April 29, 2024

What You Know About Interest Rates Is Likely Wrong

Dear Subscriber,

|

| By Gavin Magor |

Since we’ve been getting too-hot inflation reports lately, the market has dipped in a big way this month.

The rationale being that hot inflation means the Federal Reserve will delay any potential rate cuts.

In fact, many are now suggesting that the earliest one could show up would be September. And three for the year might be out the window completely.

That’s bad news for the market. And higher rates are definitely bad for the economy. But wait …

Is everything we’re being told about interest rates actually backward? Are higher interest rates actually now keeping this economy hot?

It’s one of the pillars behind the fascinating macroeconomic theory known as modern monetary theory, or MMT.

But first, some background context … Fed Chairman Jerome Powell did his best imitation of former President Richard Nixon at the Washington Forum on April 16th when he “made things perfectly clear.”

“There has been a lack of further progress this year on inflation — the recent data have clearly not given us greater confidence, and instead indicate that it’s likely to take longer than expected to achieve that confidence.”

Mind you, that wasn’t the first time Powell told it straight, and it likely won’t be the last.

When Wall Street lacks clarity or doesn’t want to believe the motivation or reasons behind actions, minds tend to wander. And like clockwork, theories surrounding why the Fed isn’t lowering rates came out of the woodwork.

I’ll admit that while I’m not a disbeliever, I’ve been known to offer my opinions very freely.

I've talked about this theory before on why the economy continues to strengthen in the face of rate hikes — a key reason for Powell’s stubbornness.

And I was delighted to read a Bloomberg article last week that mirrored my thoughts, calling it a “fringe economic theory.” In a nutshell, I proposed that higher interest rates were stimulating the economy rather than restricting it.

Here we are around four months since I broached the subject, and nothing’s happened to change my mind. In fact, I’m more convinced than ever with ongoing GDP growth, low unemployment and strong consumer spending.

That’s all happening despite 16 months of rapid-fire interest rate hikes that in any other time in history would’ve snuffed out a hot economy, not fanned the flames.

After all, the primary motivation for shifting monetary policy from loose to tight has been to reel in high inflation. The consequences of doing so are intended to weaken the economy, raise the unemployment rate and cause some pain for consumers.

The economy and consumers not behaving like “they’re supposed to” is keeping Wall Street on edge and looking for self-satisfying answers. To that end, I’ve read some interesting and, dare I say, pretty convincing theories behind today’s conundrum — and what might come next as a result.

I’ll do my best to explain clearly, starting with reasons behind consumer resiliency.

As has been the case for some time, we’re still experiencing an inversion in yields. That simply means that short-term U.S Treasuries yield more than long-term U.S. Treasures.

Investors — especially those in the largest demographic group in the U.S., Baby Boomers — are benefitting from short-term yields of 5%.

In fact, U.S. households receive income on more than $13 trillion of short-term interest-bearing assets, almost triple the $5 trillion in consumer debt. Excluding mortgages, that translates to a net gain for households of some $400 billion a year.

Another factor supporting resiliency might be that a lot of Americans secured dirt-cheap rates on their 30-year mortgages during the pandemic. That protected many homeowners and those who refinanced from the pain of rising rates.

On top of that, Americans tucked away trillions of dollars in excess savings during the pandemic, largely due to a steady stream of Covid-19 relief/stimulus checks from Uncle Sam. Oh, and extended unemployment checks helped, as well.

But stubbornly high prices for the most basic needs and services have forced many people to dip into savings and even retirement accounts. So, while whatever excess is left presents some near-term strength for the economy, it leaves consumers more financially vulnerable.

And as would be expected when folks are dipping into savings to pay bills, the rate of personal savings has dropped precipitously.

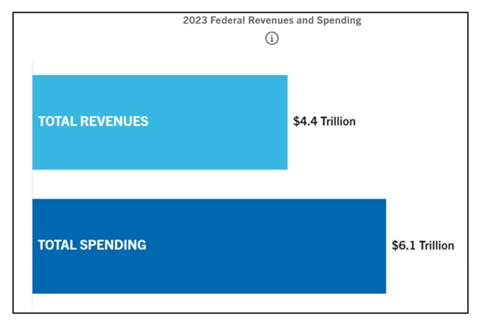

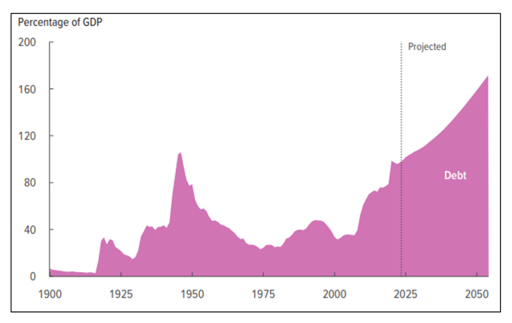

The kicker: The government is spending more than ever, putting the U.S. in a position we’ve only experienced a few times in history — leading up to the Great Depression in 1929 and during the Great Financial Crisis in 2008.

Uncle Sam is literally spending more than the U.S. gross national income resulting in an unenviable negative savings rate. That’s akin to you and me spending tirelessly regardless of what we make or owe to lenders.

Of course, the government uses its unique money-printing powers to bail itself and our economy out. That practice has come back to bite us many times over the decades (i.e. bailing out major banks and handing out Covid-19 relief without much discretion as to who received it).

This is one time I hope history doesn’t even rhyme, let alone repeat itself. But something needs to give for that not to happen.

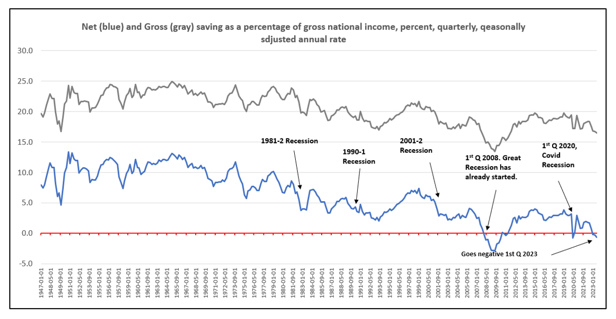

In general, net saving tends to fall steeply in the early periods of recessions. You see that in the below graph.

But one thing is clear: Net saving has worsened rapidly since Q4 2020, dropping from 2.9% in that quarter to -0.7 percent in Q3 2023. Such a rapid drop virtually always indicates the U.S. has either entered a recession or will soon enter one.

And besides out-of-control spending, paying higher interest rates to pay debt only compounds the imbalance challenges.

This year, federal government interest costs are on pace to become higher than the entire U.S. defense budget.

Plus, interest costs — and mandatory spending programs like Social Security, Medicare and Medicaid — are growing so fast that spending won’t shrink as a percentage of the economy going forward. And they're projected to remain higher if nothing is done to change it.

So, on one hand, lowering interest rates might benefit the government. However, it could, if done prematurely, grind the economy to a halt.

One thing I strongly urge is for all investors to continue using all of our investment ratings to stay up to date on the markets. Our main goal is to help investors achieve the best profits and safety no matter what craziness the Fed throws our way.

Cheers!

Gavin

P.S. Another way to achieve profits and safety is to come to this special, exclusive and free gala event. Dr. Martin Weiss is unveiling something on Tuesday, May 7 at 2 p.m. Eastern that he calls “the crowing achievement of his 53-year career and the 100-year legacy of his father’s life work." You can get your ticket by signing up here.

Tidak ada komentar:

Posting Komentar