sugar high.”

The real sustenance for markets is liquidity. And so far, the Fed hasn’t been serving it up.

But don’t worry. Liquidity is on its way, and likely before year’s end. That’s because as the U.S. nears its debt ceiling in early 2025, the Treasury will likely inject cash into the economy to speed up negotiations and avoid prolonged gridlock.

As for crypto, we saw Bitcoin (BTC, “A”) and other leading assets spike after the Fed’s dovish turn.

But let’s not kid ourselves. That’s just a knee-jerk reaction. There’s no direct correlation between the Fed funds rate and crypto prices.

For example, the entire 2015-2018 crypto bull market — which is still the biggest in history — unfolded while the Fed was hiking rates.

Some might argue that the last bull market, which began in early 2019, was fueled by a Fed cutting cycle.

That’s not quite true.

In reality, the crypto markets peaked when the Fed started cutting rates in mid-2019. It wasn’t until March 2020 that the Fed started to print money and boost liquidity. When that happened, the crypto market went back into bull mode.

The real catalyst for crypto markets is the upcoming surge in liquidity that is expected between now and the end of the year.

That’s what you should be watching.

Or just keep checking in with the Weiss crypto ratings team here every day. We’ll tell you when that liquidity starts pouring in. And we’ll cover the cryptos most likely to catch it.

Best,

Juan Villaverde

Tidak ada komentar:

Posting Komentar