Dear Fellow Investor, | A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history...

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn't just a national asset.

It's an American birthright.

That means every citizen now has the legal right to stake a claim...

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall...

I've assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here - while the claim window remains open.

"The Buck Stops Here,"

Dylan Jovine, CEO & Founder

Behind the Markets

P.S. This claim belongs to American citizens - but the first profits will go to those who move early. See the full briefing here. | | | | | | |  | Fresh Insight for You |

|

|

|

The Memory Stock That Gained 1,500% in 1 Year |

|

|

|

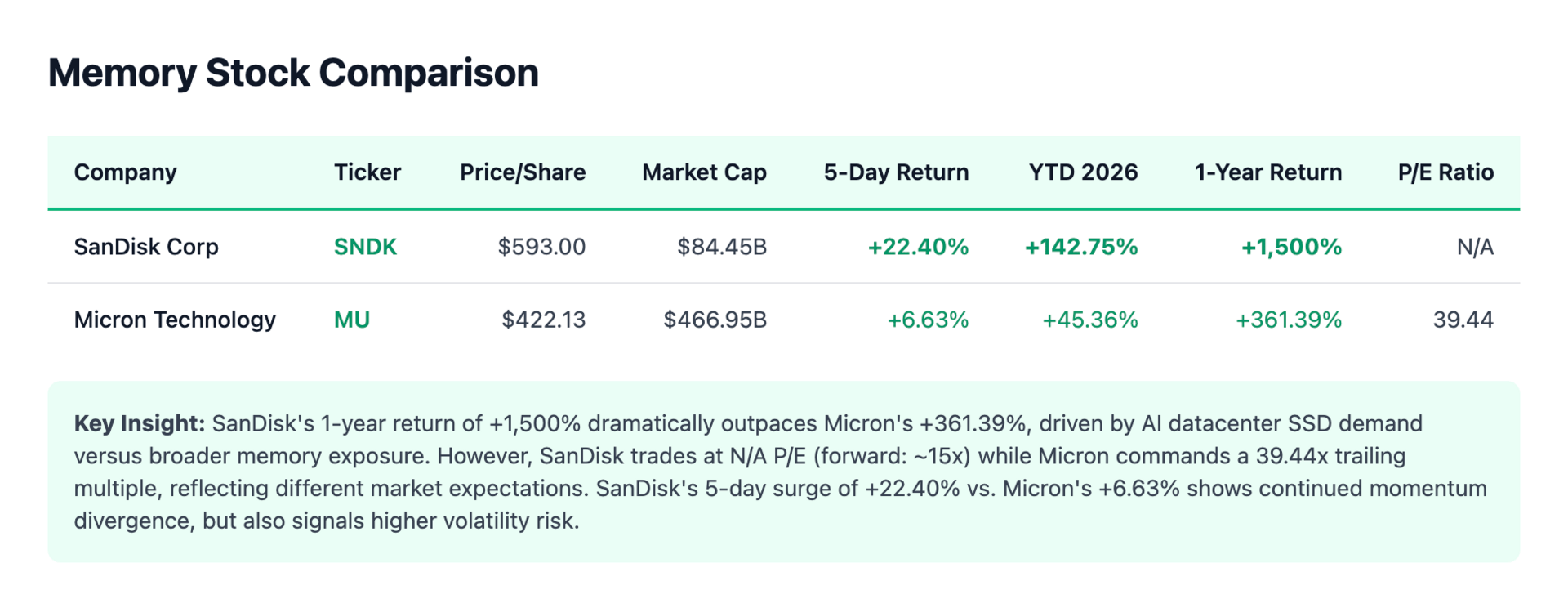

SanDisk just went from $36 to $593 in one year. Analysts think it could hit $1,000. |

$SNDK ( ▲ 6.85% ) traded at $36 exactly one year ago. |

Yesterday it's sitting around $593. That's a 1,500% gain in 12 months, not in some penny stock or crypto gamble, but in a NAND flash memory company that most people forgot existed. |

And here's the thing: Wall Street analysts aren't calling it overpriced. They're raising price targets to $700, $800, even $1,000. |

|

Business Model |

|

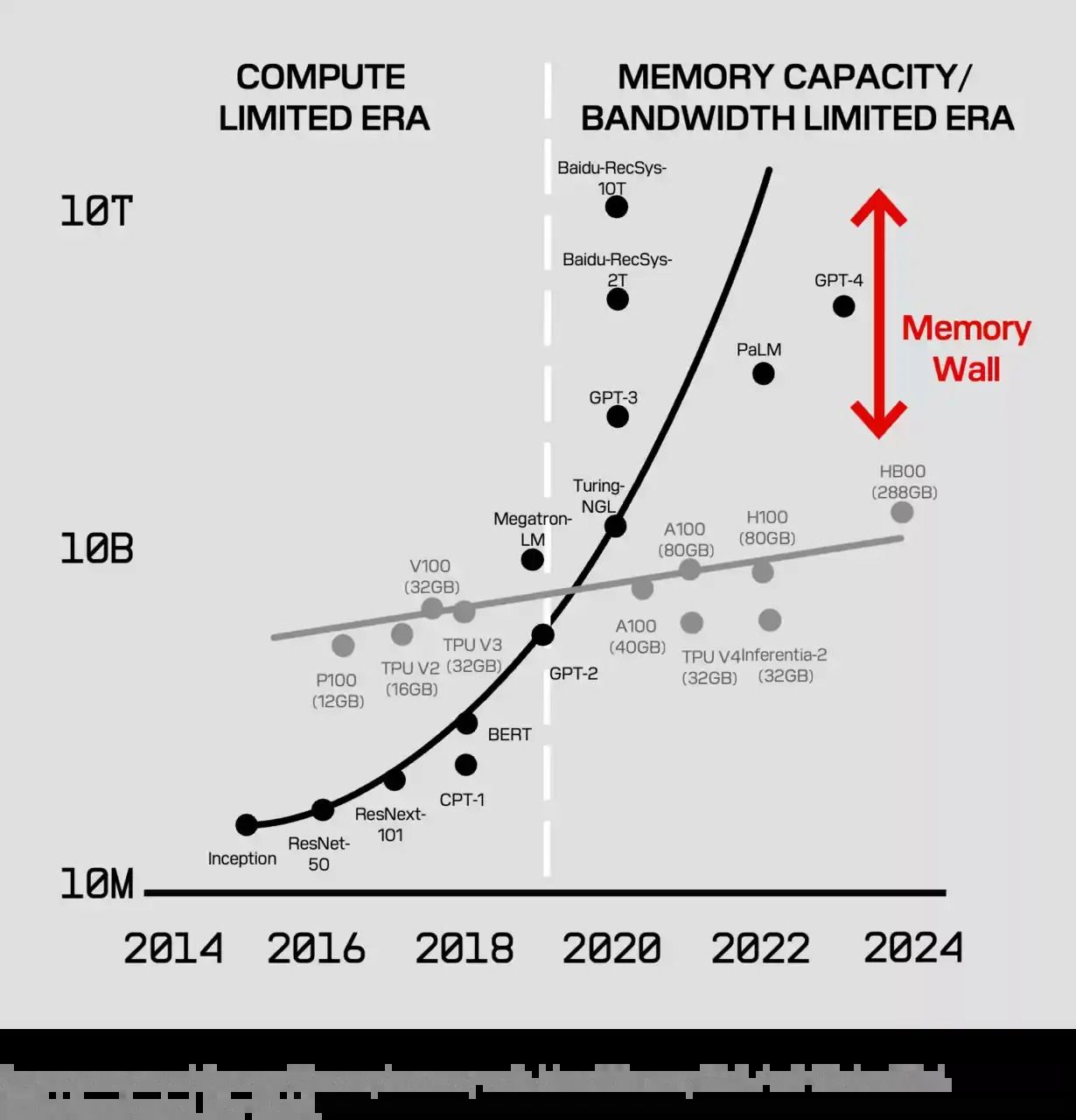

AI doesn't just need GPUs. It needs somewhere to store massive amounts of data—model weights, training datasets, inference logs. SanDisk makes enterprise SSDs that handle that storage. |

The memory wall problem is creating significant challenges in the datacenter and for edge AI applications. |

HBF is our answer to this problem. This NAND-based architecture offers 8x to 16x the capacity of High Bandwidth Memory (HBM), while delivering the same read bandwidth at the same price points. |

In the datacenter, SanDisk sees HBF augmenting HBM with the ability to attach terabytes of memory to GPUs. |

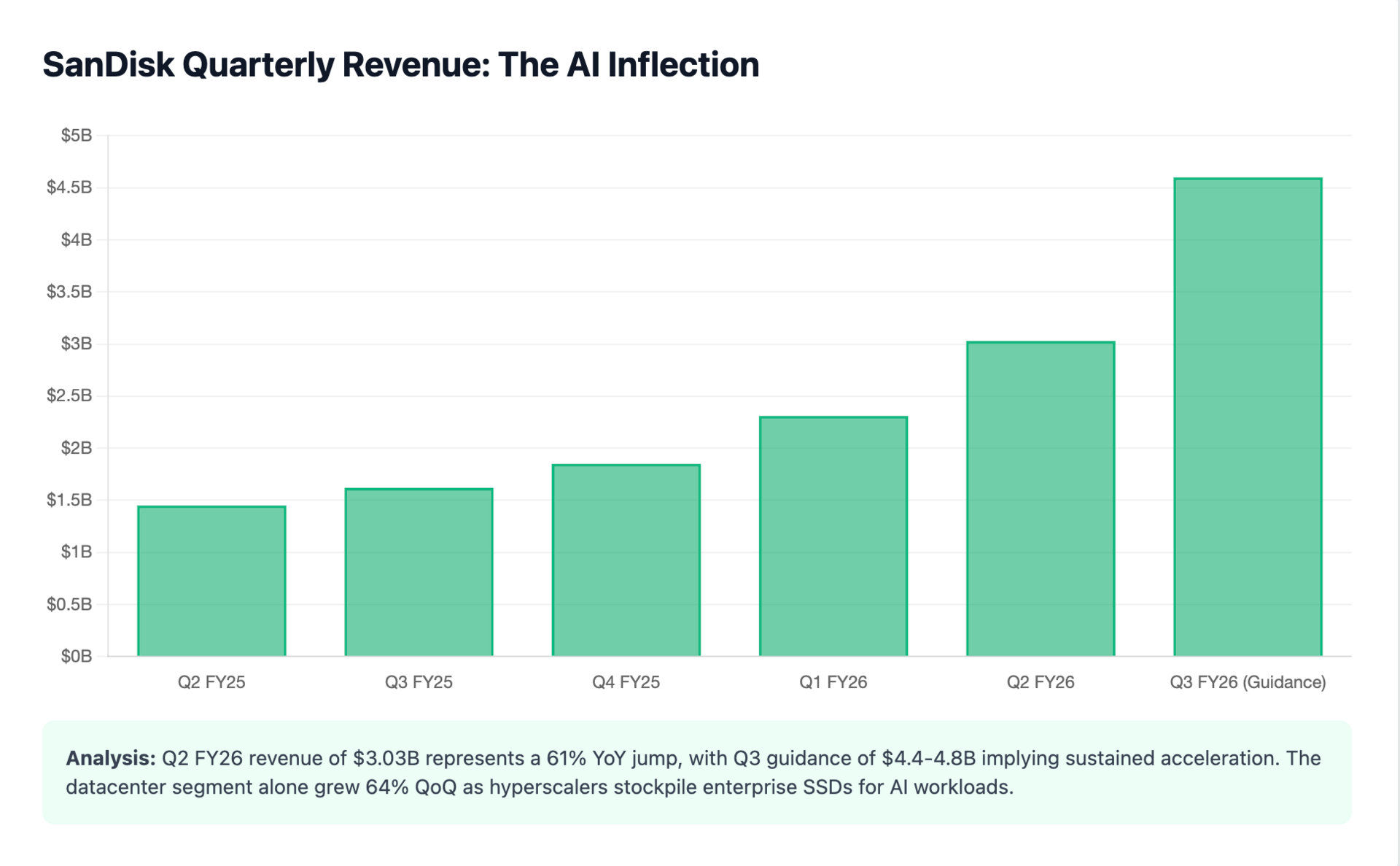

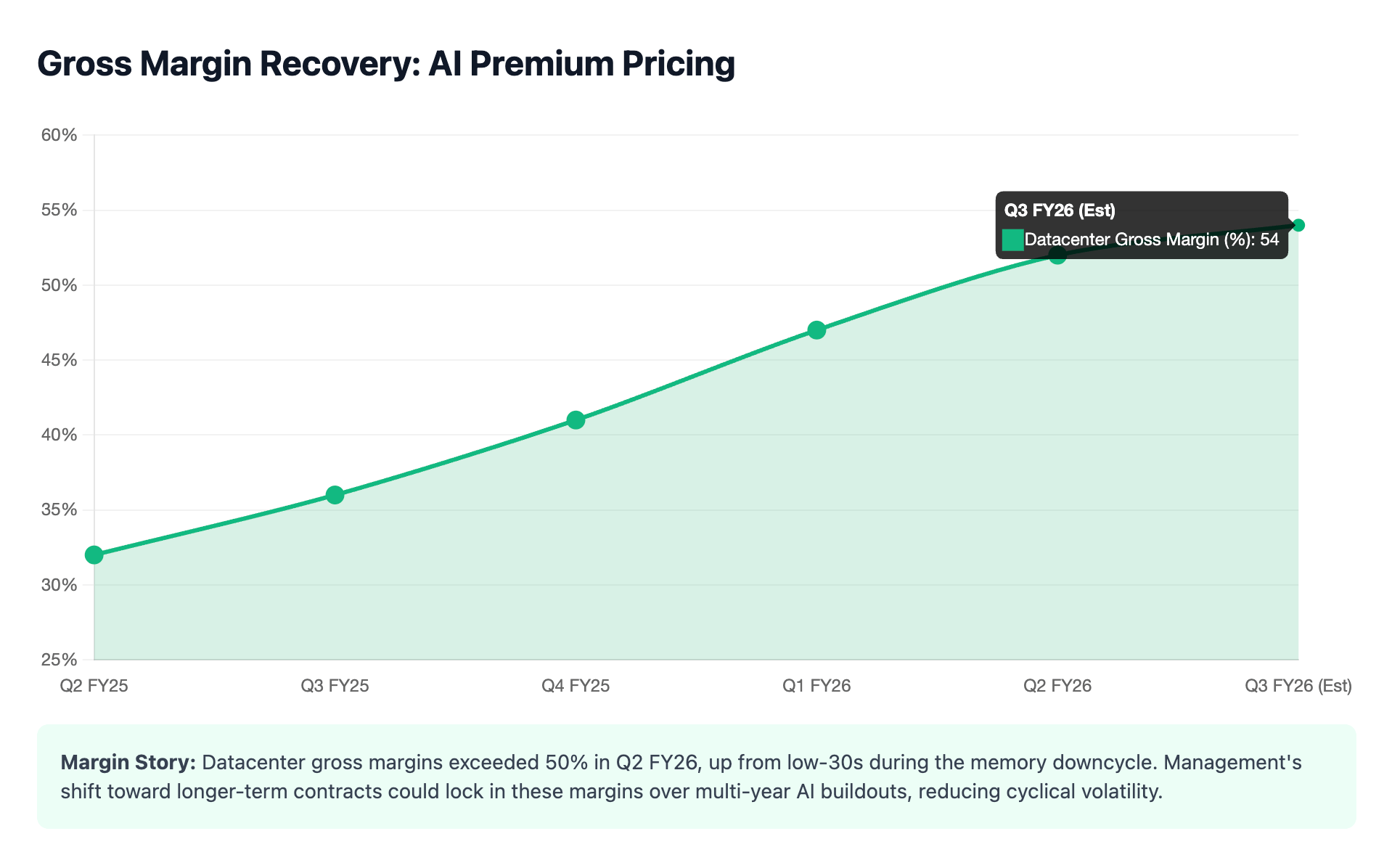

Q2 fiscal 2026 revenue hit $3.03 billion, up 61% YoY. |

|

Datacenter revenue alone jumped 64% QoQ. Gross margins crossed 50%. The company guided Q3 revenue between $4.4 and $4.8 billion when analysts expected maybe $2.9 billion. |

That guidance gap matters more than you might think. |

When a company beats expectations by 10%, the Street takes notice. When they double the consensus forecast, something structural is happening. |

In this case, it's hyperscalers and AI infrastructure builders buying far more enterprise SSDs than anyone predicted six months ago. |

|

But Here's the Catch |

$SNDK went from $539 to an intraday high of $676 in a single trading session. |

Volume hit over 20 million shares. That's not normal price discovery. |

Real on-the-ground question: Is this an early-stage AI infrastructure play that could run for years, or is it a memory cycle spike dressed up in AI hype? |

Management says demand will exceed supply through at least 2026. |

They're talking about moving customers to longer-term contracts with fixed pricing, something memory vendors almost never do. That would lock in economics over multi-year AI buildouts instead of riding the usual boom-bust cycle. |

Bernstein raised their price target to $1,000 and projected fiscal 2027 earnings per share at $90.96. At today's $593 price, that's only 6.3x forward earnings. |

Goldman, Jefferies, and RBC all moved targets to the $650-$700 range. |

|

The Valuation Question |

|

Here's where it gets messy. |

If you believe SanDisk is now an AI infrastructure company, not just another memory chipmaker, then a mid-teens P/E on 2027 earnings makes sense. That puts fair value somewhere in the $550-$650 band, which is basically where it's trading now. |

But if you haircut those bullish earnings estimates by 30-40% to account for competition and cyclicality, then $SNDK is already pricing in a lot of optimism. |

A more conservative entry price would wait for a pullback toward the $400-$500 range. |

The technical picture doesn't help. When a stock moves 25% in one day on massive volume, it's signaling either a major regime change or an overshoot that will mean-revert. |

Nobody knows which until after the fact. |

| | Big T's $5 Million AI Bet | Big T is going all in on what he believes will be the hottest trend in 2026. | With this strategy… | | He believes you'll have the chance to capture massive gains while protecting your money against any AI bubble risk. | He's so confident, he's put over $5 million of his own money into it. | Click here to see why | *ad |

| | |

|

|

|

CEO David Goeckeler keeps emphasizing that this isn't a one-quarter fluke. He's talking about "industry-leading financial performance" and structural resets that position the company for sustained high margins. |

The CFO keeps repeating that demand will outstrip supply. If true, that's pricing power. If it's just talking up the stock, well, that's also what CFOs do. |

Cantor Fitzgerald's analyst called SanDisk's enterprise SSDs "critical enablers" of hyperscale AI infrastructure, putting them in the same category as GPUs and networking gear as a core bottleneck. |

Several research notes frame this as early innings of a multi-year AI capex cycle. They also explicitly warn about volatility given how far the stock has already run. |

|

The Extended JV Move |

SanDisk extended its Yokkaichi joint venture with Kioxia through 2034 to lock in NAND supply. They're also evaluating a shift from short-term contracts (over 90% of sales today) toward longer-term agreements. |

That would be a structural change in how memory vendors capture value in the AI era. It would also reduce cyclical volatility, which is the main reason memory stocks historically trade at low multiples. |

If they pull that off, the AI premium baked into the current valuation starts to make more sense. |

|

So What's a Fair Entry Price? |

At $593, you're somewhere in the middle. Not cheap, not absurdly expensive, but definitely not undiscovered. |

For a multi-quarter position focused on AI infrastructure rather than trading momentum, staged entry makes more sense. Start small, add on 20-30% pullbacks toward support levels. |

|

Potential Risks |

|

It's not competition from Samsung or SK Hynix. It's not even cyclic. |

It's that the stock has gone parabolic in a year, options are pricing in wild swings, and retail traders are piling in after the move is mostly done. When a stock becomes a meme, even one backed by legitimate fundamentals, it can overshoot in both directions. |

The Q3 guidance was spectacular. If the company meets or beats that, $SNDK probably holds. |

If they miss, or if macro sentiment wobbles, or if AI infrastructure spending shows any sign of slowing, this could give back 30-40% in a hurry. |

|

Bottom Line |

SanDisk is riding real AI demand, not just hype. |

Datacenter revenue is up 64% QoQ. |

Management is guiding to numbers that imply a step-change in earnings power. Analysts who actually cover semiconductors are raising targets, not calling it overvalued. |

But $SNDK has also gone from $36 to $593 in a year. |

Momentum that extreme doesn't reverse gently. It either consolidates for months or it crashes back to reality. |

If you're looking at this for the long term and believe the AI storage thesis, wait for a pullback. |

If you're already in, maybe take some profits and let the rest ride with a tighter stop. |

And if you're thinking about jumping in right now at $593 because you're afraid of missing out?

That's exactly when you should wait. |

|

| | | | Quick ratingHow was this one? | |

| |

| | |

|

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions. |

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers. |

Tidak ada komentar:

Posting Komentar