|

Reimbursement is supported by a permanent J-code (J9161), effective as of April 1, 2025. LYMPHIR is included in the NCCN Guidelines with a Category 2A recommendation. Patient and provider support programs are already active. Commercial-ready inventory with a 60-month shelf life is already in place to meet projected demand for 12–18 months post-launch.

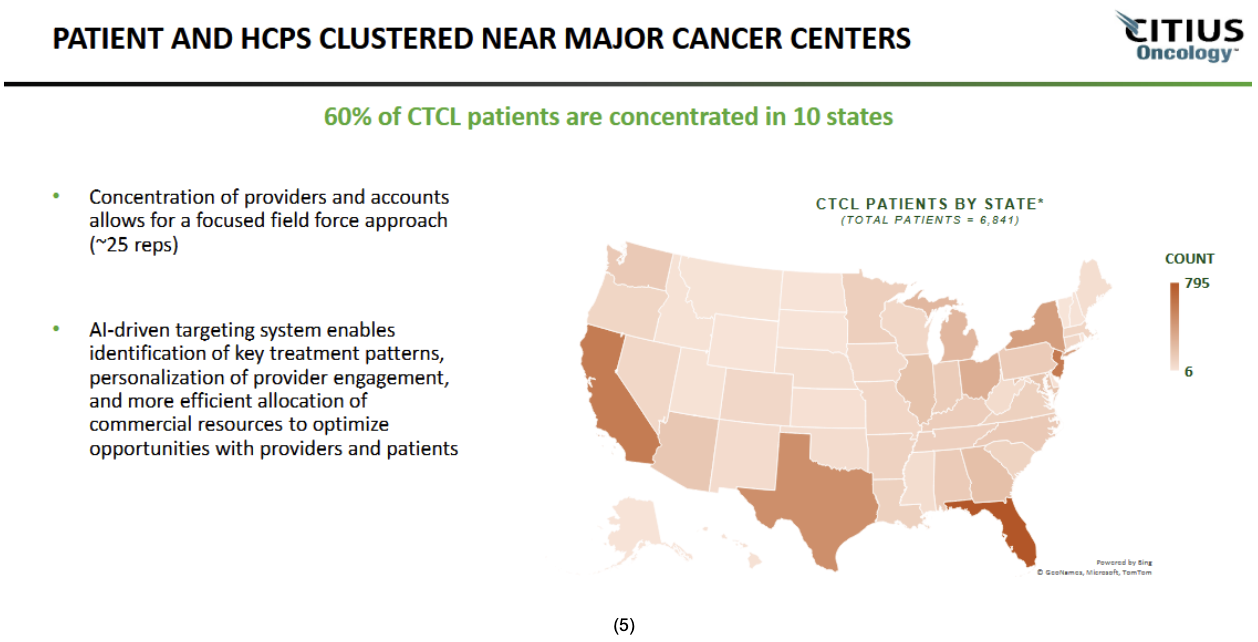

The opportunity itself isn't theoretical.

CTOR estimates the U.S. addressable market at over $400 million, based on internal research. But here's what amplifies that: 60% of all CTCL patients are concentrated in just 10 states. Only 10% of providers treat three or more patients. That means only 427 high-value prescriber accounts matter. A focused, specialized field force of approximately 25 representatives can reach the concentrated nodes where decisions get made. This isn't spray-and-pray distribution. This is surgical precision. 🎯

Act Two: Global Acceleration (December 4 – Just 3 Days Later) 🌍 (1)(2)(5)(6)(7)

On December 4, CTOR announced an exclusive distribution agreement with Er-Kim for LYMPHIR across Turkey and key Gulf Cooperation Council countries: Bahrain, Qatar, Oman, Kuwait, Saudi Arabia, and the United Arab Emirates.

That single announcement brought international availability to 19 markets outside the U.S.—expanding from a prior October announcement covering Greece, Cyprus, Malta, Bulgaria, Romania, Croatia, Serbia, Albania, Bosnia Herzegovina, Kosovo, Montenegro, and North Macedonia.

Nineteen markets in sixty days.

This isn't gradual market entry. This is aggressive, coordinated expansion signaling internal confidence in demand.

CEO Leonard Mazur stated: "This agreement represents a significant milestone in our global expansion strategy. Er-Kim has deep industry experience and a strong track record of providing access to oncology therapies in complex international markets."

Translation: This isn't a licensing footnote. These are experienced distribution partners with oncology pedigree.

Act Three: Capital Positioned (December 10 – 9 Days After Launch) 🏦

On December 10, CTOR closed an $18 million concurrent registered direct offering priced at-the-market. The capital raise itself is noteworthy for what it signals: the company wasn't scrambling. It closed financing nine days after launch, at $1.09 per share, with a single healthcare-focused backer. This suggests pre-arranged, orderly capital deployment—not desperation capital-raising.

Here's the three-act structure: announcement → international expansion → capital. That's coordinated execution, not improvisation.

The Competitive Moat: Long-Term Runway 🛡️ (1)(2)(5)(6)(7) What's equally important: the intellectual property protection. LYMPHIR has: -

12 years of BLA exclusivity (from FDA approval) -

7 years of orphan dr-ug exclusivity -

2 patents pending for use as combination therapy with checkpoint inhibitors -

Complex proprietary manufacturing process protected as trade secret That means roughly 19 years of protected runway before generic competition becomes realistic. This isn't a product with a five-year window. This is a protected franchise. ✨

Growth Upside: Expansion Beyond CTCL (Coming Q1 2026) 📊 (1)(2)(5)(6)(7)

What's flying under the radar: LYMPHIR isn't just capturing CTCL patients. Two investigator-initiated trials from academic medical centers are testing the medication's potential in broader indications—with Phase 1 data coming in Q1 2026.

University of Pittsburgh (with Merck's KEYTRUDA): -

Testing LYMPHIR in combination with a checkpoint inhibitor in solid tumors -

27% objective response rate and 33% clinical benefit rate -

57-week median progression-free survival for patients achieving clinical benefit -

This signals potential to oncology markets well beyond the orphan space University of Minnesota (with CAR-T therapies): LYMPHIR-P Program: This isn't speculative science. These trials are active. Data is coming in 90 days. The market isn't pricing in the expansion potential—but physicians testing the medication outside the approved indication already are. 🔬

This Is the Phase Where Stories Often Change Tone 🔄 (1)(2)(5)(6)(7)

The science risk is behind it. The product exists in the real world. Distribution is live across all major U.S. wholesalers and now 19 international markets. Reimbursement is defined with J-code active. Capital is in place. Competitive protection extends 19 years. Management is executing in coordinated waves, not reactive chaos.

What's left is execution—and the market's ability to recognize that this is no longer a "what if" situation. Physicians are already treating patients. Wholesalers are already shipping product. Payers are already authorizing reimbursement. The field force is already engaging providers in the concentrated prescriber base.

CTOR didn't introduce a promise this month. It introduced a commercial product backed by distribution, reimbursement, clinical data, patient support infrastructure, international partnerships, capital, and long-term intellectual property protection.

And in biopharma, that's the point where attention tends to shift from speculation to positioning — sometimes faster than people expect.

The hard part isn't coming.

It's already done. ✅ |

Tidak ada komentar:

Posting Komentar