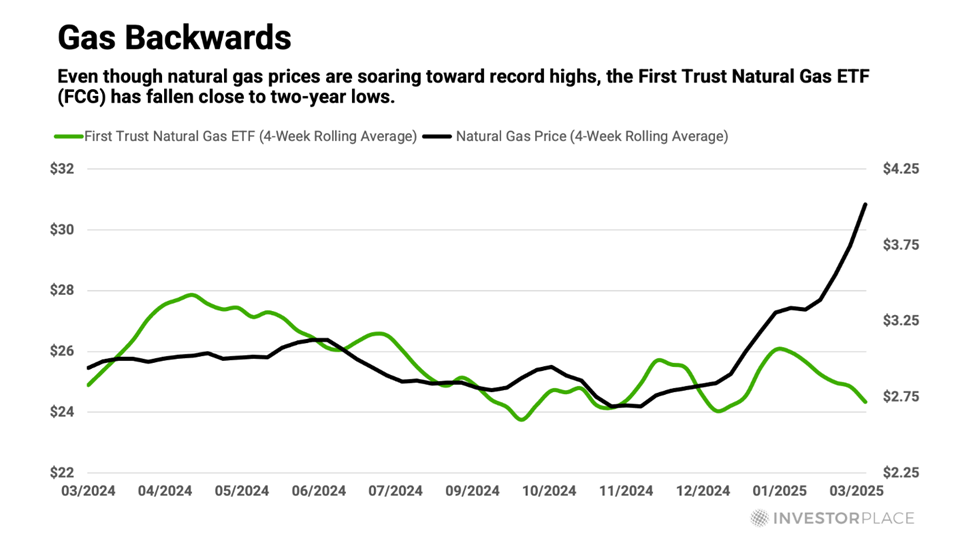

| WEEKLY ROUNDUP Hello, Reader. Life can be filled with anomalies. A white puppy is born into a litter of brown siblings. Snowfall blankets the Florida Panhandle. That one Monday when Garfield was happy. Anomalies happen in the stock market, too. As it happens, a short-term anomaly has developed in the natural gas market: Gas prices are rising, but natural gas stocks are falling. The chart below tells the tale.

Tumbling crude oil prices probably deserve most of the blame for causing this rare divergence. For starters, falling crude prices cast a pall over the entire fossil fuel sector. In addition, most major natural gas producers also produce significant volumes of crude oil. As a result, the shares of almost every North American natural gas producer have been sliding lower, no matter how little crude each company produces. The First Trust Natural Gas ETF (FCG) is a perfect case-in-point. Its price has gone nowhere during the last two months, even though the natural gas price has jumped around 35% over that brief time frame. Sooner or later, natural gas stocks should begin to reflect the strong pricing in the natural gas market and the bullish trends underway there. U.S. natural gas in storage, relative to seasonal three-year average levels, has been dropping sharply for nearly a year. The most recent reading showed storage levels 14% below average levels for this time of year. Against this backdrop, U.S. natural gas demand is on track to surpass supply by a wide margin over the next two years, which should reduce stockpiles even further below three-year average levels. Our nation’s rapidly growing LNG (liquified natural gas) export capacity will account for most of the demand growth. The U.S. became the world’s biggest LNG supplier in 2023, surpassing Australia and Qatar. In February, the amount of gas flowing to the eight big U.S. LNG export plants rose to a record-high 15.6 Bcf/d (billion cubic feet per day), as new units at Venture Global’s 3.2-Bcf/d Plaquemines LNG export plant in Louisiana entered service. So far this month, LNG export volumes are even higher. Looking down the road, the U.S. Energy Information Administration (EIA) predicts LNG exports will grow by 2.1 Bcf/d and an additional 2.1 Bcf/d in 2026, due to new export facilities that will begin operating during that time frame. Assuming this LNG demand materializes as the EIA expects, it would account for a whopping 72% of the entire country’s expected demand growth in 2025 and 2026. Unlike domestic demand spikes that occur during exceptionally cold winters or hot summers, LNG export demand is relatively constant. Once in place, it remains in place and continues to consume domestic gas supplies, no matter what national weather conditions might be. As such, this source of demand puts continuous upward pressure on natural gas prices, especially if domestic gas production fails to keep pace. The EIA is predicting that exact scenario. Although the agency expects domestic production to increase by 3.6% during the next two years, that figure is well below the 5.8% demand growth the agency predicts. This widening supply-demand imbalance would reduce U.S. gas inventories, which would be unequivocally bullish for natural gas prices. My newest Fry’s Investment Report play on natural gas is already reaping rewards from improving natural gas prices in the Permian Basin of West Texas… although the company’s still-depressed share price does not reflect that potential. At less than eight times earnings, its share price seems substantially undervalued, relative to both its peer group and to its “hidden” earnings potential from its holdings in the Delaware Basin chunk of the Permian. But all that means is that this company currently offers a great buying opportunity. Bottom line: U.S. natural gas is “Buy,” which means this natural gas play is a “Strong Buy.” For more, click here to learn more about becoming a Fry’s Investment Report member today. Now, let’s look at what we covered here at Smart Money this past week… |

Tidak ada komentar:

Posting Komentar