Unlock the Secret to Better Options Trading |

|

One thing that many traders get wrong when it comes to options trading is their strategy selection. |

They'll buy straight calls (or puts) when trading directionally vs. trading spreads… |

Or do spreads when they should be buying outright options. |

Throughout my career I've seen millions of trading accounts…and I can't tell you how much money was left on the table. |

A LOT. |

So what do you need to know to level up your options game? |

First, you want to pay attention to the options implied volatility. |

This tells us how much the options market is expecting a specific stock or ETF to move. |

For example, if you take a look at red-hot Tesla you can see some interesting things in the options market. |

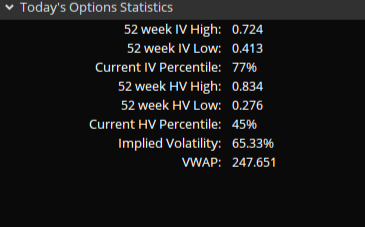

The current implied volatility for Tesla options is 65.3%. |

Implied volatility is expressed in annual terms, which can be hard to grasp. |

But if you take the annualized implied volatility and divide it by 15.87, which is the square root of the number of trading days in a typical year (252) you can convert it to implied daily volatility. |

In this case the daily options implied volatility is 4.1% |

And while it has moved higher than that a few times this week, you have to ask yourself, is it sustainable? |

To better answer that question, it's best to compare the implied volatility to what it's done over the last year. |

|

You can find this on the thinkorswim platform for free, and most option trading platforms offer it as well. |

The 52-week high implied volatility for Tesla options is 72.4%...and our current implied volatility is 65.3%. |

In other words, option volatility in Tesla is relatively high. |

In fact, it's in the 77% percentile. |

Equipped with this knowledge, you probably don't want to buy outright options. If you have a directional bias, a spread trade is a better bet based on the current volatility. |

However, there's another reason why trading a spread is better, especially if you are bullish Tesla right now. |

It's called Skew. |

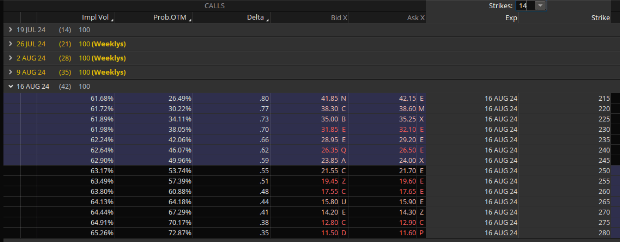

Most equities have a negative skew. |

That means the farther OTM calls have a lower implied volatility than the atm money options. |

Why? |

Because institutions who own the stock sell calls against their stock to collect premium and hedge some of their risk. |

The selling of calls makes the implied volatility go down in OTM options. |

However, that's not what we are seeing with Tesla options right now. |

Tesla call options have a positive skew. |

In other words, institutions aren't selling calls in OTM options, they are actually buying them. |

The buying pressure is causing the OTM call options spike in implied volatility. |

|

This makes it even more advantageous to buy call spreads if you're bullish. |

Because you are selling the more expensive option and collecting a bigger premium. |

I believe if you start analyzing implied volatility and skew into your decision making it will make you a better options trader. |

|

To your success, |

Don Kaufman |

P.S. 90% of all trades are placed by algorithms. If you could better understand how they move utilizing the power of AI, do you think it would make you a better trader? Click here to learn more. |

P.P.S. I was on TheoTrade Live this morning discussing Tesla and a whole lot of other topics with Brandon and Blake. If you missed our session, you can catch the replay here. |

Tidak ada komentar:

Posting Komentar