| TQ Morning Briefing | Risk Priced, Not Pressed | | | | | | Markets are closing a record year without urgency. | U.S. equity futures are modestly lower this morning, extending a quiet drift that has defined the final sessions of 2025. | Indices remain near all time highs, participation is thin, and price action is muted. That is not stress. It is supervision. | This is a market ending the year fully invested, but no longer pushing. | The most important signals are again coming from outside headline equities. | Precious metals are violently repricing leverage rather than belief. Rates remain pinned. The dollar is soft. Liquidity is thinning into the holiday close. | Risk is still on. | But it is being priced carefully, not pursued aggressively. |

| |

| | |

| | | | | | | WHAT'S ACTUALLY MOVING MARKETS |

| |

|

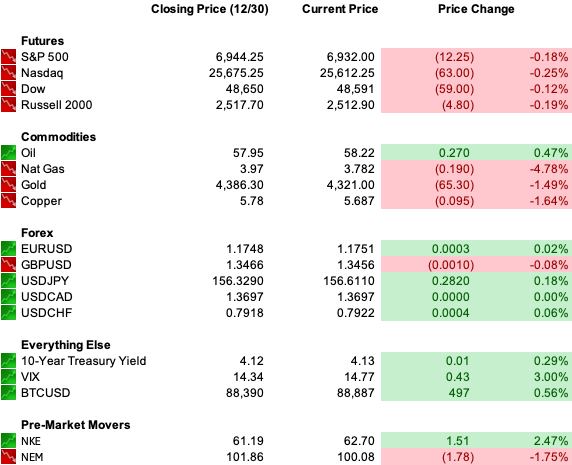

| | | Metals Are Repricing Constraints, Not Conviction | Silver is down sharply this morning after the CME raised margin requirements for the second time in a week across precious metals contracts. Gold, platinum, and palladium are also lower. | The catalyst is mechanical, not macro. | Margin hikes forced rapid deleveraging into one of the weakest liquidity windows of the year.

The result is violent price action without structural damage. This follows a year in which silver more than doubled and gold posted its strongest annual gain in decades. | That context matters. | This is not a breakdown in demand. It is a reset in positioning. | China's decision to restrict silver exports adds another layer. The metal is being elevated from a commodity to a strategic material, placing it closer to rare earths in policy treatment. That reinforces long term scarcity even as near term leverage is flushed. | Belief remains intact. Exposure was simply too crowded. | Equities Are Holding Altitude Without Chasing | Equity futures point to a soft open on the final trading day of the year. Nasdaq futures underperform slightly. Small caps lag. Volume is light. | This is consistent with late December behavior. | The S&P 500 is up more than 17 percent in 2025. The Nasdaq has gained over 20 percent. There is little incentive to extend risk further with the calendar closing and liquidity thin. | This is not distribution. It is balance sheet management. | The Santa Claus window has not failed. It has simply stalled. | Rates and FX Reflect Governance, Not Growth Fear | The 10 year Treasury yield sits near 4.11 percent, steady and contained. The curve continues to reflect expected easing without panic. | Markets are digesting the Federal Reserve's December meeting minutes, which revealed a narrower margin behind the latest rate cut than the vote implied. | That nuance matters less than the broader signal. | Attention has shifted from rate math to governance. | The open discussion around the next Fed chair and public pressure on institutional independence are increasingly relevant inputs. | Markets are not pricing a policy shock. They are pricing sensitivity. | The dollar is on track for its worst annual performance since 2017, reinforcing the bid under commodities and non U.S. assets while quietly loosening global financial conditions. |

| |

| | |

| | | | | | Tuesday saw mild profit taking across large technology winners. | Nvidia, Tesla, Palantir, and Oracle all eased as valuation sensitivity reasserted itself near highs. | This morning's pre market action is flat to slightly lower across indices. Nasdaq underperforms modestly. Small caps remain weak. There is no forced selling. | Rates are steady. Volatility is elevated from last week but remains compressed historically. | Crypto mirrors the same theme. Bitcoin trades near 88,000, still well below its October highs and slightly down on the year. Narrative enthusiasm remains, but sustained inflows have not returned. | Across asset classes, conviction exists. Urgency does not. |

| |

| | |

| | | | Geopolitical pressure continues to rise without forcing repricing. | Geopolitical pressure continues to rise without forcing repricing. | The U.S. has intensified enforcement around Venezuelan oil flows, including the pursuit of sanctioned tankers and the disclosure of covert actions. | China has staged its largest military drills around Taiwan to date before pulling ships back.

Europe is ending the year near record highs, led by banks, defense, and value rotation. | Markets are not panicking over geopolitics. | They are normalizing it. | This is what late cycle risk pricing looks like. Friction is absorbed through positioning rather than liquidation. |

| |

| | |

| | | | Amazon's $794M Bombshell: Nvidia's Secret Partner Revealed | | Amazon has quietly poured $144 million into a secretive AI chip company — and has already committed to purchasing a staggering $650 million worth of their product. Why? Because this obscure startup holds the key to unlocking the full potential of Nvidia's revolutionary Blackwell chip. | Discover the company at the heart of the AI arms race. |

| |

| | |

| | | | Low Volatility Is a Feature, Not a Signal | Markets often misread calm as complacency. | What we are seeing instead is constraint doing its job. | Margin rules forced metals to reset. Liquidity conditions are disciplining equity behavior. Governance risk is being priced without dramatic repricing. | Capital remains deployed, but exposure is monitored. | This is how mature bull markets preserve gains. | Not through acceleration. | Through discipline. | Risk does not leave. It gets priced more carefully. |

| |

| | |

| | | | Data: Initial Jobless Claims

Earnings: No notable reports

Overnight: Nikkei -0.37%, Shanghai +0.00%, FTSE 100 -0.20%, DAX +0.51% |

| |

| | |

| | | | | | This is not a market searching for a catalyst. | It is a market closing a strong year by protecting altitude. | Leverage is being reduced where it needs to be.

Governance is being priced.

Liquidity is thinning.

Risk remains on. | But nothing is being chased. |

| |

| | |

|

|

Tidak ada komentar:

Posting Komentar