|

|

The ground beneath your feet is worth trillions. And in 2026, investors are finally waking up to it. |

Geothermal energy just hit a tipping point. We're not talking about those old-school hot springs anymore. |

This is next-gen tech that's pulling 24/7 clean power from miles underground—no sun required, no wind needed, no batteries necessary. |

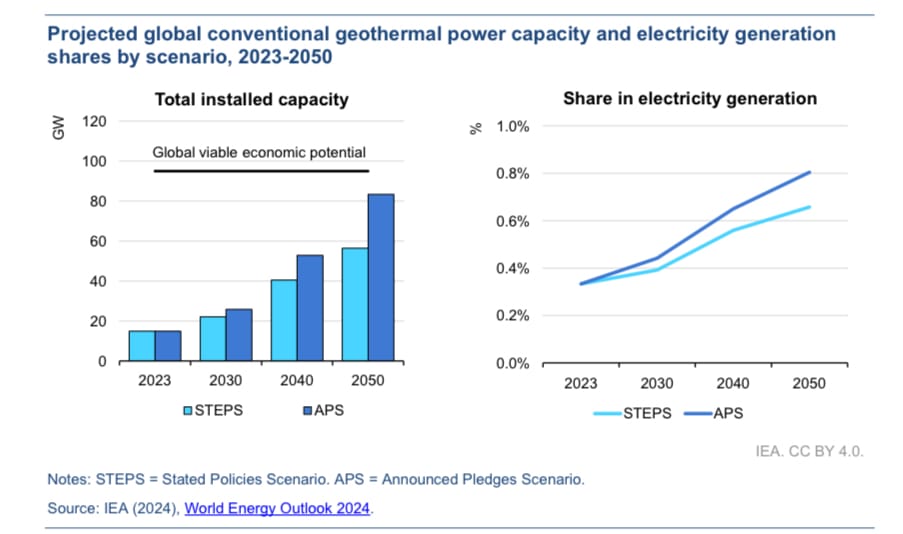

Here's what we know: the International Energy Agency says geothermal could supply 15% of global electricity growth through 2050. |

|

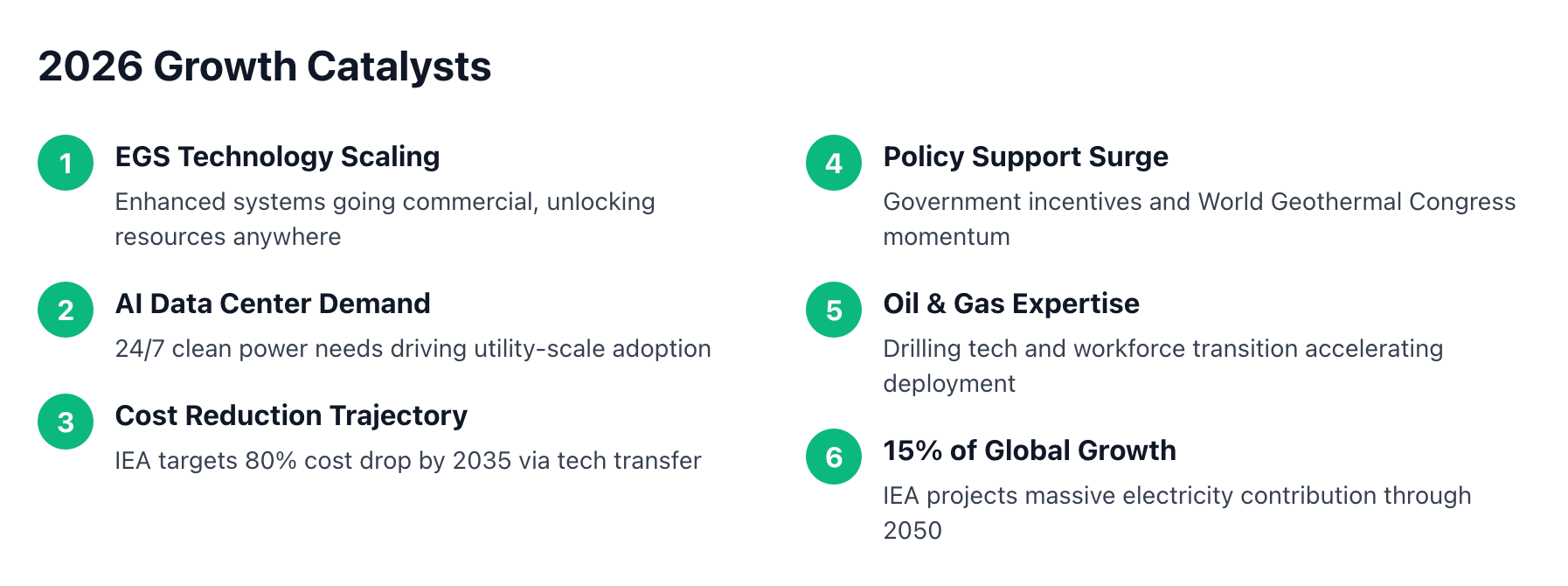

Why 2026 Changed Everything |

|

Three things happened that flipped the script: |

Technology finally caught up. Enhanced Geothermal Systems (EGS) and closed-loop drilling mean we can now tap heat anywhere, not just near volcanoes. Oil and gas companies are bringing their expertise, cutting costs fast. |

Policy opened the floodgates. Government incentives are pouring in. The World Geothermal Congress in Calgary this year put American innovation front and center. |

AI entered the game. Machine learning now optimizes drilling, predicts reservoir behavior, and cuts operational waste. Real on-the-ground improvements, not hype. |

|

The timing matters. Data centers need baseload power for AI. Electric grids need reliability. Industries need to process heat. |

Geothermal delivers all three without carbon emissions. |

That gap between what the grid needs and what solar and wind can provide? |

Geothermal fills it perfectly. |

| | | | What catalyst do you think actually matters most? | |

| |

| | |

|

| | Tesla's Smart Home Vision. Apple's Big Move. One Startup Owns a Crucial Piece. | Elon Musk is building the Tesla Smart Home.

Apple is doubling down with new Face-ID locks and smart displays.

The world's biggest tech giants are battling for dominance in the $158B smart home market, growing 23% each year. | | Big Tech is pouring billions— the race is officially on.

Just like how Google acquired Nest for $3.2 Billion and Amazon snapped up Ring for $1.2 Billion, investors are hunting for the next smart home breakout.

As Tesla and Apple race ahead, one startup is riding the wave—leading a massive, overlooked category - smart shades. And RYSE is dominating it.

RYSE checks every box: | 10 granted patents Over $12M in revenue 200% annual growth

| RYSE is not just another smart gadget—it's a prime acquisition target in a category with billion-dollar potential.

At just $2.35/share, investors can still get in early—before their next wave of growth.

The next Nest or Ring could be this.

Invest in RYSE now | | This email contains a paid advertisement for the Ryse Regulation A+ offering. Please review the offering circular at https://invest.helloryse.com/ |

| | |

|

|

The Geothermal Revolution |

|

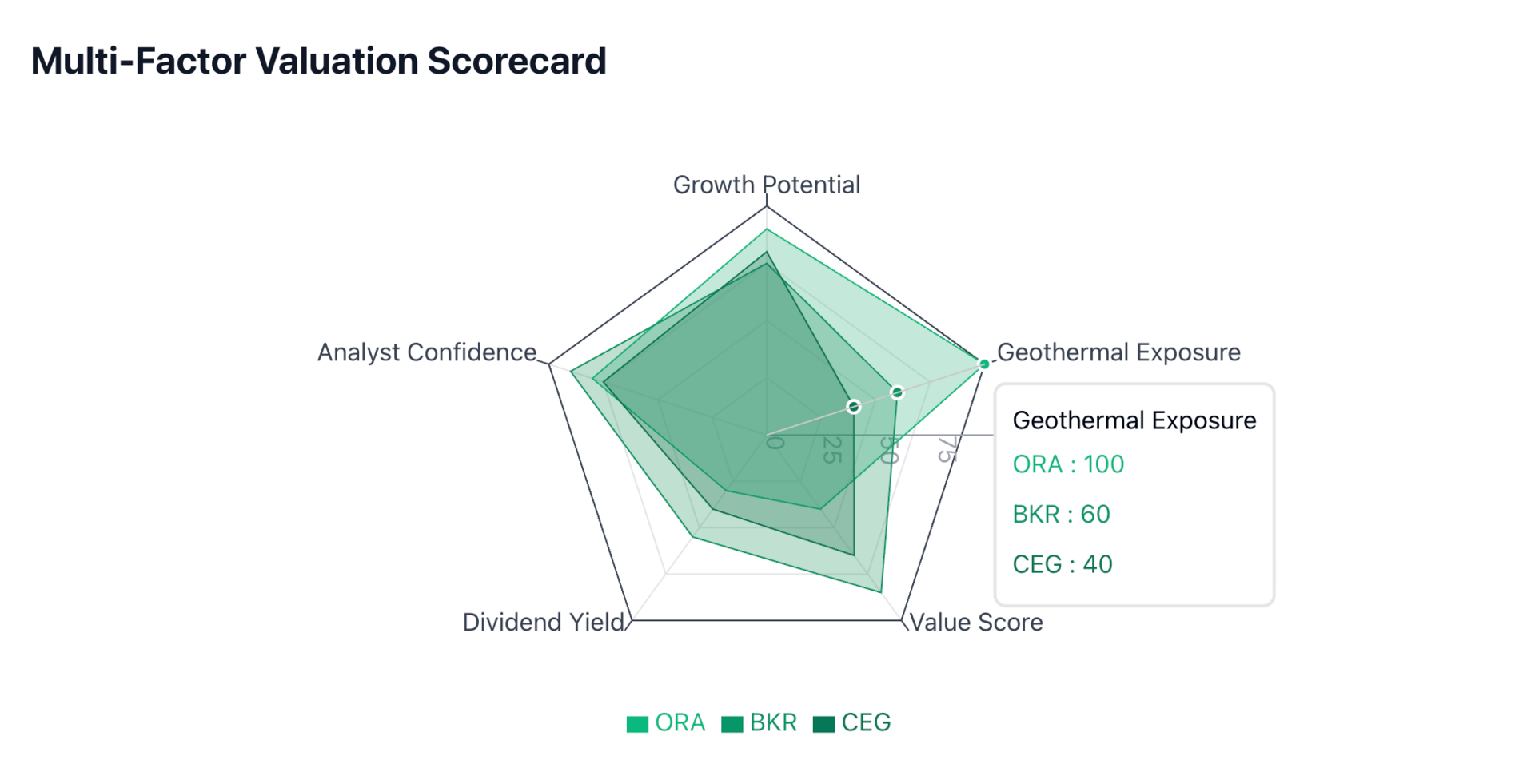

Let's cut through the noise. Three companies dominate this space, each with a different angle. |

Ormat Technologies $ORA ( ▲ 0.34% ) is pure play. They design the turbines, build the plants, and operate them globally. Think vertical integration. They're targeting 2.6-2.8 gigawatts of capacity by 2028. If geothermal wins, ORA wins directly. |

Baker Hughes $BKR ( ▼ 0.99% ) brings the drilling muscle. They're applying oil field technology to geothermal projects—surface equipment, reservoir analysis, risk mitigation. They're not just selling shovels in a gold rush; they're financing the mines and taking equity stakes. |

Constellation Energy $CEG ( ▲ 0.6% ) plays it differently. They're a massive clean energy utility with nuclear and renewables. Geothermal isn't their main focus, but it complements their baseload strategy perfectly. |

Different exposure levels. Different risk profiles. Different opportunities. |

|

How They Actually Make Money |

Business models matter more than stock tickers. |

Ormat runs the full cycle. They manufacture equipment, develop projects, operate plants for decades, and collect steady cash flow from power purchase agreements. High upfront costs, but predictable revenue streams once plants are running. |

Baker Hughes sells services and technology. Drilling contracts, equipment leases, consulting fees. But they're also moving into project finance—taking equity positions to share upside when projects succeed. Lower capital requirements than Ormat, but tied to industry growth. |

Constellation generates power at utility scale. Geothermal fits into their renewables mix as a reliable baseload. Less pure exposure, but more diversification. They're betting on the overall clean energy transition, not just one technology. |

|

The Head-to-Head Comparison |

|

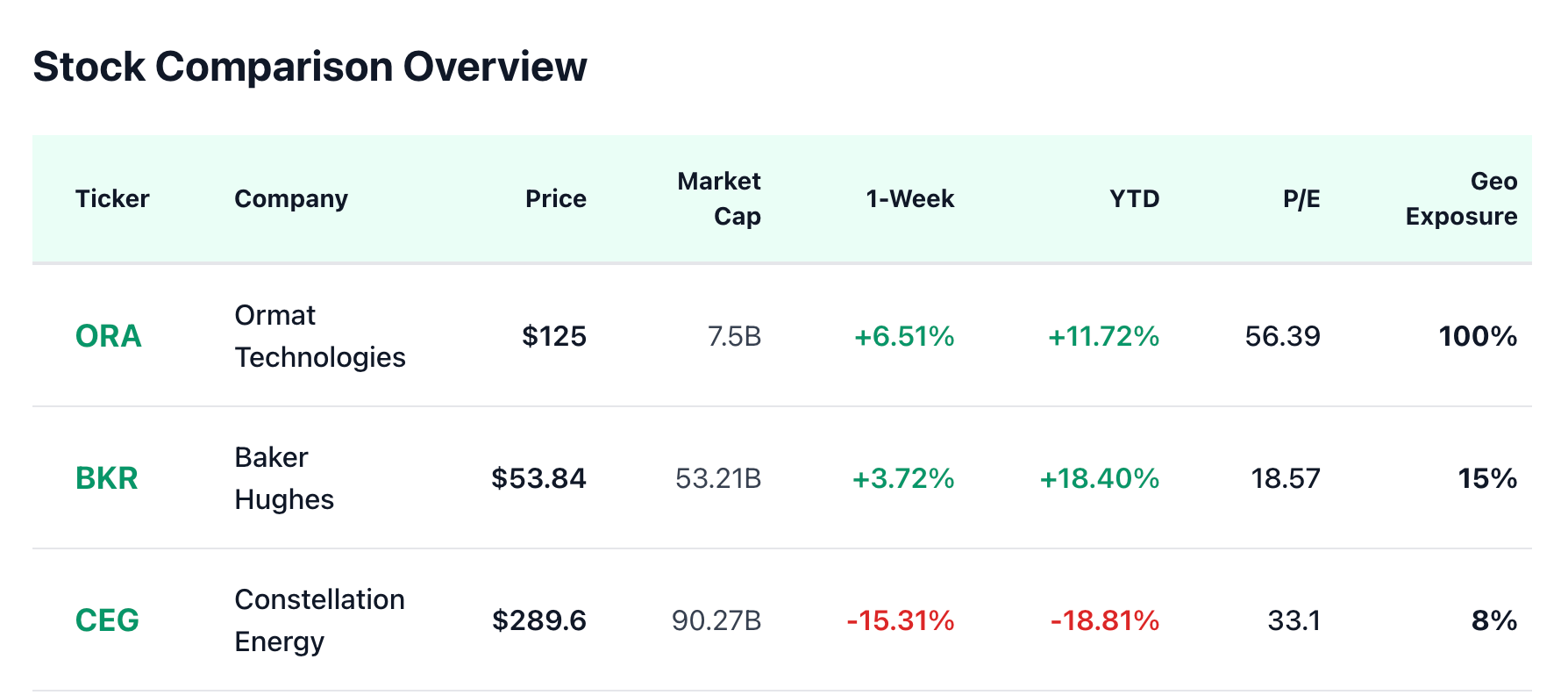

Here's how they stack up with the latest data: |

Ormat Technologies (ORA) just hit its price target. Trading at $125, $ORA proved analysts right with a strong +11.72% YTD performance. But here's the catch, it's now trading at the level analysts said was fair value. The 56.39x P/E ratio still commands a premium, and new targets sit around $135. That's only 8% upside from here. |

Baker Hughes (BKR) is the surprise winner. Up 18.4% YTD, the market is finally recognizing their geothermal pivot. At $53.84, they're close to analyst consensus but still show 17% upside to the $63 fair value. The 18.57 P/E ratio means you're not paying for hype, you're getting proven execution at a reasonable multiple. |

Constellation Energy (CEG) tells a different story. Down 18.81% this year, the stock took a beating. Now at $289.60 with a 33.10 P/E, it's trading well below the $370 analyst target. That's 27.8% upside—the highest of the three. But you need conviction that the selloff was overdone and the clean energy thesis still holds. |

|

|

The numbers shifted, and so did the opportunity. |

Ormat (ORA) achieved what most stocks dream of—it hit analyst targets. The run from $106 to $125 validated the pure-play geothermal thesis. New price targets around $135 suggest modest upside from current levels. The 56.39x P/E still prices in significant growth expectations. You're paying for execution now, not potential. |

Fair entry point: Current price is the fair entry. You're buying proven execution, not a discount. |

Baker Hughes (BKR) keeps delivering. The +18.4% YTD return leads the pack, but DCF analysis still shows fair value around $63. That's 17% higher than today's $53.84. The 18.57 P/E ratio is reasonable for their geothermal services growth trajectory. 19 analysts maintaining "Buy" ratings tells you the street sees more room to run. |

Fair entry: Right now at $53.84, still undervalued despite the gains. |

Constellation (CEG) became the value play nobody expected. The -18.81% drop this year created a gap between price and potential. Analyst targets averaging $370 imply 27.8% upside, the largest opportunity of the three. The 33.10 P/E sits between ORA's premium and BKR's value, suggesting the market is uncertain about direction. |

Fair entry: Current levels around $289.60 if you believe the selloff was excessive. |

| | What is the Golden Paradox? | If you missed out on gold's recent run … | You've been given a second chance. | Because the gold market is moving to the next phase. | Something we call the Golden Paradox. | It's a hidden opportunity that's played out for nearly 100 years. | A way that could've helped investors make 31 times more … | 65 times more … | Even 469 times more than just buying gold. | To solve this Golden Paradox, click here | *ad |

| | |

|

|

What Smart Investors Are Watching |

The performance divergence changed everything. |

BKR's momentum raises a question: is the geothermal story already priced in, or is this just the beginning of recognition? The 18.4% gain suggests the market is waking up, but 17% upside remaining says there's still meat on the bone. |

ORA's target achievement forces a decision. You got what you wanted—validation of the geothermal thesis. But buying here means you believe the next leg up comes from execution, not multiple expansion. That 8% upside to $135 won't excite growth investors. |

CEG's collapse creates the biggest debate. Did investors overreact to short-term headwinds? Or did fundamentals actually deteriorate? The 27.8% upside looks attractive, but you're catching a falling knife unless you have conviction about the turnaround. |

Three stocks, three completely different risk-reward setups than just weeks ago. |

|

The Real Risk Nobody Talks About |

When BKR outperforms by nearly 7% YTD, and CEG underperforms by 30 points, you're not looking at random noise. You're looking at market re-pricing of the entire clean energy narrative. |

ORA's ascent to target proves geothermal works as an investment thesis. But it also means early movers captured most of the easy gains. |

BKR's surge shows the market values diversified exposure plus geothermal upside. But chasing momentum at these levels means less margin of safety. |

CEG's collapse tests your conviction. Is this a buying opportunity or a value trap? The answer determines whether that 27.8% upside is real or wishful thinking. |

The bigger risk isn't technology anymore. It's position timing and portfolio psychology. |

|

What This Means |

The allocation strategy just got more nuanced. |

If you're building a new position: |

BKR offers the best risk-reward at current levels—proven momentum with 17% upside remaining CEG presents the contrarian bet—highest upside but requires strong conviction ORA gives you pure exposure at fair value—you're paying for quality, not getting a deal

|

If you already own these stocks: |

ORA holders should consider taking partial profits after hitting targets BKR holders have room to let winners run with trailing stops CEG holders face a hold-or-fold decision based on turnaround conviction

|

New portfolio construction: |

50% BKR (momentum + value combo) 30% CEG (calculated contrarian position) 20% ORA (pure play allocation at fair price)

|

This weighting reflects current risk-reward asymmetry, not theoretical exposure targets. |

|

Final Word |

The ground beneath your feet still generates enough heat to power civilization. |

But the stocks that profit from it just sorted themselves into clear categories. |

Baker Hughes seized momentum. Ormat achieved validation. Constellation created controversy. |

Six months ago, the opportunity was speculation. Today, BKR proved the thesis. ORA delivered on promises. CEG tested investor conviction. |

The question isn't whether geothermal works anymore. The question is which entry point matches your risk tolerance and which performance trend you believe continues. |

One thing's certain: the market is no longer sleeping on geothermal. |

The only question is whether you positioned yourself before the wake-up call. |

|

| | | | Quick ratingHow was this one? | |

| |

| | |

|

Disclaimer: This analysis is for educational purposes only and should not be considered investment advice. Always do your own research before making investment decisions. |

Items marked with an asterisk (*) are promotional and help support this newsletter at no cost to readers. |

Tidak ada komentar:

Posting Komentar