September 17, 2024

Hotter than the 'Sun'

Dear Subscriber,

|

| By Nilus Mattive |

When a CEO says shareholders paid too much for his company’s stock, you should pay attention.

That’s exactly what the CEO of the “Original Nvidia” did more than 20 years ago. I’ll get into all the details in a moment.

I’ll also tell you what to do about the “Next Nvidia” … along with the actual one.

First, let me set the scene …

It was 1999. The stock market was roaring. And I was regularly making trades to supplement my income as an intern on Wall Street.

One of my favorite targets, Sun Microsystems, was a Nasdaq darling.

Sun regularly beat Wall Street estimates. Its rapid growth came from supplying hardware and software to internet startups around the world.

In a world where a lot of high-flying companies racked up huge losses, Sun could boast about actual products and real profits.

Still, after buying and selling the stock a couple times during my senior year of college, I bought my last 50 shares in December 1999. I cashed out with one final gain on Oct. 12, 2000.

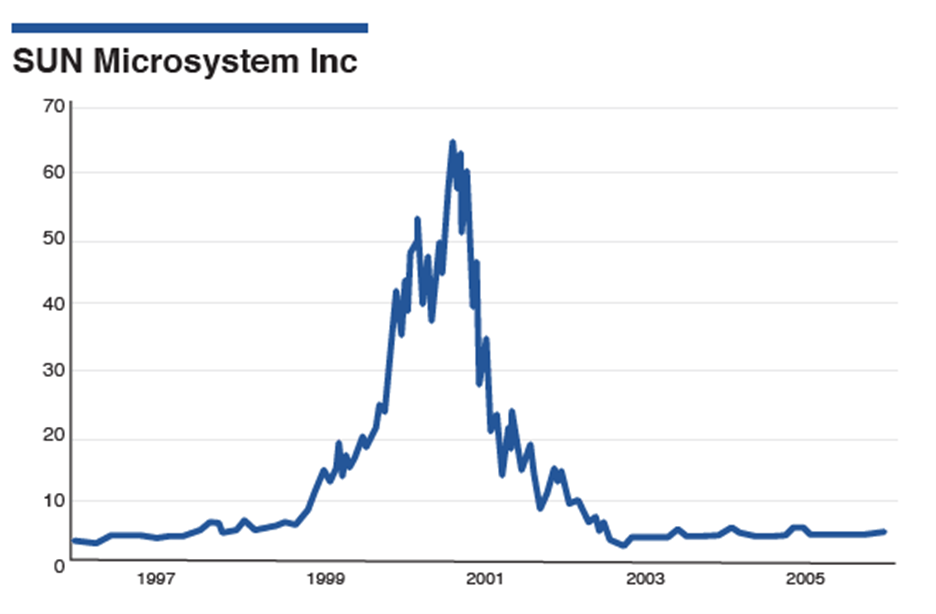

At its peak valuation, Sun was worth roughly 10 times its annual revenues. As this chart shows, that multiple didn’t hold very long …

Shares of Sun collapsed from late 2000 through 2002, from around $65 to just $5.

Shortly after that implosion, the company’s CEO — Scott McNealy — conducted a now-infamous interview with Businessweek where he explained Sun’s peak valuation:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends.

That assumes I can get that (approved) by my shareholders.

That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run-rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are?

You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Sun wasn’t the only company getting valued that way, of course.

At the height of the late ’90s tech bubble, 29 companies in the S&P 500 traded at 10 times sales.

What shocked most analysts about Sun revolved around how the company cratered in spectacular fashion despite its profitability.

This happened because, as McNealy rightly pointed out, investor expectations were so shockingly high the company really had no way to deliver into perpetuity.

When Sun’s end-users suddenly stopped needing its products, the entire house of cards came crashing back down. Oracle eventually acquired the company in 2009.

Fast forward to today.

Can you think of another company that’s:

- Growing revenues and profits by leaps and bounds …

- Enjoying unprecedented demand because of a booming new “this will change everything” trend …

- Almost become synonymous with the power of that trend itself?

I’ll give you a hint: You can’t spell its name without AI.

Nvidia (NVDA) recently traded at 34 TIMES its annual sales.

Put another way, Nvidia’s value is 340% richer than its internet-bubble counterpart at the top of that market!

What could possibly go wrong from here?

Now, I’m not saying all stocks are doomed. Or even that all tech stocks are overpriced.

But for your keep-safe money — the nest egg you can’t afford to take big risks with — you should look to companies with lower valuations.

Much lower.

They do exist, but they aren’t hiding in plain sight.

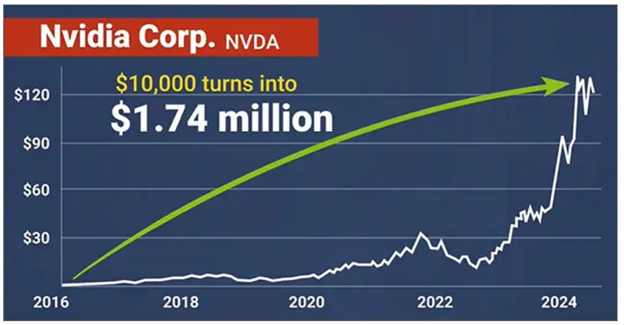

My colleague and Silicon Valley insider Michael A. Robinson has been on the hunt for “The Next Nvidia” for months.

Michael has an incredible track record when it comes to the world’s most-traded stock, along with plenty of others in the tech world. He first recommended it at a split-adjusted 80 cents. That could have turned $10,000 into $1.74 million!

Now, Nvidia may enjoy its own day in the “Sun” again. But seeing another gain like that feels like an out-of-this-world proposition right now.

So, Michael started to look elsewhere. But not just any AI tech angle for the next Nvidia would do.

He wants a good price today.

And despite the tech industry seeing higher prices than even the Dot-Com Bubble, he found something.

He says this find IS “The Next Nvidia.” And guess what? It currently trades at just 0.62 times its annual sales. That’s a 55x cheaper valuation than Nvidia itself!

I urge you to check it out here.

Best wishes,

Nilus Mattive

Tidak ada komentar:

Posting Komentar