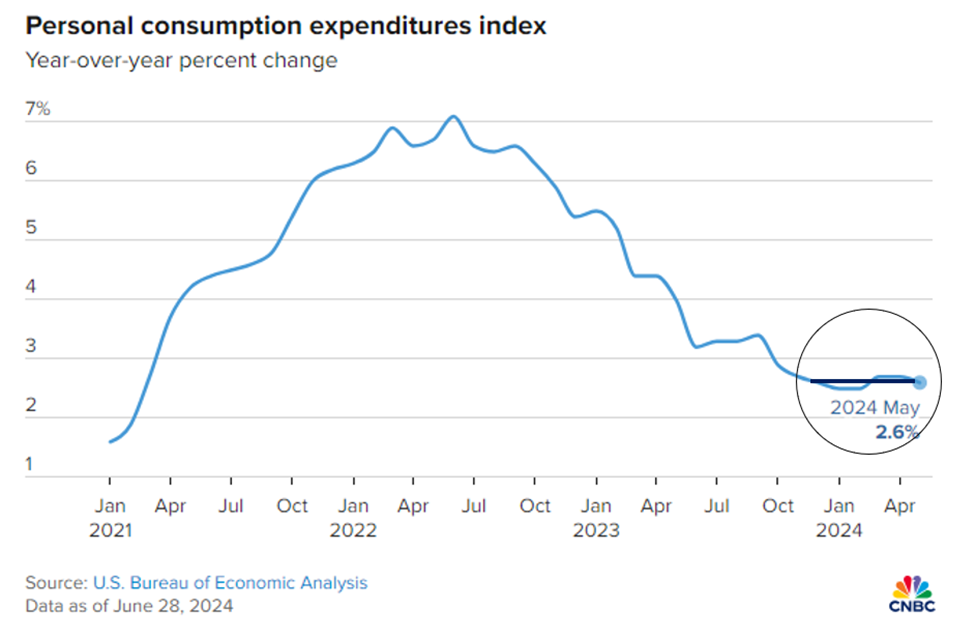

The core personal consumption expenditures price index increased just a seasonally adjusted 0.1% for the month and was up 2.6% from a year ago, the latter number down 0.2 percentage point from the April level, according to a Commerce Department report…

Including food and energy, headline inflation was flat on the month and also up 2.6% on an annual basis. Those readings also were in line with expectations.

It’s good news that this data didn’t come in unexpectedly hot. However, while many commentaries suggest that this will help the Fed build the case for a September rate cut, keep in mind that this 2.6% figure is the same as last December, as you can see below.

I’ve added a black line connected December 2023 to this morning’s reading.

The various Federal Reserve members have repeatedly said that they want to see data pointing toward a clear trajectory down to 2%. The related talking point they’ve echoed is “several months of data” suggesting this 2% trajectory.

Although this morning’s data is dovish, we’ve flatlined since last December. So, “several months of data” to warrant a rate cut in September sounds less certain to me unless the next two months of data are wildly dovish.

Beyond inflation, we also learned that personal income rose 0.5% on the month. That topped the 0.4% estimate. However, consumer spending came at just 0.2%, below the 0.3% forecast.

As I write, the markets are down slightly after having been up solidly earlier in the session. It appears Wall Street is relieved there were no curveballs in the data. However, this report wasn’t bullish enough to ignite a significant rally, or move the needle on the timing of rate cut expectations.

To illustrate, yesterday, the CME Group’s FedWatch Tool put the odds of a September quarter-point at 59.5%. As I write Friday early-afternoon, those odds have remained steady at 59.5%.

Now, in the wake of this morning’s data, let’s look at two “haves” versus “have nots” dynamics that are at work right now and what they mean for your portfolio.

The first centers on the U.S. consumer; the second features the stock market.

A rate cut is becoming increasingly needed for “have nots” Americans who are slipping financially

Beyond this morning’s lower-than-expected consumer spending figure, we saw another sign of a weakening consumer yesterday when Walgreens (WBA) reported earnings.

Shares of the drugstore chain plunged after the company reported disappointing profits while slashing its full-year outlook.

But it was commentary from Walgreen’s CEO on the condition of the American shopper that I found most interesting.

From CNBC:

“We assumed ... in the second half that the consumer would get somewhat stronger” but “that is not the case,” Walgreens CEO Tim Wentworth told CNBC.

He added that “the consumer is absolutely stunned by the absolute prices of things, and the fact that some of them may not be inflating doesn’t actually change their resistance to the current pricing. So, we’ve had to get really keen, particularly in discretionary things.”

ADVERTISEMENT

PayPal was not a popular idea at first.

In the late 1990s, when most people were still mailing checks, Elon Musk’s idea of making payments over the internet was unimaginable.

Now, though, PayPal is a promising contender in the ever-competitive AI boom.

It seems that everything Musk has done throughout his career sounded insane at first…

Which is why it’s important that you pay attention to his latest, strange invention.

It’s an AI device that could be the most powerful technology ever created.

This new idea is set to shock the world once again – and this time, you don’t want to be a nonbeliever.

Click here to learn all the details.

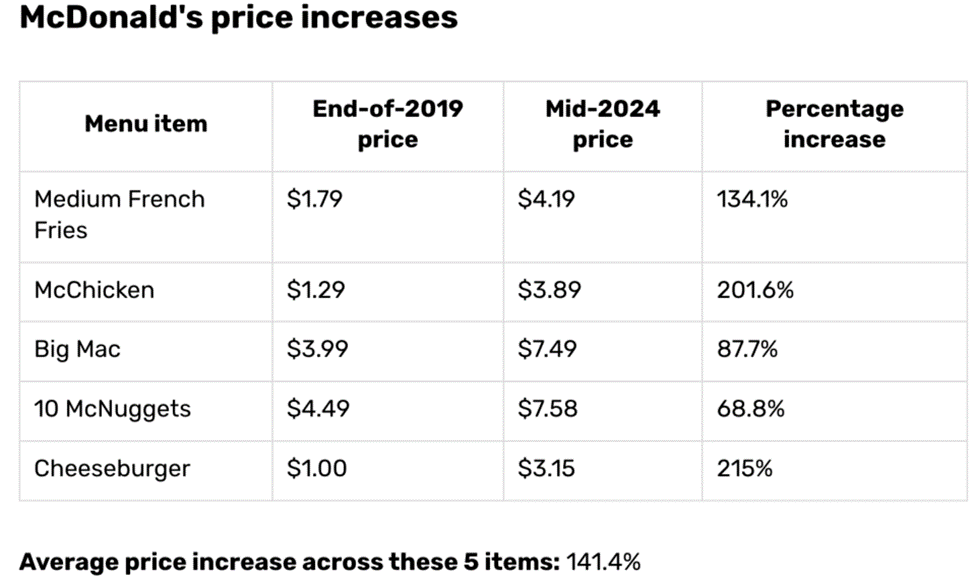

This is a good reminder that there’s a world of difference between inflation rates and absolute prices

Inflation measures changes in prices. So, all that slowing inflation means is that prices are continuing to get more expensive – but at a slower rate.

Shifting focus away from “falling inflation” toward “current prices” reveals why so many Americans are struggling to make ends meet each month.

Our Editor-in-Chief and fellow Digest writer, Luis Hernandez, provided a great example of this on an internal Slack channel earlier this week.

Though the image below shows the percent change in prices at McDonald’s, I’d point you toward the mid-2024 prices themselves.

Source: The Street

$7.49 for a Big Mac?

Luis summed it up succinctly: “Why no one feels good about slowing inflation...”

Meanwhile, data show that an increasing number of Americans are turning to credit cards to meet their monthly spending needs, and it's leading to an uptick in defaults and delinquencies.

Here’s American Banker:

…New data from the Federal Reserve Bank of New York indicates that defaults haven't peaked yet, as the number of borrowers maxing out their cards approaches its pre-pandemic level…

The percentage of credit card balances that slid into delinquency rose to nearly 9% last quarter, a rate not seen in more than a decade.

Joelle Scally, a household and public policy research leader at the New York Fed, said in a prepared statement that the rise in borrowers missing credit card payments signals "worsening financial distress among some households."

The challenge for the Fed is that while these households are hurting, “haves” households are doing great because of high interest rates

For those with a healthy nest egg, a savings account throwing off 5% interest means some great disposable income that’s finding its way into the economy, keeping inflation more elevated than otherwise.

This creates a Catch-22 for the Fed…

Does it choose to help lower-income Americans by cutting rates, knowing that those lower rates might goose inflation?

Or does it hold rates higher for longer to snuff out inflation, knowing those higher rates might kneecap lower-income Americans?

Here’s how Politico puts it:

“Lower-income households felt the pain from the disease, which was higher inflation. And now they feel the pain from the cure, which is higher borrowing costs,” Bovino said.

Wealthier households, in contrast, are doing well, boosted by a buoyant stock market and higher yields on savings, and they continue to fuel the economy through spending.

This is the “K-shaped” economy we’ve highlighted in past Digests reflecting the growing divide between “haves” and “have nots.”

What is the Fed willing to sacrifice?

ADVERTISEMENT

NVIDIA is the biggest company in the world, and if you had gotten in at the beginning of the AI boom, you'd be up 701%. Not bad, BUT...

You could have done better with help from millionaire trader Jonathan Rose.

He recommended a rainmaker trade on another hot stock — Super Micro Computer — back in September 2022... a full three months before the AI craze kicked off.

And it hit big, up as much as 1,060% in under two months.

That's bigger than NVIDIA's record gains and 10X faster too.

But that's just the tip of the iceberg. Because Jonathan's got a new rainmaker trade locked and loaded, ready for you.

Catch it here now — while you still can.

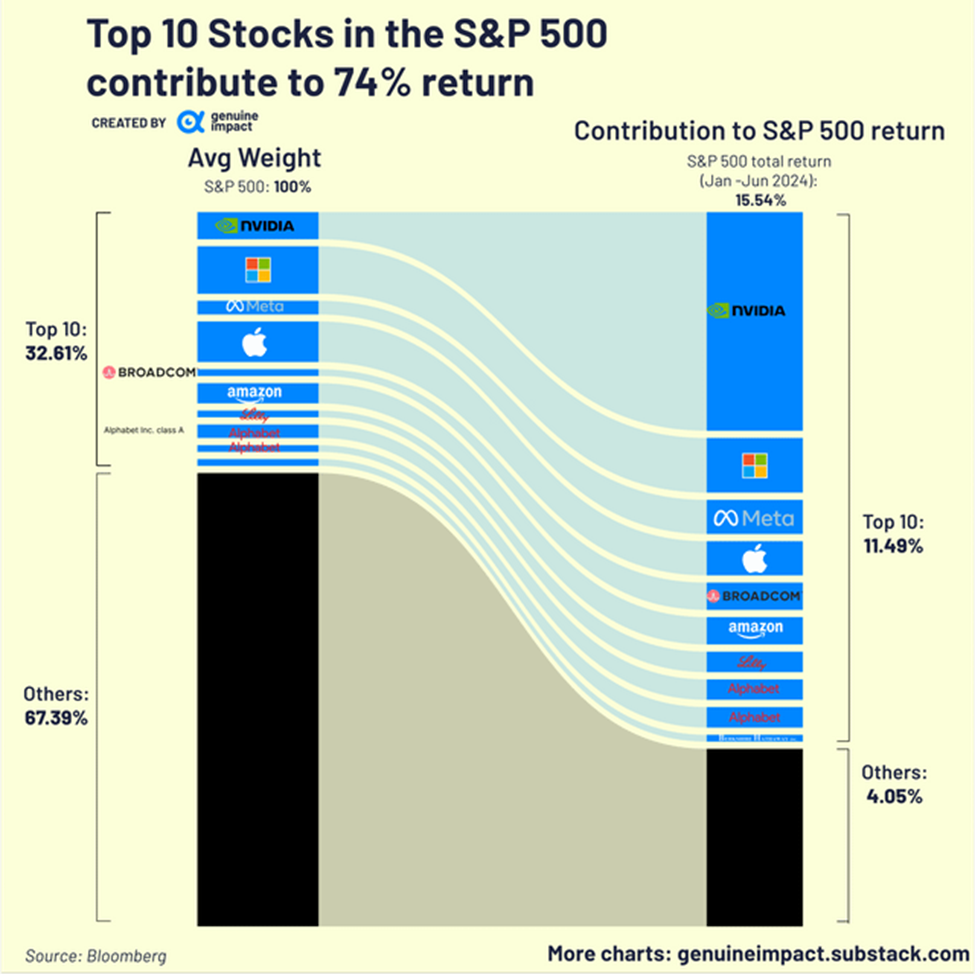

Meanwhile, let’s look at a parallel “haves” versus “have nots” dynamic playing out in today’s stock market

In recent Digests, we’ve pointed out how narrow this bull market has grown.

A handful of tech/AI leaders have been responsible for the majority of gains this year while the average stock is up, but not by much.

To illustrate, as you can see below, the top 10 biggest stocks are contributing 11.49% to the S&P’s total return this year while the rest of the market is contributing just 4.05%.

This means mega-cap stocks are responsible for 74% of the S&P’s return this year.

This market version of “haves” and “have nots” has some interesting historical relevance.

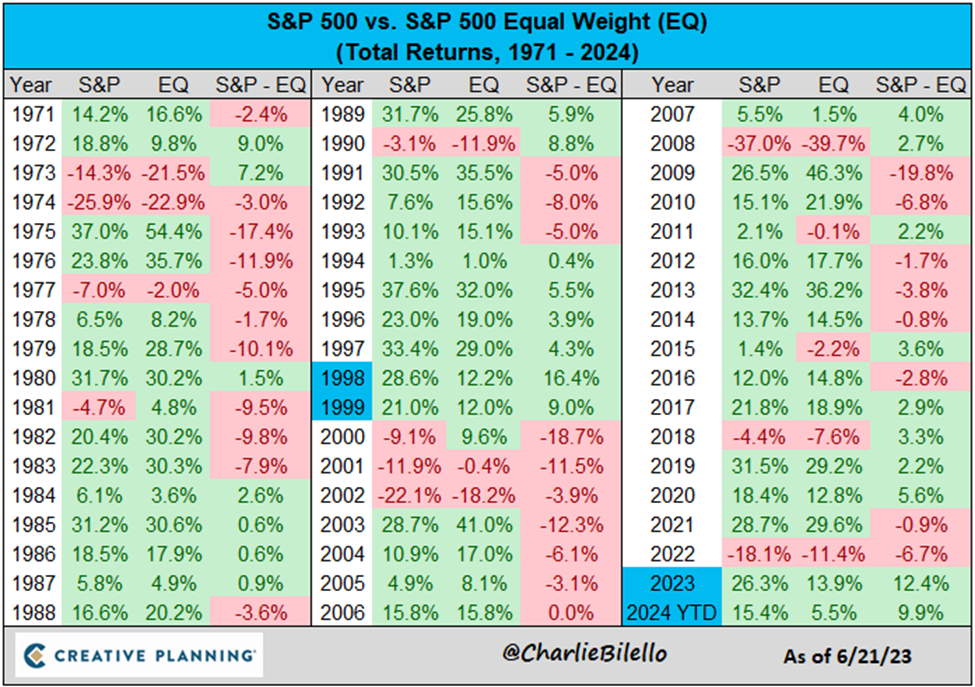

The market-cap weighted S&P Index, which is heavily influenced by the mega-cap tech stocks above (Nvidia, Microsoft, Amazon, etc.) is crushing the S&P Equal Weight Index in 2024. As the name suggests, the Equal Weight Index gives each holding the same weighting when calculating returns.

Here’s Charlie Bilello from Creative Planning with the significance:

The market cap-weighted S&P 500 is outperforming the equal weight index by nearly 10% this year, following 12% outperformance in 2023.

Since 1971, the only back-to-back years with a higher combined outperformance: 1998-1999.

Meanwhile, on Wednesday, the research shop Bespoke reported that the S&P 500 climbed on negative breadth.

Here they are with more and the significance:

It's now been five days in a row where price has gone in one direction and breadth has gone in the other. That ties the record streak from April 1999.

In the same way that the average U.S. consumer could use some rate cuts from the Fed, so too could the average stock.

In the absence of knowing when those cuts will come, there’s one market approach that feels most appropriate for today…

Trading.

In yesterday’s Digest, we put trading front-and-center.

We highlighted legendary investor Louis Navellier who’s currently in an AI “mania” trade.

Then there was Jonathan Rose, who’s gearing up for earnings season which he trades by finding mispriced options.

Finally, there’s the latest addition to our corporate family, Tom Gentile, who is a veteran pattern trader, identifying reliable stock price patterns in historical data, then placing calculated wagers that those patterns will repeat.

I encourage you to learn more about the styles from all three of these veteran traders. After all, you probably noticed the parallels in the data above between today’s market conditions and those in 1999…

To me, that suggests “trading this market” is a wise mindset. The three trading pros above have almost 10 decades of experience between them helping everyday investors succeed in doing exactly that.

ADVERTISEMENT

You have just days left to prepare for a sudden shift in the stock market that could double your money 6 different times. The man whose work pointed to the best-performing stock every single year from 2012 through 2023 explains the full details here.

But to make this Digest as valuable to you as possible, let’s give you a rubber-meets-road trade set-up to put on your radar

If you want to place the trade today, I believe it will pay off handsomely in the years to come. But to be clear, we could still be early, and prices could go lower.

I’m talking about small caps.

We profiled the opportunity setting up in small caps earlier this month. In short, the divergence of returns between large-cap stocks and small-caps stocks is hitting historical levels – and suggesting a massive mean-reversion rally is on the way for small caps.

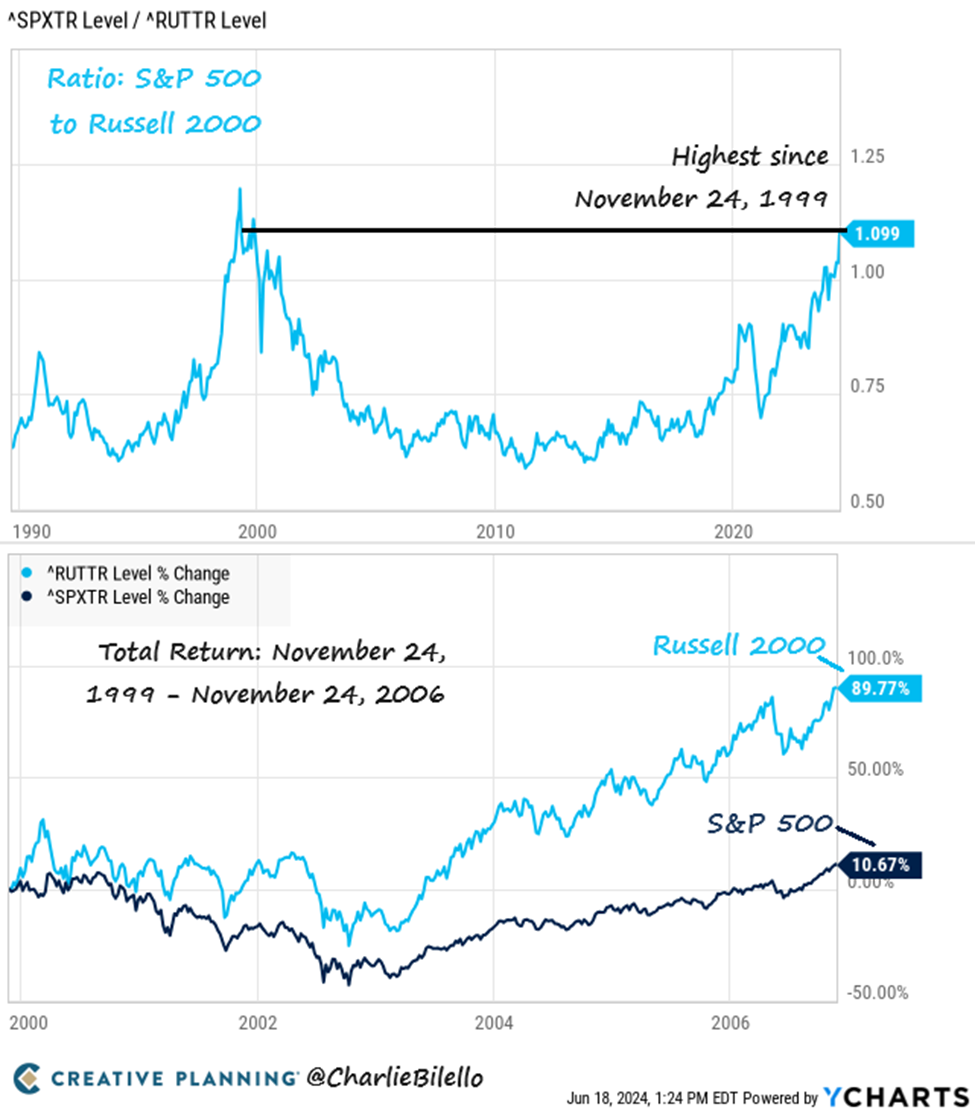

Let’s go back to Charlie Bilello:

The biggest US companies have been dominating the equity market for well over a decade. As a result, the outperformance of US large caps (S&P 500) over small caps (Russell 2000) is now at its most extreme level since November 24, 1999.

What happened in the 7 years following the 1999 extreme?

Reversion to the mean.

Small caps would outperform large caps by a wide margin, with the Russell 2000 gaining 90% versus an 11% gain for the S&P 500.

Again, small caps could keep sucking wind – especially if the Fed maintains higher for longer rates. But at some point, a reversion is coming, and it’s going to make one heck of a trade.

Tying it all together, we have a growing divergence between “haves” and “have nots” with both U.S. consumers and the stock market

In the middle of these respective tensions is the Federal Reserve and its interest rate policy.

Will today’s PCE data finally give the Fed the green light to cut as many talking heads are now suggesting?

We hope so, but we’re not convinced. And so, without knowing for sure, nimble trading is our gameplan.

Have a good evening,

Jeff Remsburg

Tidak ada komentar:

Posting Komentar