December 31, 2024

5 Crypto Tax Tips That Can't Wait Till April

Dear Subscriber,

|

| By Beth Canova |

2024 was the second-best year on record for crypto.

If you followed your Weiss crypto editors’ leads this year, you should have some nice gains of your own.

For example,

- If you had followed Marija Matić’s guidance in Crypto Yield Hunter, you could have seen your DeFi portfolio outperform the market average by 5x to target multiple impressive yield opportunities boasting over 100% APY.

- You could have harvested three different triple-digit gains if you kept up with Juan Villaverde and Dr. Bruce’s small-cap crypto recommendations, plus a few rounds of smaller wins.

- And if you’re using Juan’s Weiss Crypto Portfolio strategy, you had the chance to harvest an average gain of 32% in your Long-Term Portfolio in 2024.

And you no doubt want to keep as much of those hard-earned profits as you can when Uncle Sam comes for his cut.

You still have some time before that infamous April 15 deadline. But April comes fast.

So, to close out this waning — and winning — year, I’m going to cover some crypto tax basics. I’ll also give you a few tools you may want to add to your arsenal.

Crypto Tax Basics

Like stocks, crypto is treated as property by the IRS, not currency.

The main difference is that you can use crypto directly to make purchases and trade them one for another.

You can also stake cryptos to earn additional yield, and you can “mine” new crypto instead of buying them.

You can’t do any of that with stocks. And so, with stocks, you are only taxed when you sell and realize gains.

In other words, certain activities involving cryptos trigger taxable events.

Learning about these events now will make filing simpler come tax season.

So, here are five of the more common taxable events you’ll likely encounter.

Taxable Event No. 1:

Receiving Crypto as Payment

Simply purchasing a crypto isn't a taxable event. Neither is holding it.

However, if someone pays you in crypto, it’s treated as income. Therefore, it’s subject to income tax.

Crypto is taxed based on your income tax bracket, the same as any other income.

Exactly how much you'll pay depends on the fair market value of the crypto at the time of the transaction.

Independent contractors and freelancers are subject to paying self-employment tax on crypto received as payment.

Meanwhile, businesses need to pay business income tax on profits earned by accepting crypto as payment.

Taxable Event No. 2:

Selling Crypto

For most crypto investors, the most important consideration is the capital gains tax you incur when you sell your crypto for a profit.

If the sale price is higher than its original purchase price, that is considered a capital gain.

You’ll need to report this gain and give a portion of your earnings to the U.S. government based on your income tax bracket.

To calculate capital gains tax, we first need to understand the cost basis, or the price you paid to purchase the asset.

In the case of crypto, that would be the spot price plus any fees paid during the process.

Let's say you buy $1,000 of Ethereum (ETH, “A-”) and pay $30 in fees to do so. Your cost basis would be $1,030. That’s the sum of the cost of the purchase plus the purchase fees.

To figure out the capital gains tax, you’ll need to go a step further and calculate the sale price minus any fees paid in the sale. In short …

- Cost basis = Purchase Price + Purchase Fees

- Capital Gain = (Sale Price — Sale Fees) — Cost Basis

So, if you sell that ETH for $2,000 and pay $50 in sales fees, your proceeds are $1,950.

Now that you have these two numbers, you can subtract them to get your taxable capital gain.

Take the $1,950 in proceeds and subtract the $1,030 cost basis and you get $920. That is your taxable capital gain.

Now that you know what's being taxed, the final step is to figure out the rate that taxable capital gain will be subject to.

That’s based on whether it's a short-term or long-term capital gain.

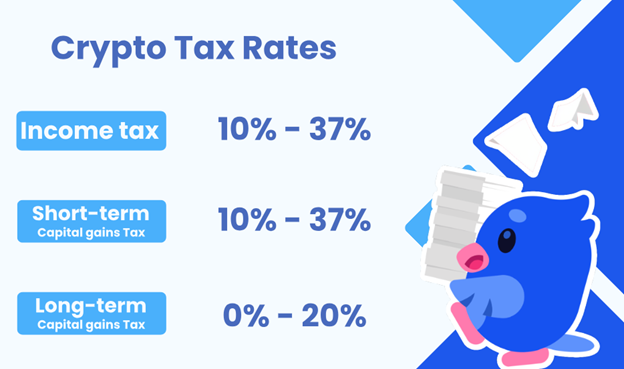

Short-term applies to any assets bought and sold within a year. As of the 2024 tax year, a short-term capital gain is taxed between 10% and 37%, based on your income.

Long-term applies to assets held for more than a year. As of 2024, those gains are taxed between 0% and 20%, based on your income.

As you can see, long-term capital gains are subject to a lower tax rate — even in the highest income bracket — than short-term ones.

So, if you don't have any need to sell before the one-year mark, you should avoid doing so.

Instead, allow it to convert into a long-term capital gain to lower your tax burden in the process.

Now, not every crypto went up this year. Or perhaps not while you were in the trade. But that’s not necessarily a bad thing.

If you lost money in the sale, you won't be required to pay any taxes on that transaction.

Accurately reporting capital losses isn't just required, it's also beneficial to investors. Capital losses offset the tax burden of capital gains in a given year.

For example, if you made $5,000 in capital gains this year, you'll be taxed on that $5,000. But if you had a capital loss of $1,000 and reported it, it would lower your capital gains to $4,000.

That lowers your taxable amount and thus saves you money.

Taxable Event No. 3:

Paying with Crypto or Swapping It

Buying things with crypto can trigger a taxable event.

In the eyes of the IRS, when you buy something with a crypto, you are essentially converting it from an investment asset into regular money.

This triggers a taxable event.

So, if you use Bitcoin (BTC, “A”) to buy a car, and the value of that BTC is higher than when you initially invested, the IRS considers that a realized capital gain.

Meaning, you’ll need to declare the sale and pay taxes on it.

The same goes for exchanging one crypto for another.

Again, as far as the IRS is concerned, you can't just trade one crypto for another, as that’s impossible with stocks.

To anyone involved in crypto, swapping is as simple as converting BTC into ETH.

But to the IRS, it’s as if you are swapping your BTC into U.S. dollars, and then buying ETH.

And if the value of your BTC when swapping is higher than when you purchased, you’ve technically realized a capital gain.

That’s why any gains or losses will need to be filed and will be taxed accordingly.

Taxable Event No. 4:

Mining and Staking

Crypto earned through mining or staking is treated just like income earned through stock dividends.

In other words, they're both subject to income tax.

- Mining is the process of solving complex algorithms to validate transactions and create new cryptos.

- Staking is a way to provide liquidity to a communal pool. In return, the network or platform gives you rewards, usually in the form of its native token.

Any rewards from mining or staking should be recorded and declared as regular income based on its fiat value on the day you received it.

If mining is a part of your business, you should declare the fruits of your labor as business income.

This way, you can deduct mining expenses — such as electricity, home office deductions, hardware and other expenses vital to your business — on your taxes.

Taxable Event No. 5:

Inheriting Crypto

Maybe you received a crypto inheritance this past year. Or you could consider leaving your holdings for your children.

Either way, you should be aware of the tax implications.

Crypto passed down from generation to generation may be subject to estate tax and capital gains tax.

The federal estate tax is only relevant if the total value of the estate is $13.99 million or more for individuals and $27.98 million or more for married couples.

If, under these rules, you are required to pay an estate tax, any crypto in the estate must be included.

The federal tax rate for an estate can range from 18% to 40% based on the exact size of the total estate.

In addition, there are 12 states and the District of Columbia that have additional estate taxes. Six more states have inheritance taxes.

Luckily for crypto heirs, upon the passing of the original owner, a step-up in basis occurs. This lowers the inheritor’s tax duties on the crypto.

A step-up in basis means that the new cost basis will be calculated based on the fair market value of the crypto at the date of the previous owner’s death. Not its original purchase date.

Assuming the asset has appreciated since its purchase, this gives the heir a higher cost basis and thus a lower capital gains tax.

How to Keep Track of

Your Crypto Taxes

Like everything else to do with taxes, accurate record keeping is essential.

To ensure you file correctly, you’ll need to put in some extra work compared to your non-crypto investor peers.

Most traditional exchanges offer 1099s, the tax documents which show investment income and transactions. But not all crypto exchanges issue 1099s.

As of 2023, all U.S.-based centralized crypto exchanges must send 1099s to investors. But if you’re a decentralized exchange user, you’ll need to do the legwork yourself.

Either way, I still suggest you put in a little extra diligence throughout the year and update a spreadsheet with every transaction.

The standard method is to faithfully log your crypto transactions and their fair market values as you invest and trade throughout the year.

That way, you can avoid having to backtrack through dozens, hundreds, or thousands of crypto transactions at the last minute.

There are also a few platforms that can offer some assistance, such as …

These services can help you track your transactions and the value of your crypto portfolio over the year to help make tax prep easier.

You can review a pros and cons list of these platforms and others here.

Whether you keep track with a pen and paper or use a sophisticated online tool, there’s no wrong answer. Just do the accounting as you go to avoid a stressful tax season later.

After all, filing correctly will keep you on good terms with the IRS. It can also lower your tax burden, which means more money for you and your family.

And, if nothing else, it can help you avoid unnecessary fees for filing incorrectly.

Best,

Beth Canova

Crypto Managing Editor

P.S. Cryptos had a banner 2024. So did gold, which started to surge the day the Fed started hinting at rate cuts.

Back in the 1970s, a cycle of lower rates helped propel gold up 262%. If just the whisper of a rate cut was enough to take gold up as much as 35% in a year, what will happen when the Fed slashes rates even more in 2025?

Adding gold now could be one of the smartest moves you make for 2025. That’s why everyone who watches this video is eligible to claim a Weiss-exclusive 2-gram gold bar, compliments of Dr. Martin Weiss, delivered straight to your house.

Click here now to see how you can claim yours.

Tidak ada komentar:

Posting Komentar