Dear Reader, Dr. Mark Skousen here. You want to know what makes me furious? Watching the same scam play out over and over. A company like SpaceX could go public any day now… in what Bloomberg is touting as "the biggest IPO of ALL TIME." And who is allowed to get in early? The hedge fund guys. The Goldman partners. The private equity sharks. The same people who've already won the game ten times over. They gobble up shares at pre-IPO prices… where around 95% of the gains are made. Then they open the gates to everyone else — after they've already locked in their fortunes. Regular investors get the leftovers. The scraps. I've been fortunate… Early in my career, I made the right connections. CIA directors. I’ve met four US presidents. Wall Street power players. The types of people who can get you in Pre-IPO. I've had a seat at the table my whole life. And it's made me wealthy. But I'm 77 years old now. I'm tired of watching good people get shut out of opportunities that could change their lives. So when I heard SpaceX could be getting ready for a $1.5 TRILLION IPO... I decided to pay it forward. Today, I’m prepared to share an "access code" that lets my readers grab a pre-IPO stake in SpaceX. Before Elon’s big announcement. Before the feeding frenzy. Before regular investors get shut out again. For once, the door is open. And I'm holding it for you. Click here to see how to get your pre-IPO ‘access code’. Yours for peace, prosperity, and liberty, AEIOU, Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club P.S. After meeting Elon face-to-face and conducting my own due diligence… Im now convinced he’ll announce the IPO on March 26, 2026. Don’t miss your shot at life-changing returns. Click here before this window closes forever.

Just For You 3 Under-the-Radar Earnings Surprises Could Signal a New TrendSubmitted by Dan Schmidt. First Published: 2/17/2026.

Key Points- Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

- Special Report: Introducing "Elon Musk's Day-One Retirement Plan" (From Brownstone Research)

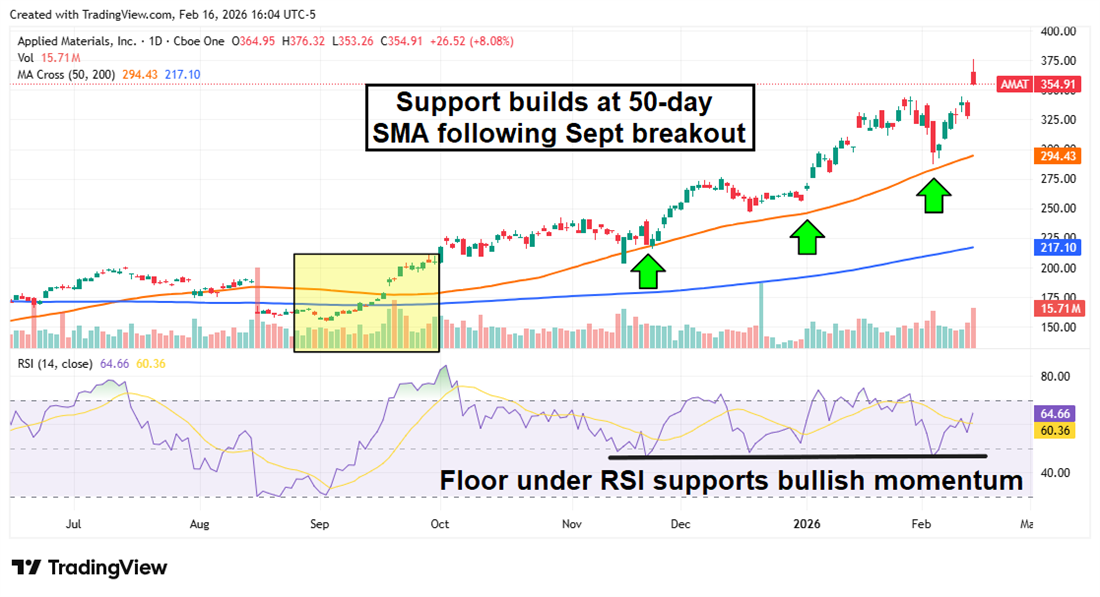

Earnings season is winding down, and more than three-quarters of the companies in the S&P 500 have reported their latest results. According to FactSet, roughly 74% of firms reporting so far have beaten analysts' EPS estimates, and 73% have beaten revenue estimates. These figures are within the five- and ten-year averages, but the dispersion between winners and losers left aggregate earnings growth essentially flat for the period. Many of last year's winners have underperformed in 2026, while some former laggards have posted sharp gains. Three companies whose earnings reports don't usually make headlines deserve a closer look — are these one-off standouts or signs of a broader trend? Applied Materials: Semiconductor Demand and Guidance Power Double-Digit GainsApplied Materials Inc. (NASDAQ: AMAT) is probably the most "on-the-radar" name here, given its roughly $280 billion market cap and about $28 billion in annual sales. As a picks-and-shovels play in the semiconductor space, Applied Materials often reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) grab headlines. That said, its most recent report merits attention: AMAT shares jumped 12% after the release, driven by strong guidance and robust equipment demand. The company reported its fiscal Q1 2026 results on Feb. 12, beating analysts' estimates on both EPS and revenue (earnings topped expectations by about 7%). What really energized investors was CEO Gary Dickerson's projection of roughly 20% sales growth for calendar 2026 — a target that outpaced even the most optimistic analyst forecasts. Most of Applied's revenue comes from its Semiconductor Systems division, which provides equipment for flash memory, logic, DRAM and other chip manufacturing. Dickerson guided Q2 revenue near $7.65 billion and expects continued rapid growth in the Applied Global Services business. Analysts moved quickly to raise targets and ratings after the upbeat report. The stock received upgrades from Hold to Buy at Summit Insights and KGI Securities, and the average price target among the 17 analysts who raised estimates is now $435 — roughly 20% above current levels.

AMAT shares have been trending higher since September, after the price moved above both the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has acted as reliable support on pullbacks. The Relative Strength Index (RSI) remains below the overbought threshold of 70 despite the post-earnings surge, suggesting the rally may have staying power. Advance Auto Parts: Turnaround Efforts Start to ShowAdvance Auto Parts Inc. (NYSE: AAP) may finally be returning to investability after losing more than 50% of its value over the past five years. The last 12 months were especially tumultuous for the company — and for the automotive sector generally — as AAP posted a steep loss in Q4 2024 and then faced tariff-related headwinds during the administration transition. CEO Shane O'Kelly has pushed a back-to-basics strategy focused on cost cutting, and those efforts now appear to be paying off. Advance Auto Parts' Q4 2025 results surprised to the upside. Revenue modestly beat expectations ($1.97 billion vs. $1.95 billion expected), and EPS of $0.86 more than doubled consensus. Same-store sales grew about 1% for the year, and management closed 17 underperforming locations. The 2026 guidance pushed the stock higher: management forecasts 1–2% comparable-store sales, roughly 45% gross margin, EPS of $2.40–$3.10 and approximately $100 million in free cash flow.

Some profit-taking followed the release, since the stock had already rallied nearly 50% year-to-date. Still, the breakout above both the 50-day and 200-day SMAs supports the bullish case. The Moving Average Convergence Divergence (MACD) also turned positive, with the MACD line crossing above the signal line and rising above the histogram during the move. Rivian: Narrowing Losses and 2026 CatalystsFriday the 13th was anything but unlucky for Rivian Automotive Inc. (NASDAQ: RIVN), which beat both top- and bottom-line estimates in its Q4 2025 report. Year-over-year revenue fell about 25% as EV tax credits expired, but sales still exceeded expectations and the company narrowed its loss to $0.66 per share. Loss reduction reflected a $5,500 increase in average vehicle selling price and an average $9,500 decline in the cost of vehicles sold. Rivian delivered its first year of gross profit, and the more affordable midsize R2 model is slated to begin deliveries in Q2 2026. Management expects to sell between 62,000 and 67,000 vehicles in 2026; the low end of that range would be a roughly 47% increase over 2025 volumes.

RIVN shares jumped about 20% in a volatile session after the report, though gains were trimmed from the open. The stock currently sits near the 50-day SMA, which previously acted as support during rallies at the end of 2025. A bullish MACD crossover signals improving technical momentum, but a successful R2 rollout will likely be necessary for the company to sustain this progress.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here |

Tidak ada komentar:

Posting Komentar