October 3, 2024

ALERT: Double the Market Dividend with Oil's Other Catalysts

Dear Subscriber,

|

| By Jim Nelson |

Oil prices have been on the move this week as renewed violence and threats escalate in the Middle East.

But there are two other reasons — besides what’s going on in Israel, Lebanon and Iran — that could tip the scales for much higher prices before too long.

And there’s a clear way to play this move AND collect a solid stream of income.

First, demand is beginning to get the best of supply.

This is true both domestically and across the globe.

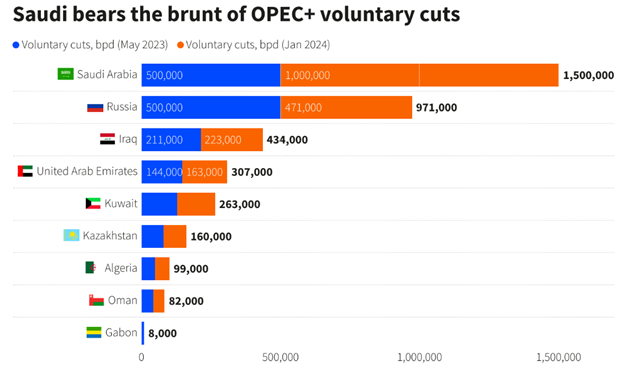

Take OPEC+ for instance, led by Saudi Arabia. The oil-producing cabal has kept strict production targets in place for over a year now.

These cuts are intended to keep prices high enough for the producing countries to profit.

Many, including those in the above Reuters article, believe that the Saudis could be persuaded to ease these cuts — as was already supposed to happen once this year.

But don’t tell the country’s oil minister.

Just yesterday, the Wall Street Journal reported:

“During a conference call last week, Prince Abdulaziz bin Salman, the oil minister of OPEC kingmaker Saudi Arabia, warned fellow producers prices could drop to $50 a barrel if they don’t comply with agreed production cuts, according to OPEC delegates who attended the call.

They said he singled out Iraq, which overproduced by 400,000 barrels a day in August, according to data provider S&P Global Ratings, and Kazakhstan, whose production is set to rise with the return of the 720,000-barrels-per-day Tengiz field.”

It sure sounds like the December deadline for removing the production cuts could be moved again. The Saudis are cracking down to ensure the cuts they already have.

Domestically, we’re seeing more production than ever before. But the increases could be over.

It takes a long time to gear up for additional production. And over the past two years, U.S. producers have done the opposite:

As you can see, U.S. oil rig count has fallen from its late 2022 peak … and stayed down. It’s well below 500 today.

That’s the supply side situation …

On the other side of the ledger, demand is increasing in many places.

Whether we are truly experiencing a “soft landing” after the spike in inflation from 2022 until now or not, last month’s interest rate cuts could fuel higher energy prices on their own.

Companies, specifically ones tied up in debt, will use the rate relief to expand. That’s what rate cuts are designed to do after all.

And that expansion means higher energy demand. There are other mandated expansions already ongoing, too.

Thanks to various bills passed over the past few years — like the $280 billion “CHIPS and Science Act” and the $1.2 trillion “Infrastructure Investment and Jobs Act” — a huge amount of money is pouring into the marketplace.

All of that construction adds to energy demand.

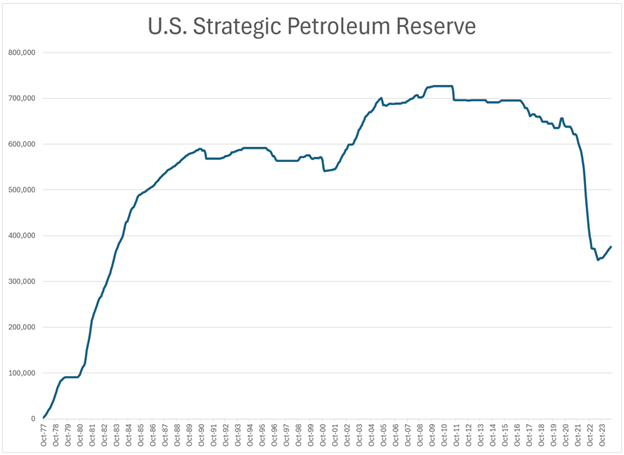

The other reason why this rally could have legs is that we have no backstop.

The U.S. Strategic Petroleum Reserve is nearly tapped out. It is still near its lowest level since 1983 thanks, in part, because of the supply cuts above.

A deficit and next-to-no reserves could spell trouble. The rest of 2024 could be yet another great time to be in energy stocks.

And I’d seriously consider this one to start with …

A Dividend Dominator

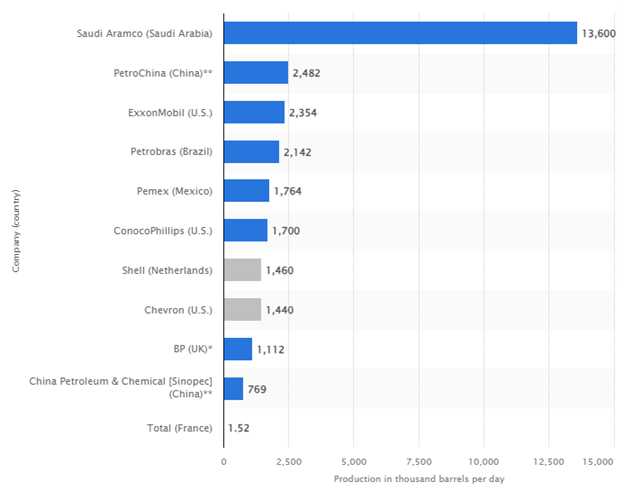

ConocoPhillips (COP) is one of the most recognizable oil companies in the world. With a market cap of $127 billion, its market position is well established.

In fact, by pure oil production, COP is the second-largest non-government player in the field:

This is the clearest indicator that any oil price hike will directly lead to profits for ConocoPhillips. But that’s not the only reason this company is the ideal way to play this trend.

It remains undervalued. At $109, shares trade at just 12.2x earnings.

It is also a cash machine. During its most recent quarter, COP saw $4.2 billion in free cash flow. That was 8.6% higher than the same period last year.

That cash is what’s behind its long, long history of paying large, growing dividends.

It’s been paying its shareholders quarterly for more than 20 years without fail — through both the Great Recession and the pandemic.

COP currently yields around 3%, which is more than double the average S&P 500 company. But even that’s going up …

The company is in the process of buying Marathon Oil (MRO) in an all-stock transaction. As part of this deal, COP is increasing its dividend by 34% during this quarter.

Add in its deep undervaluation, as well as the likelihood of higher energy prices and you have a great chance at profits with this oil giant.

Of course, there’s another way. Last year, we showed select members how to turn that 3% into a 10.6% annualized yield.

Next week, at our Great Income Solution Summit, you’ll see exactly how. Grab your spot by clicking here.

All the best,

Jim Nelson

Tidak ada komentar:

Posting Komentar