Pepsi stock might be one of the best value opportunities in the market today, one which investors can time by following this ratio.. ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Gabriel Osorio-Mazilli

Investors must always understand where they are in the stock market cycle. This is easier said than done, as all the noise can often blind participants to what they should be looking into and thinking about as well. However, occasionally, a certain indicator flashes to give investors an idea of where capital might be flowing. Breaking things down into simplicity, there are only two major areas that capital often prefers. On one end is the world of value stocks, not known for their exciting growth or volatility but rather for their stability and long-term promise of an adequate return. On the other hand, investors can consider growth stocks, which are a bit more speculative in nature, to say the least, and therefore more tied and correlated with the overall business and economic cycle. Therein lies the indicator investors can track: a performance or ratio between value and growth stocks, which will be broken down in a minute. What really matters is that today’s level points to a potential rotation back into value, which always lines up with a volatile S&P 500 such as today’s. That is precisely why considering shares of PepsiCo Inc. (NASDAQ: PEP) could be a winning strategy in the coming months and quarters. What’s Driving Rotations Right Now To track this safety versus speculation gauge, investors should add broader coverage of value and growth to their watchlists. This is where the iShares S&P 500 Value ETF (NYSEARCA: IVE) and the iShares S&P 500 Growth ETF (NYSEARCA: IVW) can come into play, representing value and growth, respectively. Far from just looking at a single chart or price action, investors need to start thinking like professional traders, who see most of the financial world in ratios and relative performance, so to speak. When charted as a ratio, it becomes obvious that value stocks, relative to growth, have now hit a very important cyclical low point, prime for a reversal. Of course, rotations don’t happen on their own—they require a catalyst. Today’s news cycle is largely driven by the impact of President Trump’s recently imposed trade tariffs, which are complicating earnings and economic forecasts for investors and economists alike. This uncertainty translates into volatility, which is no friend of growth stocks. So, investors have a paved road ahead to justify a rotation back into value stocks from this current cyclical low. Not all value stocks are standing on equal ground today; some offer better opportunities than others. Why Is Pepsi Stock a Top Choice? Some value stocks offer a decent risk-to-reward setup for investors today, but nothing big enough to trigger the type of rotation and investments being considered today. This is why Pepsi stock, which only trades at 71% of its 52-week high, becomes a top target for buyers hungry for safety and upside. More than just its price action relative to 52-week highs, investors can note the company’s forward price-to-earnings (P/E) ratio of just over 16.0x, which is also lower than even the peak months of the COVID-19 pandemic, when the entire United States economy was essentially closed. Today’s world, tariffs or not, is nothing close to being as dire or uncertain as when the pandemic was around, giving Pepsi stock no justifiable reason to be trading this low. That’s the biggest opportunity of all, and it is already being taken advantage of by bold buyers out there. Capital Is Warming Up To Pepsi Stock As of mid-May 2025, institutional buyers from UBS Asset Management decided to boost their stakes in Pepsi stock by 1.8%. This may not sound like much on a percentage basis, but it was enough to get them to a stake worth up to $1.7 billion today, giving investors another pillar of strength to lean on. These buyers may see more than just a discount in PepsiCo, as its position in the consumer staples sector likely offers a reliable cushion against today’s market volatility. And the optimism doesn’t stop there. Wall Street analysts now have a consensus price target of up to $160.7 per share on Pepsi stock. This would call for a rally of as much as 23.2% compared to today's prices, which should excite investors during this uncertainty. But what about timing? Investors using a dollar-cost-averaging strategy can continue buying Pepsi at these deep discounts. Those with a more aggressive approach can watch the value versus growth ratio and wait for a breakout, which is one of the strongest signals that more capital may soon flow into Pepsi.  Read This Story Online Read This Story Online | People who don't understand the gold market are about to lose a lot of money. Unfortunately, most so-called "gold analysts" have it all wrong…

They tell you to invest in gold ETFs - because the popular mining ETFs will someday catch fire and close the price gap with spot gold. Go here to learn about my Top Four picks for the coming bull mania. |

| Written by Gabriel Osorio-Mazilli  Today’s market is highly reactive to headlines, and understandably so. With major developments emerging almost weekly, it’s no surprise investors stay glued to their newswires as the S&P 500 swings in all directions. However useful this may be, the awareness part, there is also a caveat to connecting unrelated themes to one another. This is the case for a major stock in the technology sector, which might be a massive opportunity. Today’s market is highly reactive to headlines, and understandably so. With major developments emerging almost weekly, it’s no surprise investors stay glued to their newswires as the S&P 500 swings in all directions. However useful this may be, the awareness part, there is also a caveat to connecting unrelated themes to one another. This is the case for a major stock in the technology sector, which might be a massive opportunity.

Shares of Alphabet Inc. (NASDAQ: GOOGL) have traded down to 83% of their 52-week high today. They are not in an outright panic or bear market but have significantly underperformed their peers in the rest of the space, especially within the Magnificent Seven stocks group. This could be the case for many reasons, though one specific reason is directly tied to the company's news cycle. Alphabet hasn’t been releasing much news related to artificial intelligence lately, nor equipment or services, but rather with regard to its autonomous taxi service called Waymo. Now, Waymo is absolutely making a splash in certain cities within the state of California, but the autonomous taxi name itself might be the sole reason why the markets have failed to react positively yet, giving investors a chance to exploit this fact. Autonomous Driving Isn’t as Exciting Right Now In any other news cycle, it might be. But today, the term autonomous driving or autonomous taxi has been tarnished by another completely unrelated company to Alphabet, Tesla Inc. (NASDAQ: TSLA). It seems that, apart from being a part of the technology sector and the Magnificent Seven, these two don’t have too much in common. Yet Tesla has recently overpromised and under-delivered on its robotaxi initiative, which sounds a lot like the autonomous taxi promise that Alphabet’s Waymo is making today. This might not seem like a legitimate reason to keep the stock down, but investors need to remember that today’s market is totally exposed to the news cycle. That being said, there are many key differences in Waymo’s current stance that set it apart from Tesla’s delayed robotaxi initiative. For starters, the technology itself is very different from Tesla’s in the sense that Waymo’s fleet is fully autonomous and requires no human supervision, unlike Tesla’s self-driving mode, which does require supervision. Secondly, Waymo vehicles use radar technology to allow them to fully operate in the environment around them successfully (again without supervision). While all of this might sound a bit too good to be true, the numbers speak for themselves regarding Waymo’s adoption rate. So far in 2025, Waymo reported up to 250,000 paid rides per week. These are not the types of numbers investors would see from a startup idea only breaking ground into the market; this is a well-developed and mature service that has already seen enough acceptance and adoption to justify further expansion and growth. How This Creates a Gap to Be Filled Of course, there are no real ways to understand how Waymo will affect Alphabet’s gigantic business, and the bears are not only leaning on its resemblance to Tesla robotaxis as a thesis but also on the fact that Google Search has lost ground to ChatGPT over the past couple of months. There’s one gap in this logic, however, since artificial intelligence models like ChatGPT ultimately source most of their answers and information from a database provided by Google, which is part of Alphabet’s umbrella. Therefore, it is reasonable to expect some sort of collaboration in this regard. Now, when investors come back to Waymo, the growth and acceptance could also make it a reasonable partnership candidate with a name like Uber Technologies Inc. (NYSE: UBER), as the synergies and benefits both can have by partnering are more than obvious at this point. In fact, it does seem that Uber and Alphabet have been in talks of seeking a combination of their services, where executives talk through the thought process of how these two disruptors can coexist in their respective markets, creating new opportunities for both. Despite being a laggard in its space, Alphabet’s future developments in Waymo and other partnerships justified enough future momentum for some institutions to come knocking on its door. As of May 2025, those from UBS Asset Management decided to build up a stake worth up to $6.8 billion, signaling some of these investment themes and views are gaining traction among so-called “smart money.” Read This Story Online | During last month's historic market swings, most investors panicked. But a small group of traders calmly watched their accounts grow.

They were using Professor Jeff Bierman's "Genesis Cog" system to spot stocks being hijacked by institutional algorithms—before the moves happened. See how they used this strategy to profit during extreme volatility. |

| Written by Leo Miller

After posting what was likely its worst earnings report ever in Q4 2024, Trade Desk (NASDAQ: TTD) roared back with a vengeance in Q1 2025. The communication services company’s final report for 2024 saw it miss internal expectations on revenue for the first time in 33 quarters. Overall, it was the first time Trade Desk missed these expectations for its entire life as a public company. Being an occurrence markets had never seen, Trade Desk’s shares plummeted 33% in one day after the report. However, the company did not turn this disappointment into a pattern in Q1. Shares popped nearly 19% after the company’s latest release on May 8. As of the May 22 close, Trade Desk has recovered 64% since the 52-week low the stock eventually hit in early April. So, what was so great about Trade Desk’s most recent quarter, and can the recovery in this stock continue? The stock is still trading at nearly half of its all-time high reached in November 2024, indicating that significant further upside could be in play. TTD: Business Breakdown and Q4 Struggles For those who may be unfamiliar, Trade Desk is an advertising technology (AdTech) company. Essentially, its software helps advertisers manage their marketing campaigns. It uses AI to match these advertisers with the optimal place to display their ads, helping these advertisers maximize the return on their ad spending. It does this by analyzing massive amounts of data to target potential customers who are most likely to buy a company’s product. Within the advertising ecosystem, Trade Desk largely focuses on connected TV (CTV), also known as streaming. However, the company's platform is omnichannel. This lets advertisers connect with potential customers through different media types. The company shows its presence in these areas by partnering with both Netflix (NASDAQ: NFLX) and Spotify Technology (NYSE: SPOT). The main problem for Trade Desk in Q4 came from the company’s rollout of its next-generation ad tech platform, Kokai. In Q4, the company focused on fixing Kokai's structural issues. This slowed down the platform's adoption during the quarter. This is what ultimately caused the company to miss its forecasts. However, the opposite was the case in Q1. Trade Desk’s Kokai Flips the Script In Q1, Trade Desk crushed estimates both on the top and bottom line. The company’s revenue growth came in at 25%, greatly exceeding the just 17% growth Wall Street forecasted. Adjusted earnings per share (EPS) also grew by 27%, while Wall Street was looking for it to drop by almost 4%. The increase of 82 basis points to 34% in Trade Desk’s adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin aided this. Wall Street predicted the figure would fall to less than 26%. The company’s full-year revenue and EBITDA guidance also came in solidly ahead of expectations. Much of this success was due to an accelerated adoption of Kokai in Q1. The company noted that about two-thirds of its customers had transitioned to Kokai, which was “ahead of schedule." As it said in Q4, Trade Desk expects all its customers to transition to Kokai by the end of 2025. Trade Desk also shared very important metrics on how Kokai is driving improved client results. Compared to its previous platform, Solimar, the cost of clients acquiring a new customer dropped by 20%. Additionally, the cost to reach a unique person with an ad dropped by over 42%. Kokai also used 30% more data points when evaluating how well an ad might perform. Overall, all of these metrics show how Kokai is helping maximize return on ad spending, making clients much more likely to use it. Customer satisfaction is ultimately demonstrated by the fact that the company’s retention rate remained above 95%, as it has for 11 straight years. TTD Can Benefit Big Long Term as CTV Spending Looks to Overtake Traditional Overall, the successful outcomes that Trade Desk is driving for marketers are very hard to deny. Additionally, the shift in ad spend away from traditional TV to CTV still has a long way to go. eMarketer finds that just $29 billion in ad spending went to CTV in 2024, versus nearly $60 billion for traditional TV. That is less than a 33% share for CTV. They expect this gap to continue narrowing. This is a big long-term tailwind that Trade Desk can benefit greatly from. Due to these factors, Trade Desk looks poised to continue down the road of long-term success. Read This Story Online | Most people don't know this…

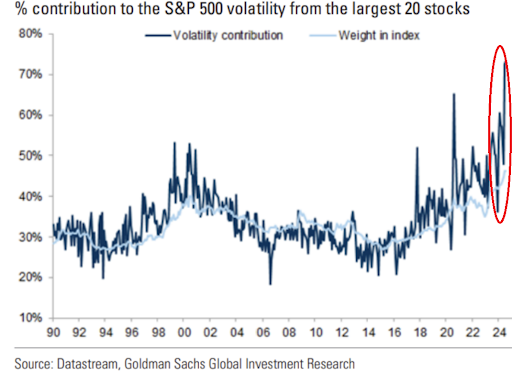

Out of the 500 stocks in the S&P 500…

Stocks like Nvidia, Tesla, and Apple - the MAG7 - are the ones really moving the markets.

Take a look at this chart of the 20 largest stocks causing 75% of the market volatility:

These stocks are causing more than twice the average volatility.

And that's great to know if you love trading the markets as much as I do.

It means you have fewer stocks to watch…

But you'd better watch them close when they make a big move. And I want to show you a trick I use to spot big market moves… |

|

| |

|

|

Tidak ada komentar:

Posting Komentar