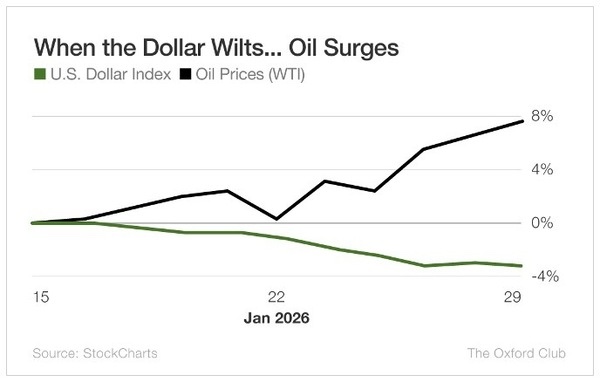

| This week, Treasury Secretary Scott Bessent said the U.S. has a "strong dollar policy." That's simply not true. And that's bad news for savers. Just a day before Bessent's statement, President Trump himself said of the dollar's decline, "I think it's great." The president has long been an advocate for a weak dollar, as it improves exports. However, it destroys savings. A weak dollar also means imports are more expensive, and since so much of what we buy comes from outside the U.S., that adds to inflation. Oil, priced in dollars, typically rises with the fall of the dollar as well. You can see on this chart that when the dollar started to decline rapidly in mid-January, oil prices took off. The decline of the dollar is also one of the reasons gold and silver have gone parabolic. The U.S. dollar is down 12% since inauguration day last year. Even if the dollar rebounds and doesn't deteriorate your savings, the banks will. The average interest rate on a savings account is below 0.4%. The average money market account pays less than 0.6%, and the average one-year certificate of deposit will earn you a whopping 1.6%. Meanwhile, inflation is currently at 2.7%. The takeaway is clear: Your savings accounts are destroying your buying power. And with the president's determination to keep interest rates low, that's not likely to change anytime soon. So what can savers do? For one, you can buy some T-bills. Currently, 3- and 6-month bills are paying slightly more than 3.5%. But when the bills mature, you may have to reinvest at a lower rate if rates go down (as President Trump is pushing for). Those who can take on a little more risk can buy quality dividend growth stocks. That way, they can get paid at least as much as T-bills, but with the very high chance that those payments will increase every year, which will actually grow your buying power. Lastly, there's an investment that I love right now that has generated an average annual return of 29% for the last 25 years. It's a conservative way to play the AI boom without investing in ultra-volatile stocks, unproven technologies, or any of the companies that have all that circular financing (where one invests in the other, which buys chips from the third, which owns a significant portion of the first). None of that nonsense. Just a company with a tremendous track record that was doing business decades before AI entered the mainstream. Click here to find out more about what I call "The 29% Account." Good investing, Marc |

Tidak ada komentar:

Posting Komentar