June 25, 2023

Crypto Dollar Stablecoins Backed by LSD

Dear Subscriber,

|

| By Chris Coney |

No one has yet cracked the idea of a fully decentralized crypto dollar stablecoin.

Although there have been a few attempts, none of them have delivered.

Single Collateral DAI

Now, the original idea behind Dai (DAI, Stablecoin) was to mint it as a debt instrument collateralized against Ethereum (ETH, “B”) locked in the MakerDAO smart contract.

Overall, it worked alright. But the main concern with a stablecoin fully backed by a variable price crypto asset is … well, the variable price crypto asset.

Crypto markets were — and still are — wildly volatile, which makes using crypto assets as collateral a high-risk game.

Even with minimum collateral ratios of 150%, there’s still the chance that a 33% drop in the value of the collateral liquidates the position.

Of course, you could post much more collateral. But then you’re locking up an increasing amount of capital to mint the stablecoins that you’re going to invest.

And at that point, the yield may not end up being worth it.

So, the DAI stablecoin is now a multi-collateral stablecoin that is partially backed by USD Coin (USDC, Stablecoin).

TradFi-Backed USDC

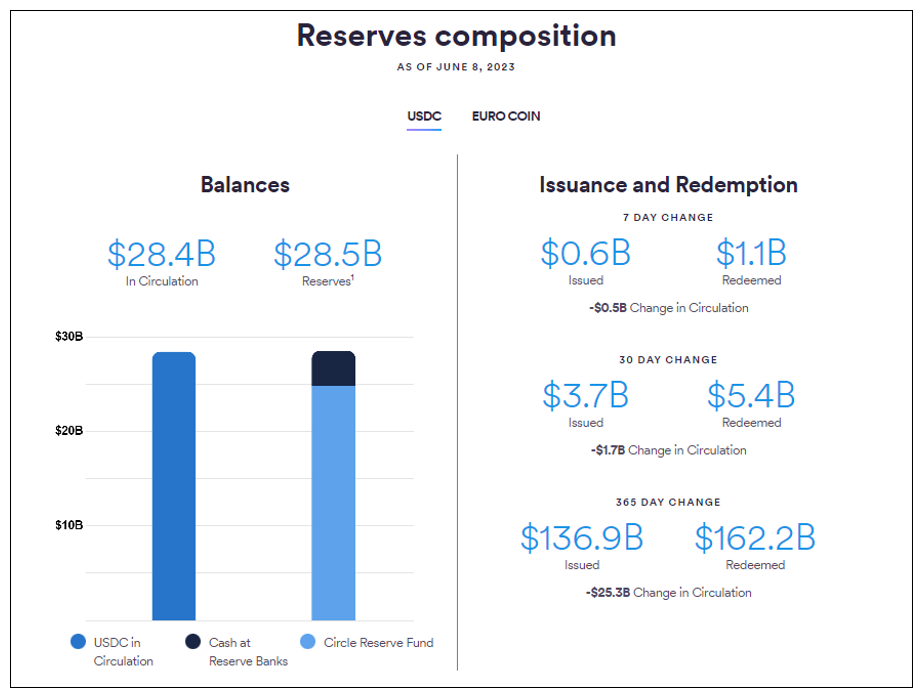

USDC is a crypto dollar stablecoin issued by Circle. This is a company that custodies the U.S. dollars you send them and issues you USDC in return.

This then means that each USDC token has one U.S. dollar it can be redeemed for in the traditional financial system.

There is no chance of liquidation in this model, since the stablecoin isn’t exactly a debt instrument.

Even if you consider it to be one and say USDC is being borrowed and collateralized with U.S. dollars, it is still 100% backed by an asset that does not fluctuate in price at all … because it’s the U.S. dollar.

However, the downside of stablecoins that are backed by assets in the TradFi system is that they lack the decentralized aspect of decentralized finance.

In this case, there is a great big point of centralization because Circle custodies the entire $28 billion of assets backing the 28 billion USDC in circulation.

Stablecoins Backed by LSTs

Ever since the Ethereum network transitioned from proof-of-work to proof-of-stake mining, an opportunity to earn yield on your ETH tokens in a decentralized way popped up.

Now that miners have been replaced with validators, anyone can stake Ethereum on a validating node and earn a share of newly minted ETH and transaction fee revenue.

At time of writing, approximately 10% of the ETH tokens in circulation are locked in any one of several staking contracts.

This is an enormous amount of ETH that is sitting there doing nothing except earning yield.

So, why not do something else with all that capital, like backing a stablecoin?

Enter Prisma Finance

It’s a clever name — Prism with an “a” on the end.

This is because it wraps up the concept of the project nicely. Namely, it absorbs all the “colors” (various staking derivatives) and produces one perfect white light (the backed stablecoin).

I also noticed that while traditionally we refer to them as liquid staking derivatives, Prisma has opted to refer to them as liquid staking tokens.

At launch, you’ll be able to take any of the receipt tokens that represent the ETH you have staked with your chosen provider, such as:

• Lido Finance’s (LDO, Not Yet Rated) wstETH

• Coinbase’s (COIN) cbETH

• Rocket Pool’s (RPL, Not Yet Rated) rETH

• Frax Finance’s (FRAX, Not Yet Rated) sfrxETH

• Binance’s WBETH

Then, you can borrow the new acUSD stablecoin against them.

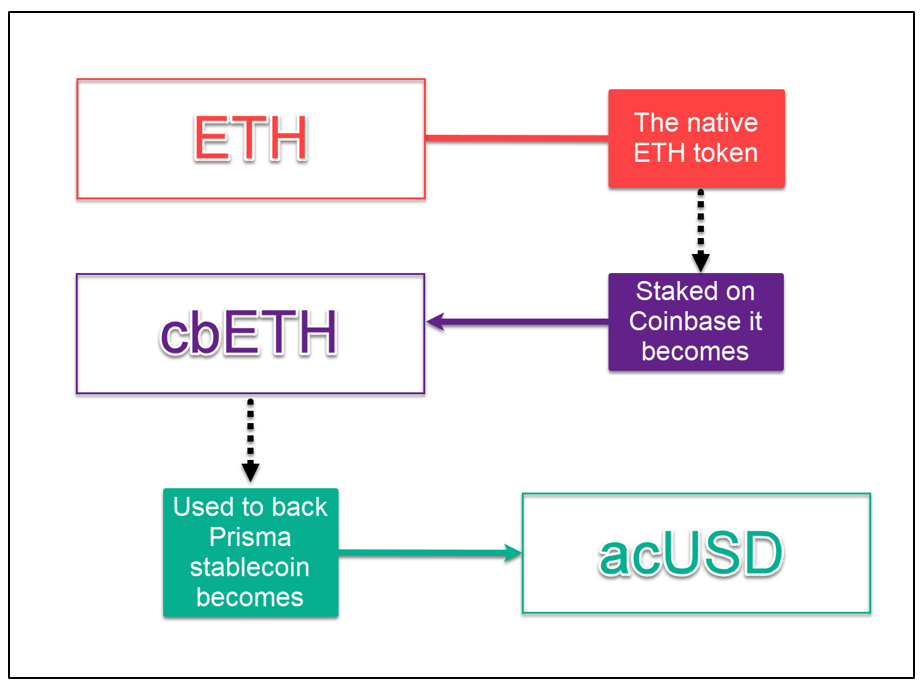

As we are in the realm of crypto derivatives, I drew this diagram to break down what is happening:

From this image, you can see how there are three layers to the acUSD stablecoin.

First, ETH is the base layer token on the Ethereum network, which is used to pay transaction fees.

Next, cbETH is a token that represents ETH staked on Coinbase. This token could be used to redeem the deposit.

And finally, acUSD is a stablecoin that is borrowed into existence against cbETH (or any of the other receipt tokens listed earlier).

Conclusion

Is this project really going to work?

After all, you may have noticed that the Prisma model looks awfully similar to the original DAI model: a stablecoin backed by a variable price asset, ETH.

So, what’s the difference?

While crypto markets are still wildly volatile by traditional market standards, they are less so than they were when the original DAI model was conceived. But that’s just one part of it.

Another important distinguishing feature is that Prisma is a fork of Liquity (LQTY, Not Yet Rated).

Liquity is a project like the original DAI where you borrow LUSD against ETH at 0%.

What is innovative about Prisma’s approach is that the collateral underlying the acUSD loans are yield-bearing assets!

That means cbETH is going up in value against ETH due to the yield on the underlying staked ETH.

Over a long enough time, an acUSD loan you take out on Prisma should eventually pay itself off automatically.

And in the interim, your loan-to-value ratio should be gradually and automatically getting better, thanks to the underlying yield from the staked Ethereum.

It’s a very subtle change to the way Liquity works, but greatly changes the economics.

Prisma is an incredibly new project and only created a Twitter account in May 2023. So, we really are on the cutting edge here.

Let’s keep an eye on this because it could be a good one.

But that’s all I’ve got for you today. Let me know what you think about Prisma, and if you think it will succeed by tweeting @WeissCrypto.

I’ll catch you here next week with another update.

But until then, it’s me, Chris Coney, saying bye for now.

Tidak ada komentar:

Posting Komentar