I hope you have enjoyed the relative stability of the stock market during first half of 2026 to the fullest.

Because two massive economic forces are colliding in real-time, and the result is set to upend everything we thought we knew about investing.

The first force: We're living through the fastest rate of technological change in human history. AI isn't just disrupting a few tech companies — it's threatening to make the world we know unrecognizable in just a few years.

The second force: Trade relationships and peace deals that have held our global economy together for decades are hanging by a thread. If that thread breaks, we're looking at an era of chaos that will make 2008 look like a minor correction.

And almost no one I talk to is prepared for it. Not yet anyway.

The Age of Chaos isn’t just another market cycle where you will eventually see the light at the end of the tunnel.

The Age of Chaos is a fundamental reshaping of the economic order. And when the dust settles, we'll be managing our money in a completely different investment landscape.

The wealth transfers will be historic.

People who are wealthy today could be penniless when this decade ends. While those who position themselves correctly right now could build massive wealth.

The great restructuring of the stock market is already happening:

Reliable, household-name companies that fund managers have loved for years are getting crushed in 2026:

Intuit: -57%

Boston Scientific: -49%

Tractor Supply: -40%

Meanwhile, a surge of dynamic companies positioned for this new world are exploding higher:

Sandisk: +573%

Rackspace: +444%

Atomera: +262%

This isn't random market volatility. This is the beginning of an irreversible economic division that's just getting underway.

Names that have seemed untouchable throughout history. Names that every "expert" tells you to buy and hold forever. Names that could rob you of your hard-earned savings if you don't act soon.

But I didn't reach out to you today to spread doom and gloom. I wrote because there's a way to protect yourself and potentially profit from what's coming.

It starts with understanding which companies are on the brink right now... and which are positioned to thrive in The Age of Chaos.

More importantly, I'll share the names and tickers of the companies you can upgrade to that could multiply your money in the coming months. Companies that aren't just surviving this transformation but driving it.

For instance, while everyone's focused on whether Tesla will get a much-needed lifeline from Space X, I've identified a little-known company that was just tapped as Nvidia's self-driving partner, already putting them miles ahead of Tesla in the autonomous driving race. (Get the ticker FREE here.)

I've also got details on what could be the biggest megadeal in the AI space this year – a potential rupturing of the company referred to as "the unseen winner of the AI race." This company could soon split up into three of the hottest new AI stocks of 2026. If it does, all you have to do to automatically get shares in all of them isbuy this stock NOW. It's a once-in-a-blue-moon opportunity you do not want to let pass you by.

I'm giving away all of this analysis completely free in this broadcast. No membership required. No credit card. Just the unvarnished truth about what I see coming and how to position yourself for it.

The Age of Chaos isn't something that might happen. It's already underway.

Knowing the names and tickers of these stocks could mean the difference between winning and losing in the months ahead.

Bullish on Netflix (NFLX) Stock? Here’s Why It’s Time to Pump the Brakes

Posted On Jun 29, 2026 by Joshua Enomoto

Among the most anticipated earnings disclosures next month will come from streaming giant Netflix (NASDAQ: NFLX). Since the beginning of the year, NFLX stock has lost more than 24% of market value. In the past 52 weeks, shares are down more than 44%. At some point, you’d figure that a turnaround is coming — and the catalyst could come from its second-quarter report.

Table of Contents

Scheduled for release on July 16, analysts are looking for earnings per share to hit 79 cents on revenue of $12.58 billion. Investors are nervous, though, because circumstances have been shaky, thus contributing to the fallout in NFLX stock. For example, the most recent Q1 report wasn’t all that great, with the streaming service slightly missing against the bottom line while barely beating on the top line.

Fundamentally, stakeholders have been dumping NFLX stock due to concerns in leadership. Historically, Netflix has preferred to grow its business from within. Recently, though, management has been eyeballing what many experts view as unnecessary and costly acquisitions. Effectively, it sends a poor message about how the company views its future growth potential.

Still, there’s a common thought process that a security like NFLX stock has simply dropped too much. After all, we’re talking about one of the most popular services available in the digital ecosystem. People really don’t go out to the movies with as much fervor as they used to; now, it’s all about streaming your favorite content on Netflix.

Given this fundamental anchor, it stands to reason that shares could potentially rerate higher — basically due to the mean-reversion concept. If so, Netflix stock looks like a wildly enticing discount. Currently, its forward price-earnings ratio is only 22x. Last year, the multiple stood at almost 54x.

So, a great company at a great price — it’s time to buy, right? While anything can happen for the Q2 report, for right now, I’d consider pushing the pause button on Netflix stock.

This piece of knowledge goes for any security, not just NFLX stock: a cheap multiple (compared to a prior level) doesn’t necessarily signal a discount. If this were a universal rule, everybody would simply buy red-ink-stained securities. Obviously, it doesn’t work that way.

When it comes to Netflix specifically, the new, lower multiple could be a reflection of growth moderation. At 54x, you’re basically pricing NFXL stock as a hypergrowth tech disruptor. Unfortunately, recent financial results — along with management’s acquisitive hunger — suggest that the underlying paradigm has matured. Therefore, this situation could be the market simply de-rating the stock to account for its new baseline.

Investors must also consider the structural regime shift in content costs. At its peak multiple, Netflix ranked as the undisputed aggregator of global content. Increasingly, however, the competitive landscape has required a different playbook. As such, Netflix had to pivot heavily into live sports and entertainment programming.

This pivot, while it kept the streaming giant relevant, has resulted in a spike in capital intensity. Namely, live sports rights require enormous up-front, non-negotiable cash outlays. Further, while sports attract massive ad-tier eyes, they carry heavy content amortization costs that can depress future cash flow margins.

Put differently, the market isn’t stupid. It recognizes that the long-term capital intensity of the business has structurally shifted. Subsequently, sophisticated investors are scaling back the multiple of NFLX stock that they are willing to pay for those cash flows.

Besides, it’s difficult to declare that the market is “wrong” about Netflix stock and that it deserves a higher multiple. That’s the type of argument you would expect from a less-sophisticated analysis. However, the onus would be on the expert making the claim to identify what portion of the positive news has not been baked into the share price.

As far as we know, the price is the price. Unless there is compelling evidence to suggest that the market has failed to account for critical datapoints that would impact NFLX stock, we should take the price at face value.

Inferring the Next Steps for Netflix Stock

Those who are still contrarian and bullish on Netflix stock will likely point to the technical damage already incurred. Philosophically speaking, it’s assumed that future bad news will need to be sufficiently repugnant to make an already terrible stock lose even more value. However, with the bears potentially exhausted, it may only take a small bit of good news to move shares positively.

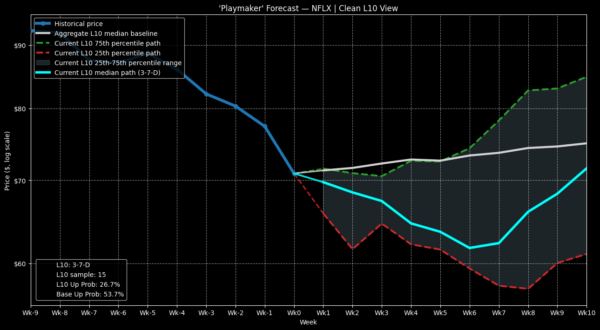

I think most of us believe in this mean-reversion concept. The difference today is that with current technology, we can measure this concept.

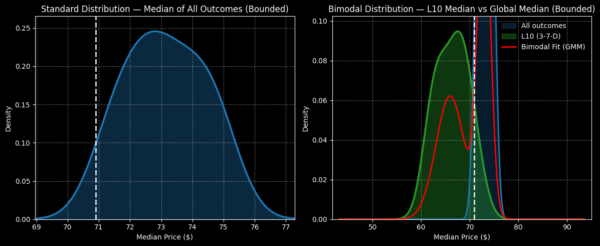

If you were to buy NFLX stock at its current price of $70.90 and hold it for a 10-week period, you would expect a range between $69 and $77, with peak probability density reaching around $72.90 (indicative of a positive bias). This is our random baseline and any signal that we trade off of must beat this baseline to make sense.

Over the last 10 weeks, NFLX stock printed only three up weeks, leading to an overall downward slope. If we condition the forward 10-week performance of NFLX on this 3-7-D signal, the expected forward distribution actually worsens to between $56 and $77. So, from a median 10-week perspective, it’s not worth taking a risk if you’re bullish.

Indeed, when you consider the week-to-week inference of NFLX stock following the 3-7-D signal flashing, it has historically demonstrated weakness for the next six weeks until popping higher. So, if anything, I would be near-term bearish on Netflix stock prior to the Q2 earnings disclosure.

If you want to follow the inference, you may consider the 69/68 bear put spread expiring July 10. Based on probabilistically conditioned data, there’s an observed tendency for NFLX stock to drop to around $68 over the next two weeks. The net debit of this spread is only $32, which may appeal to those speculators on a budget.

However, I wouldn’t expose myself to the bearish trade when it comes to the Q2 earnings disclosure. You just really don’t know what’s going to happen — and personally, I don’t want the smoke. That said, the historical data shows that NFLX stock may still give up some value prior to the Q2 report.

Tidak ada komentar:

Posting Komentar