January 14, 2025

The Answer to a New Tax Question in 2025

Dear Subscriber,

Editor’s note: You might already be putting together your 2024 taxes. If so, you might be asking a question you never had to before: What do I do about crypto?

With the launch of Bitcoin and Ethereum ETFs in 2024, likely millions of traditional investors are figuring out how to report any gains from crypto for the first time in history.

If that’s you, you’ll want to read this. And even if it’s not you, you’ll still want to read this. Many of what our Crypto Managing Editor Beth Canova has here can be applied beyond to the likes of crypto — precious metals, collectables, real estate and even stocks.

Read on …

|

| By Beth Canova |

Like stocks, crypto is treated as property by the IRS, not currency.

The main difference is that you can use crypto directly to make purchases and trade them one for another.

You can also stake cryptos to earn additional yield, and you can “mine” new crypto instead of buying them.

You can’t do any of that with stocks. And so, with stocks, you are only taxed when you sell and realize gains.

In other words, certain activities involving cryptos trigger taxable events.

Learning about these events now will make filing simpler come tax season.

So, here are five of the more common taxable events you’ll likely encounter.

Taxable Event No. 1:

Receiving Crypto as Payment

Simply purchasing a crypto isn't a taxable event. Neither is holding it. That’s true for just about everything — gold, real estate, etc.

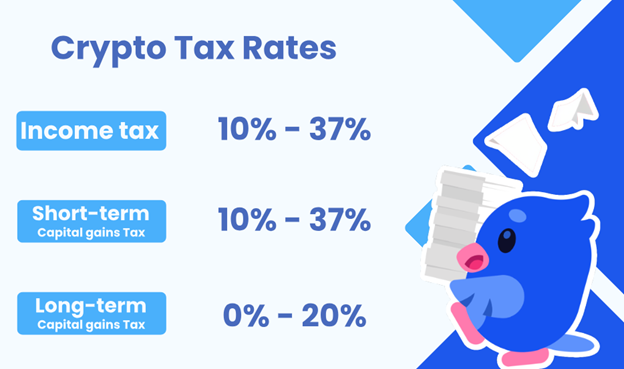

However, if someone pays you in crypto, it’s treated as income. Therefore, it’s subject to income tax.

Crypto is taxed based on your income tax bracket, the same as any other income.

Exactly how much you'll pay depends on the fair market value of the crypto at the time of the transaction.

Independent contractors and freelancers are subject to paying self-employment tax on crypto received as payment.

Meanwhile, businesses need to pay business income tax on profits earned by accepting crypto as payment.

Taxable Event No. 2:

Selling Crypto

For most crypto investors, the most important consideration is the capital gains tax you incur when you sell your crypto for a profit.

If the sale price is higher than its original purchase price, that is considered a capital gain.

You’ll need to report this gain and give a portion of your earnings to the U.S. government based on your income tax bracket.

To calculate capital gains tax, we first need to understand the cost basis, or the price you paid to purchase the asset.

In the case of crypto, that would be the spot price plus any fees paid during the process.

Let's say you buy $1,000 of Ethereum (ETH) and pay $30 in fees to do so. Your cost basis would be $1,030. That’s the sum of the cost of the purchase plus the purchase fees.

To figure out the capital gains tax, you’ll need to go a step further and calculate the sale price minus any fees paid in the sale. In short …

- Cost basis = Purchase Price + Purchase Fees

- Capital Gain = (Sale Price — Sale Fees) — Cost Basis

So, if you sell that ETH for $2,000 and pay $50 in sales fees, your proceeds are $1,950.

Now that you have these two numbers, you can subtract them to get your taxable capital gain.

Take the $1,950 in proceeds and subtract the $1,030 cost basis and you get $920. That is your taxable capital gain.

Now that you know what's being taxed, the final step is to figure out the rate that taxable capital gain will be subject to.

That’s based on whether it's a short-term or long-term capital gain.

Short-term applies to any assets bought and sold within a year. As of the 2024 tax year, a short-term capital gain is taxed between 10% and 37%, based on your income.

Long-term applies to assets held for more than a year. As of 2024, those gains are taxed between 0% and 20%, based on your income.

As you can see, long-term capital gains are subject to a lower tax rate — even in the highest income bracket — than short-term ones.

So, if you don't have any need to sell before the one-year mark, you should avoid doing so.

Instead, allow it to convert into a long-term capital gain to lower your tax burden in the process.

Now, not every crypto went up this year. Or perhaps not while you were in the trade. But that’s not necessarily a bad thing.

If you lost money in the sale, you won't be required to pay any taxes on that transaction.

Accurately reporting capital losses isn't just required, it's also beneficial to investors. Capital losses offset the tax burden of capital gains in a given year.

For example, if you made $5,000 in capital gains this year, you'll be taxed on that $5,000. But if you had a capital loss of $1,000 and reported it, it would lower your capital gains to $4,000.

That lowers your taxable amount and thus saves you money. Again, this applies to many assets beyond crypto.

Taxable Event No. 3:

Paying with Crypto or Swapping It

Buying things with crypto can trigger a taxable event.

In the eyes of the IRS, when you buy something with a crypto, you are essentially converting it from an investment asset into regular money.

This triggers a taxable event.

So, if you use Bitcoin (BTC) to buy a car, and the value of that BTC is higher than when you initially invested, the IRS considers that a realized capital gain.

Meaning, you’ll need to declare the sale and pay taxes on it.

The same goes for exchanging one crypto for another.

Again, as far as the IRS is concerned, you can't just trade one crypto for another, as that’s impossible with stocks.

To anyone involved in crypto, swapping is as simple as converting BTC into ETH.

But to the IRS, it’s as if you are swapping your BTC into U.S. dollars, and then buying ETH.

And if the value of your BTC when swapping is higher than when you purchased, you’ve technically realized a capital gain.

That’s why any gains or losses will need to be filed and will be taxed accordingly.

Taxable Event No. 4:

Mining and Staking

Crypto earned through mining or staking is treated just like income earned through stock dividends.

In other words, they're both subject to income tax.

- Mining is the process of solving complex algorithms to validate transactions and create new cryptos.

- Staking is a way to provide liquidity to a communal pool. In return, the network or platform gives you rewards, usually in the form of its native token.

Any rewards from mining or staking should be recorded and declared as regular income based on its fiat value on the day you received it.

If mining is a part of your business, you should declare the fruits of your labor as business income.

This way, you can deduct mining expenses — such as electricity, home office deductions, hardware and other expenses vital to your business — on your taxes.

Taxable Event No. 5:

Inheriting Crypto

Maybe you received a crypto inheritance this past year. Or you could consider leaving your holdings for your children.

Either way, you should be aware of the tax implications.

Crypto passed down from generation to generation may be subject to estate tax and capital gains tax.

The federal estate tax is only relevant if the total value of the estate is $13.99 million or more for individuals and $27.98 million or more for married couples.

If, under these rules, you are required to pay an estate tax, any crypto in the estate must be included.

The federal tax rate for an estate can range from 18% to 40% based on the exact size of the total estate.

In addition, there are 12 states and the District of Columbia that have additional estate taxes. Six more states have inheritance taxes.

Luckily for crypto heirs, upon the passing of the original owner, a step-up in basis occurs. This lowers the inheritor’s tax duties on the crypto.

A step-up in basis means that the new cost basis will be calculated based on the fair market value of the crypto at the date of the previous owner’s death. Not its original purchase date.

Assuming the asset has appreciated since its purchase, this gives the heir a higher cost basis and thus a lower capital gains tax.

What About Crypto ETFs?

Here’s the good news, since you technically could not have held a Bitcoin ETF for longer than a year (since they didn’t launch until January 2024), it’s easy. Any gains you took in the 2024 tax year would be short-term capital gains.

But really, the answer going forward will be the same. As long as you aren’t mining, accepting crypto as payment or the handful of other taxable events above, any gains will be treated the same as other assets.

Hold longer than a year? Pay long-term capital gain taxes.

Hold for less? Pay short-term capital gain taxes.

So, if this is the first time you have some extra gains from this alternative asset class, you don’t need to worry. If you know how to pay taxes on other assets, you got this, too.

But as always, we recommend you speak with a tax professional.

Best,

Beth Canova

P.S. In just a few hours, a brand-new event describing how to collect “Supersized Crypto Royalties” will go live. We don’t want you to miss it. To grab your spot, click here right away.

Tidak ada komentar:

Posting Komentar