| TQ Morning Briefing | The Cut Is Priced. The Dot Plot Is the Battlefield. | | | | | | Markets arrive at decision day in a familiar posture. Seemingly calm, but poised to get volatile. | Futures drift modestly higher. The dollar softens at the margins. Precious metals continue to glow. Yields press upward. And yet the tape itself barely moves. The Fed is finally here, and the market has already decided what the headline will be. | A 25 basis point cut is fully priced. | What is not priced is how far Powell lets the easing story travel into 2026. | This is not about whether the Fed moves. It is about whether December marks a waypoint or a pause. Growth remains intact. Inflation remains sticky. Labor cools without breaking. The Fed now sits at the most unstable equilibrium of the cycle. | Markets are not waiting for rates. They are waiting for permission. |

| |

| | |

| | | | Triple the Market's Dividend + Explosive AI Growth… Still Trading for $5? | This dividend-paying manufacturer just dropped a bombshell: AI server revenue is projected to surpass iPhone revenue within 24 months. | ✔ Builds most of Nvidia's AI servers

✔ Pays nearly 3X the S&P 500 dividend

✔ $30+ billion in AI revenue projected THIS YEAR

✔ Yet the stock still trades for around $5 | While other tech names struggle, this hidden AI dividend gem keeps climbing. | Alexander Green calls it his "Single-Stock Retirement Play." | Click here for Alex Green's full analysis and ticker. |

| |

| | |

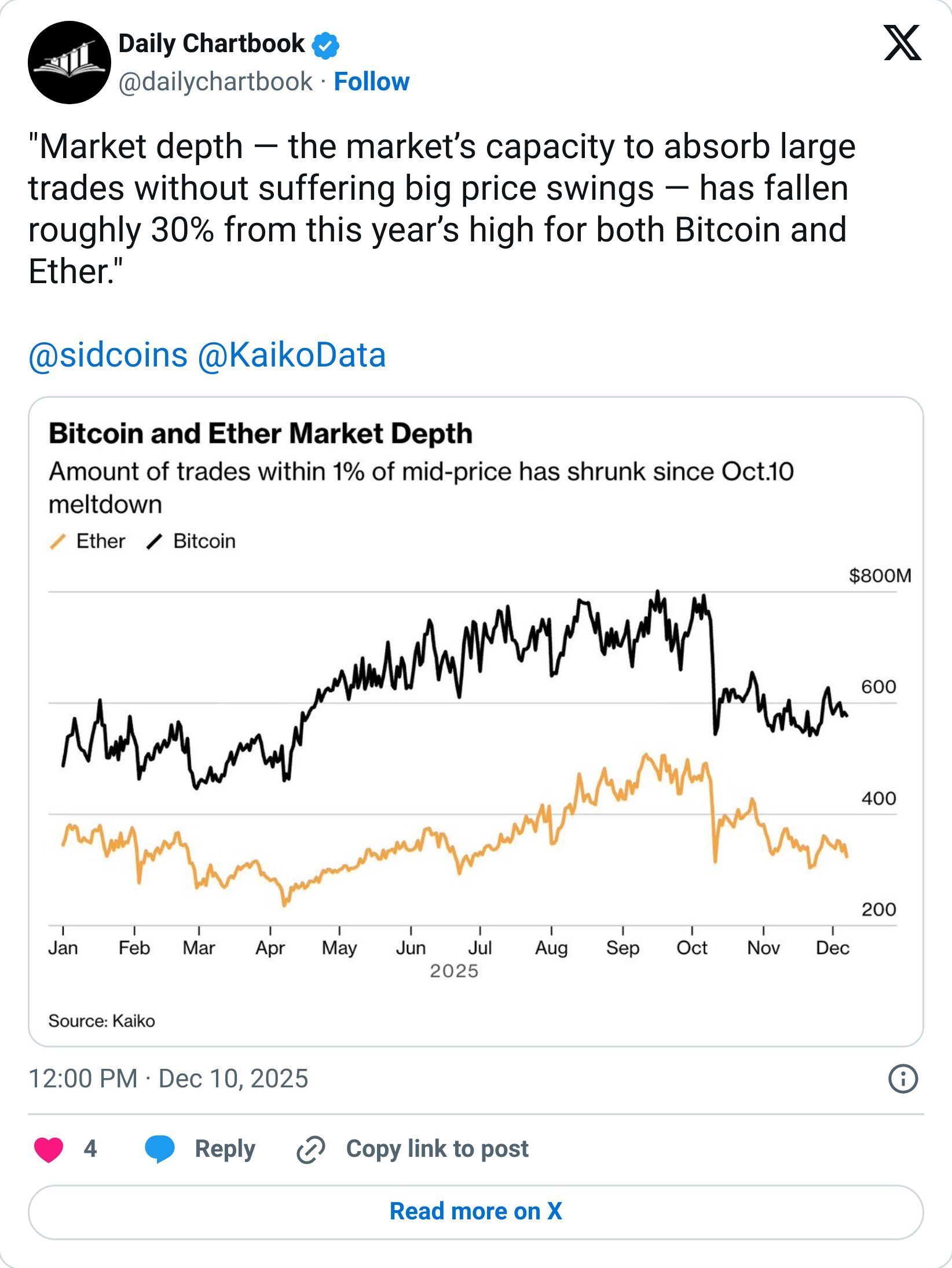

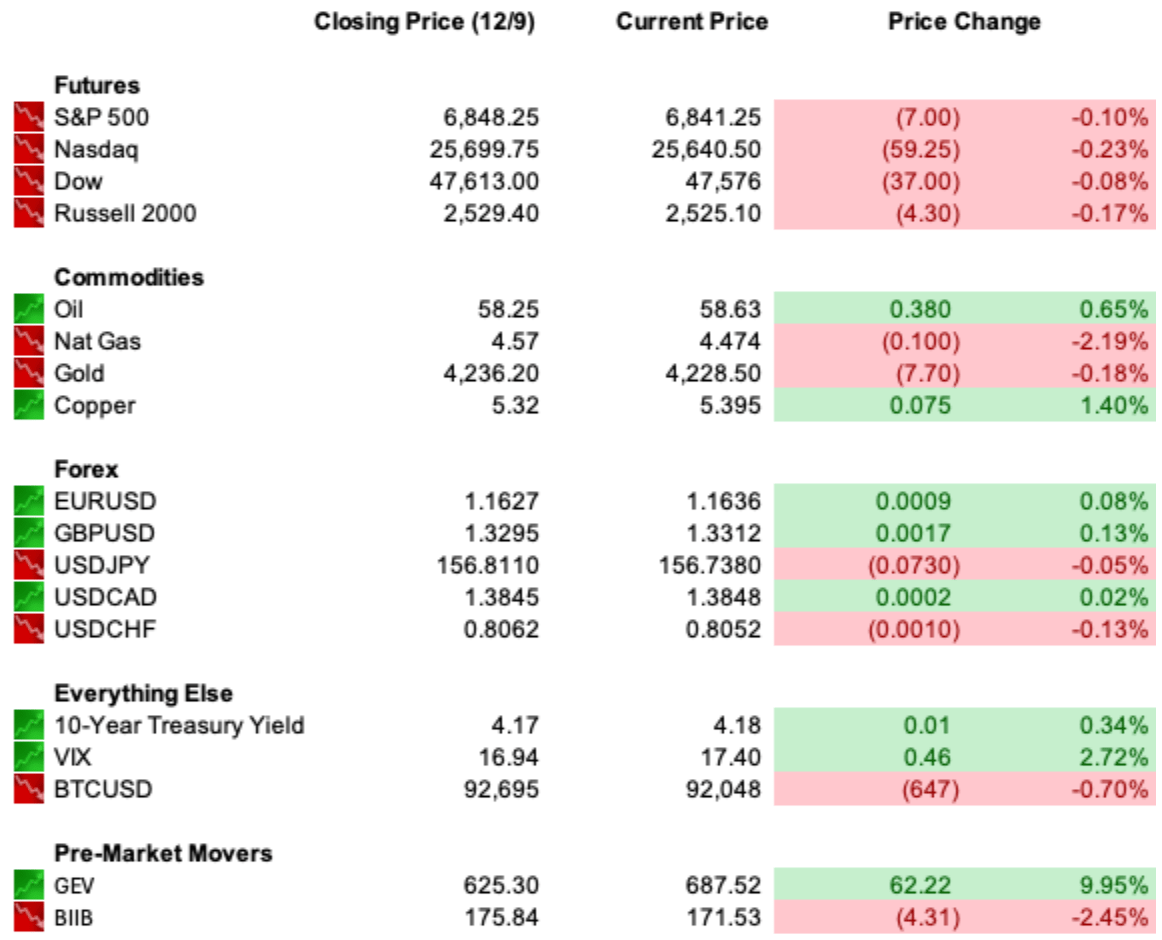

| | | | Equities are drifting into the final FOMC decision of the year with indexes pinned near record highs and positioning stretched but unresolved. | S&P futures have barely moved overnight, after several stagnant sessions. The Dow and Nasdaq remain within reach of recent peaks. Small caps continue to quietly outperform, with the Russell 2000 printing fresh highs as rate sensitivity pulls capital down the size spectrum. | Yields stay the anchor. The 10 year Treasury sits near 4.20 percent, holding pressure on valuations and reinforcing expectations of a hawkish cut rather than an open ended easing cycle. | Gold is holding above 4,200 and Silver continues its historic surge above 61 dollars an ounce. Oil prices remain under pressure as supply accumulates in transit. Natural gas tagged three year highs and has been in a hurry to give it back ever since. | Crypto has re-entered the risk conversation. After spending the back half of November bouncing between $80k and $90k, an equilibrium is holding around $92k, though that can change in a hurry. Liquidity expectations, not adoption narratives, are driving the move. | | Technology continues to dominate. XLK is now up more than 27 percent year to date, logging its twelfth straight session of gains. Software and semis regain center stage with Oracle and Broadcom as the next volatility gates. | Trade headlines remain active beneath the surface. China resumes soybean purchases but remains far behind Trump era targets. Washington responds with a 12 billion dollar farmer aid package that markets increasingly view as a stopgap rather than a solution. |

| |

| | |

| | | | The Federal Reserve delivers its final policy decision of the year this afternoon. The market assigns an almost 90 percent probability to a quarter point cut into the 3.50 to 3.75 percent range. | The cut itself is consensus. The dots are not. | Futures markets have sharply downgraded expectations for 2026, with odds of three or more cuts collapsing below 30 percent. One or zero cuts now dominate the curve. That repricing has pushed yields higher over the past two weeks. | The December dot plot carries unusual weight because it includes what officials now believe policy should have been for 2025. That creates the possibility of soft dissents without formal votes against the cut. | How many officials quietly mark that they would have held is likely to be the most important data point in today's release. | The Fed remains divided. Doves focus on labor cooling. Hawks focus on inflation persistence. Powell must now land a cut with hawkish language and hold the risk of internal fracture at bay. | Global central banks remain largely frozen. The Reserve Bank of Australia held at 3.60 percent and signaled that the next move could be higher if inflation persists. Canada and Switzerland are expected to stay on hold. The ECB continues navigating a narrow corridor between weak growth and latent price pressure. | Currency markets reflect the divergence. The euro firms. The yen stabilizes after violent volatility ahead of the Bank of Japan meeting. The dollar drifts lower into the Fed. |

| |

| | |

| | | | | Trade Winds & Global Shifts |

| |

|

| | | China's export machine remains the central distortion in global trade. Despite renewed soybean purchases, the pace of Chinese buying remains far below the volumes promised under recent U.S. trade frameworks. Washington responds with subsidies while tariffs remain the policy backbone. | The U.S. Indonesia trade deal now teeters. Jakarta is accused of backtracking on non tariff barriers, digital trade commitments, and agricultural access. Washington signals that the deal itself may be at risk. | Across Europe, diplomacy frays. Trump openly criticizes European leaders as weak just as they scramble to prove relevance in Ukraine peace efforts. The transatlantic rift continues to widen beneath nearly eight decades of alliance architecture. | | Southeast Asia reenters the global risk map. Fighting between Thailand and Cambodia has reignited after a failed U.S. brokered ceasefire. Evacuations resume. Civilian infrastructure is hit. Regional risk premiums quietly creep higher across select ASEAN markets. | In Latin America, Chile is poised to elect its most right wing president since the Pinochet era. Markets have largely pre-priced the shift as part of a broader regional turn toward security and migration enforcement over redistribution. | China's domestic model remains under pressure. The IMF urged Beijing to accelerate its shift away from export dependence and toward consumption. Growth forecasts were raised, but the warning is unambiguous. China is now too large for the world to absorb its surplus without consequence. |

| |

| | |

| | | | [How To] Claim Your Pre-IPO Stake In SpaceX! | This is urgent, so I'll be direct… | For the first time ever, James Altucher – one of America's top venture capitalists – is sharing how ANYONE can get a pre-IPO stake in SpaceX… with as little as $100! | In other words, this is your first-ever chance to skip the line, and get in BEFORE Elon Musk's next IPO takes place. | Best of all, it couldn't be any easier… | When you act today, you can get a pre-IPO stake right inside your regular brokerage account, all with just $100 and a few minutes of time. | All you need is the name and ticker symbol that James reveals for FREE, right inside this short video. | [Click here now to view.] |

| |

| | |

| | | | | D.C. in the Driver's Seat |

| |

|

| | | Washington remains the dominant volatility engine across healthcare, energy, and trade. | Senate Republicans move toward a health savings account centered alternative to expiring ACA subsidies. Democrats reject the proposal outright as junk insurance. With enhanced Obamacare subsidies set to expire, millions of households face higher premiums in 2026 with no bipartisan solution yet visible. | Trump returns to the road to rewrite the affordability narrative. In Pennsylvania, he defends tariffs, blames Democrats for price pressures, touts tax cuts and drilling expansion, and openly embraces political confrontation as his midterm strategy hardens. | | Trade aid flows even as trade strains persist. Farmers receive 12 billion dollars in tariff funded relief while export markets remain structurally impaired. |

| |

| | |

| | | | Fed Interest Rate Decision

FOMC Economic Projections |

| |

|

| | | | Oracle (ORCL), Adobe Systems (ADBE), Synopsys (SNPS) |

| |

| | |

| | | | Asia: Nikkei -0.10%, Shanghai -0.23%

Europe: FTSE 100 +0.28%, DAX -0.42% |

| |

| | |

| | | | | | Before the AI Wealth Gap Widens, See This List | Blue-chip stability meets AI growth in The 10 Best AI Stocks to Own in 2026. | Inside: a top-10 dividend payer rolling out AI-powered logistics across 200 countries… a $300B titan embedding AI across its full product stack… and a semiconductor leader still trading 15% below its 52-week high. | All proven operators, all using AI to widen their lead. | See the list for free today |

| |

| | |

| | | | Today's trade is no longer about direction. It is about duration. | A quarter point cut is consensus. What will move markets is whether the Fed quietly tells traders how long risk can stay bid before yield pressure reasserts control. | If the dot plot confirms only one cut in 2026 and Powell leans into policy patience, expect a fast repricing across duration sensitive assets. Long bonds stabilize. High multiple software and semis face air pockets. Small caps stall after their recent momentum burst. | If projections reopen the easing path, the playbook flips. Liquidity expectations extend. Financial conditions loosen. The chase resumes into year end with technology, cyclicals, and crypto back in the lead. | Either way, today injects information into a market that has been trading almost entirely on assumption. | Volatility is not about the cut.

It is about how long the Fed lets momentum stay alive. |

| |

| | |

|

|

Tidak ada komentar:

Posting Komentar