Quick Market News: | Oil Reality Check: WTI crossed $100 — up 51% since the war began February 28 Nuclear Nightmare: Iran's power plant hit three times — IAEA warns of radiological catastrophe American Blood: 13 US troops killed, 303 wounded — a $270M aircraft destroyed in Saudi Arabia Your 401k Is Bleeding: Dow confirmed correction — five straight losing weeks, no bottom in sight Stagflation Is Back: Inflation hits 4.2% — the Fed may now raise rates into a slowing economy FREE BUY ALERT: 3 top stocks to own in 2026* (ad)

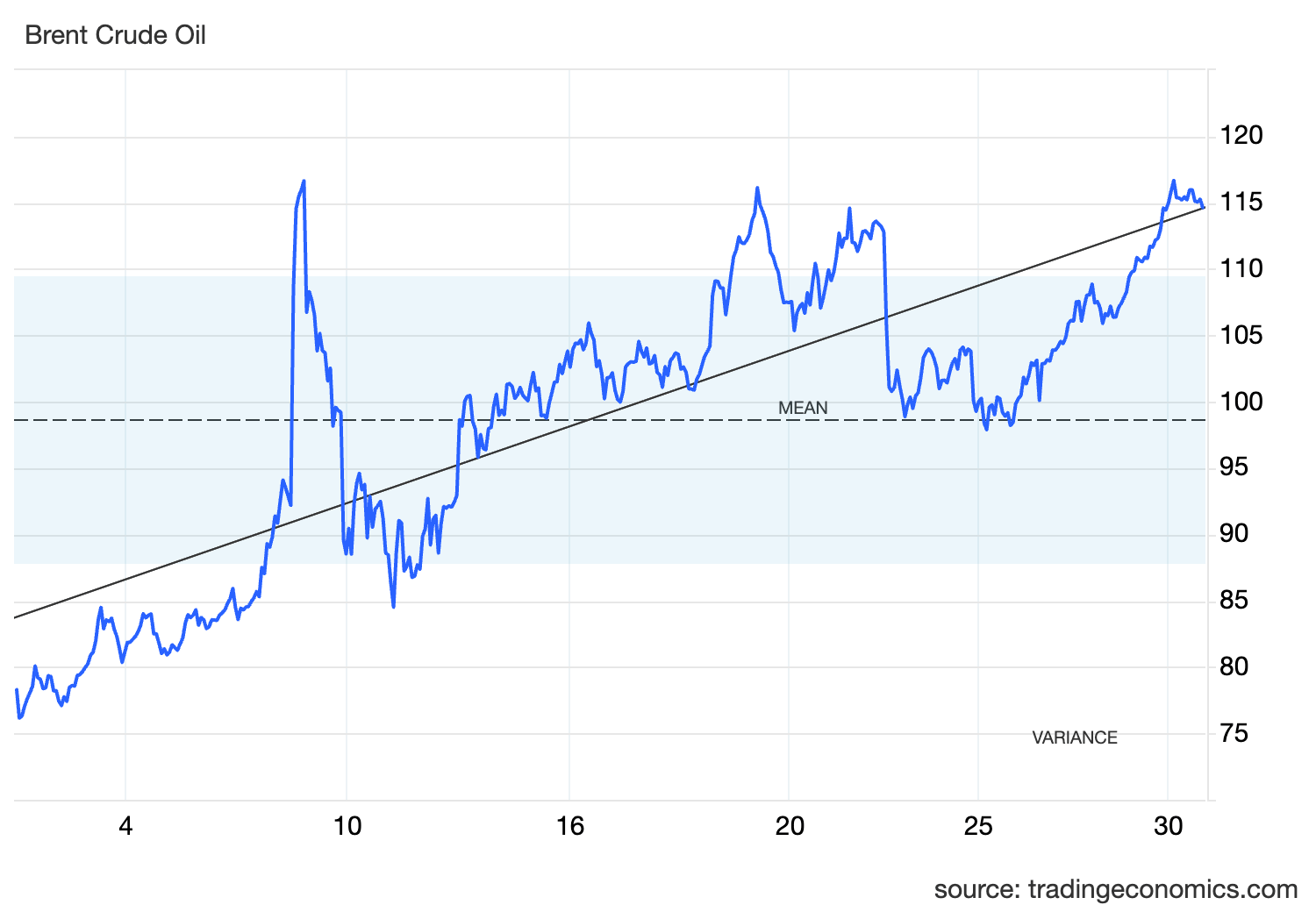

| | | | | | Block 1 of 5 | WTI Hits $101, Brent at $115 — The War Premium Is Holding | | — Top Story | WTI settled at $99.64 Friday — its first $100 print since July 2022 — and is trading $101.50 premarket. Brent is at $115. Both are holding war-premium levels going into Monday. | — Why This Matters for Investors | Every $10 rise in crude adds roughly 0.2–0.4 percentage points to US core inflation. Oil is up +51% since February 28. The OECD already revised US inflation to 4.2% from 2.8%. The Fed is now caught between fighting oil-driven inflation and a slowing economy. | WTI premarket: $101.37–$102.50, up from $67.20 at war start — a 51% surge in 29 days Brent premarket: $107.94–$116.25. Physical Dubai crude at a staggering $126/barrel Goldman Sachs forecasts Brent averaging $110 through April. JPMorgan $130 scenario: 20–25% probability

| — The Bottom Line | Do not fade oil until there is a credible Hormuz reopening timeline — and there is none today. Energy longs remain the only sector with a clear fundamental tailwind. |

| |

| | |

| | | | | | | Block 2 of 5 | Trump's Kharg Island Gambit — Leverage in Plain Sight | | — Top Story | Trump publicly threatened to seize Kharg Island — the terminal handling 90% of Iran's oil exports. The Pentagon is actively planning ground operations. The USS Tripoli with 3,500 Marines has arrived. | | ❝ | | | "Maybe we take Kharg Island, maybe we don't. We have a lot of options." | | | | President Trump, Air Force One, Sunday March 29, 2026 |

|

| — Why This Matters for Investors | Kharg seizure would cost Tehran $300–400M per day in lost oil revenue — a symmetric counter to the damage Iran is inflicting on the world via Hormuz. If seized, the US controls when Iran gets its revenues back. Hormuz compliance becomes the literal condition of return. | Washington Post (Sunday): Pentagon preparing "weeks of limited ground operations", with Kharg raids as one of three primary scenarios April 6 deadline: energy infrastructure strikes resume if Hormuz remains closed and talks stall VP Vance confirmed the war objective: "to ensure Iran is neutered for a very long time"

| — The Bottom Line | April 6 is the single most important market-moving date this week. A Hormuz signal before then crashes oil 5–8% intraday. No deal, and Brent pushes toward $120. |

| |

| | |

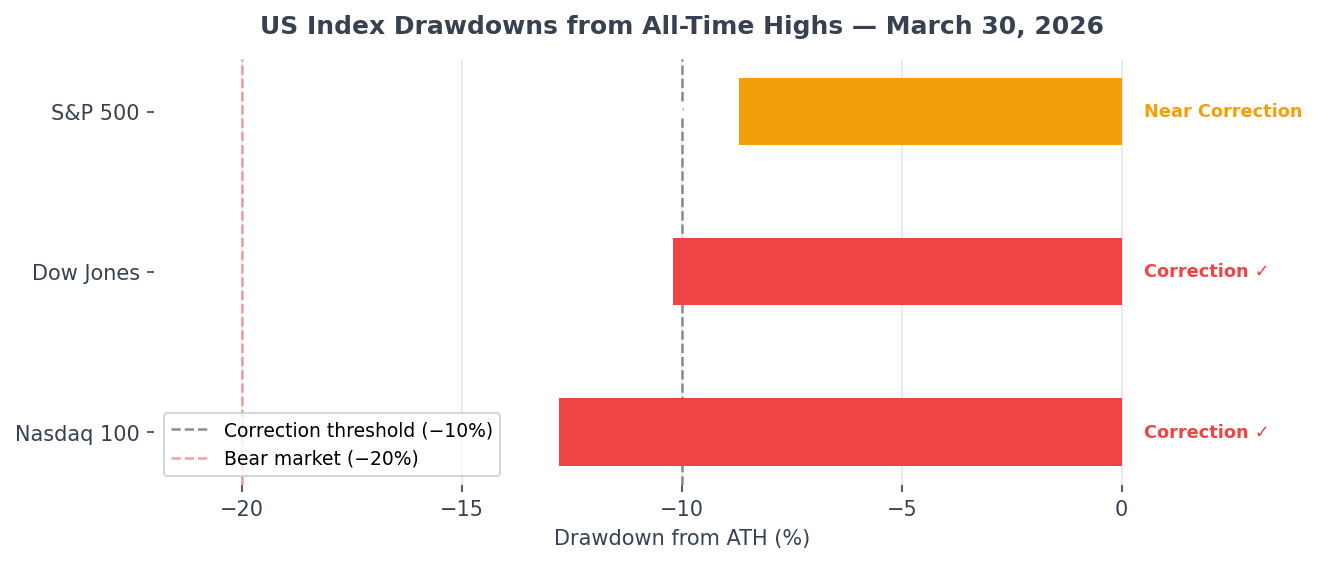

| | | | | | Block 3 of 5 | Correction Confirmed — Dow, S&P 500, and Nasdaq All Breaking | | — Top Story | The Dow confirmed a correction. The Nasdaq is down 12.8% from its October record. The S&P 500 is 8.7% off its all-time high — teetering on the edge. | — By the numbers: | Dow Jones: correction confirmed at −10.2% from ATH, closed at 45,166 (−1.73% Friday). Premarket Monday: 44,905 Nasdaq 100: −12.8% from October's all-time high — deepest correction of the three US indexes, led by tech selling S&P 500: −8.7% from ATH, 5th straight weekly loss, 7-month closing low at 6,368. Premarket: 6,334 VIX: closed Friday at 31.05 (+13.16%), firmly in the extreme fear zone (above 30). March range: 20.28–35.30

| — Why This Matters for Investors | This correction carries a structural tail-risk that normal corrections do not. A live war with no end date, a commodity shock, and a Fed that cannot cut rates without igniting inflation — all three simultaneously. The average correction (10–20% decline) lasts 17 days. We are on day five. | — The Bottom Line | Every equity rally is a short until the Hormuz question resolves. Watch the 10-year yield — the 30-year briefly broke 5.00% Friday, sending a clear stagflation signal. |

| |

| | |

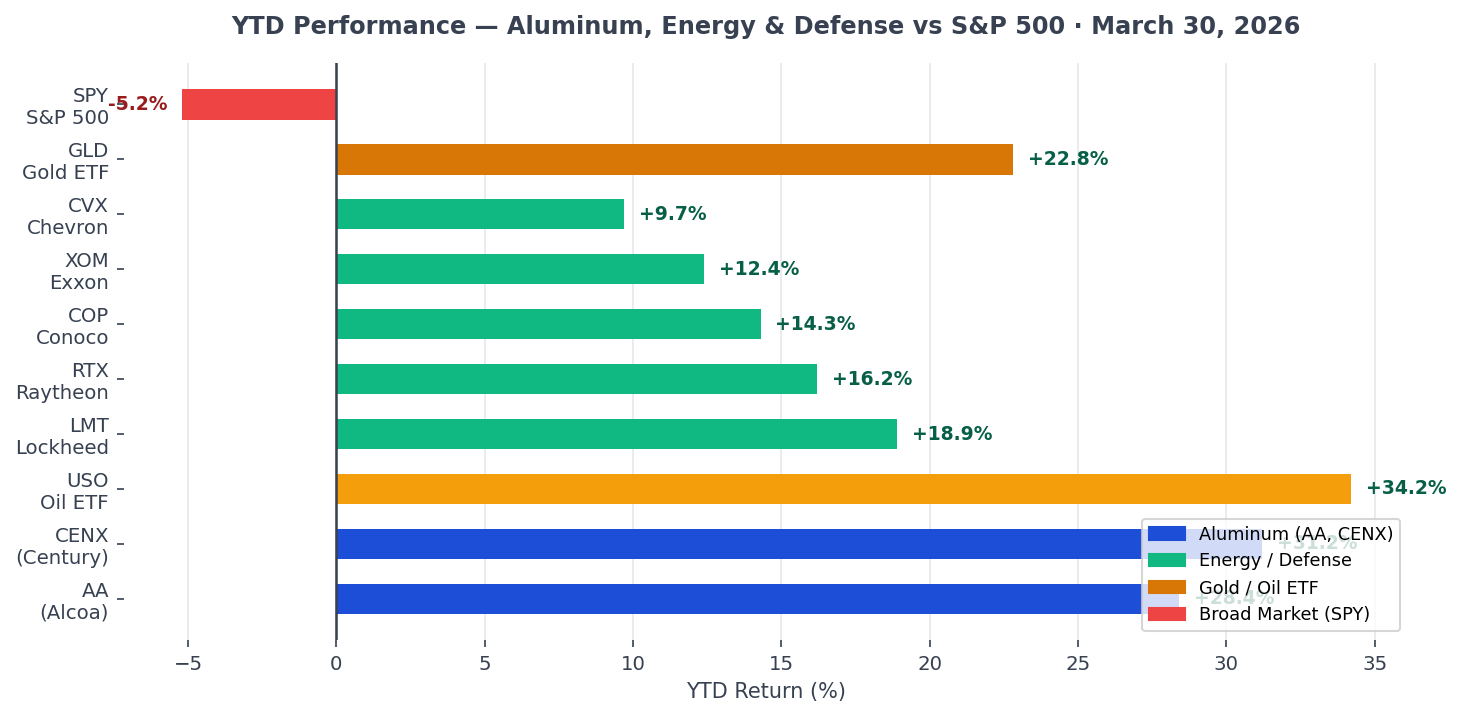

| | | | | | Block 4 of 5 | Aluminum Surges +6% — UAE & Bahrain Plants Struck, Supply in Shock | | — Top Story | Aluminum jumped +6% after Iranian forces struck aluminum production facilities in the UAE and Bahrain. Alcoa (AA) and Century Aluminum (CENX) are the direct beneficiaries — both are up 28–31% YTD. | — Why This Matters for Investors | The Gulf accounts for a significant share of global primary aluminum capacity. With those facilities offline or at risk, the LME aluminum price hit ~$3,492/ton. For US aluminum producers, this is a pure pricing windfall — higher spot prices flow directly to margins with no increase in their own production costs. | Alcoa (AA): up +28.4% YTD. Primary aluminum producer with US and international smelters fully insulated from the Gulf supply shock Century Aluminum (CENX): up +31.2% YTD. Smaller, more leveraged play on aluminum prices — highest beta to the spot price move LME aluminum: ~$3,492/ton, up +6% on the week. The commodity is bifurcating — copper is down 1.43% on recession fears while aluminum is up on supply disruption

| — The Big Picture | Industrial metals are no longer moving together. Copper signals demand destruction (down on recession fears). Aluminum signals supply destruction (up on wartime disruption). That split is the clearest picture of a stagflation commodity environment in the data. | — The Bottom Line | $AA ( ▲ 1.41% ) and $CENX ( ▲ 2.58% ) are among the few non-energy, non-defense stocks with a direct fundamental catalyst. Momentum holds as long as Gulf facilities remain at risk. |

| |

| | |

| | | | | AD | Trump's $200 Billion Revolution Changes Everything AI | With 100X faster processing power... and 90% less energy usage... current AI systems could become obsolete. And three companies control the technology that could make it happen. Discover the "Trillion Dollar Triangle" here. |

| |

| | |

| | | | | | Block 5 of 5 | Houthis Enter the War — Dual-Chokepoint Risk Is Now Real | | — Top Story | Houthis fired ballistic missiles at Israel for the first time since the war began — two waves Saturday, a third Sunday. Bab al-Mandeb closure risk is no longer hypothetical. | — Why This Matters for Investors | Bab al-Mandeb handles ~12% of global oil trade alongside Hormuz's 20%. A dual-chokepoint closure pushes Brent toward or past the 2008 all-time high of $147.50 — and JPMorgan's $130 Brent scenario jumps to 20–25% probability instantly. | Saturday: Two Houthi ballistic-missile waves at Israeli military sites. IDF intercepted both Sunday: Cruise missiles and drones hit near Eilat and Tel Aviv area — expanding the target set Prince Sultan Air Base: Iranian strike, 15 US troops wounded, E-3 Sentry AWACS destroyed. Running totals: 13 US KIA, 303+ wounded

| — The Bottom Line | Dual-chokepoint exposure is the primary tail-risk in energy markets — and it is not yet priced in. If Houthis formally announce a Red Sea closure, treat it as an immediate buy signal in energy and gold. |

| |

| | |

| | Two trades fighting each other at the open. One will win by close. | Three words define this week: oil, fear, deadline. | WTI at $101.50, Brent at $115, and a Dow in confirmed correction are the baseline. | April 6 is the hinge point — a Hormuz signal changes everything. | No deal means higher oil, deeper equity pain, and a Fed that cannot help. | Watch AA and CENX for the aluminum trade, VIX above 35 as the capitulation signal, and the Pakistan-brokered Hormuz convoy deal as the only active diplomatic off-ramp in play. | | | | | How do you like this new format? | |

| |

| | |

| | Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions.

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers. | |

|

Tidak ada komentar:

Posting Komentar