You're reading The Budget Analyst — a calm space in the noise of markets.

Here we collect signals, patterns, and quiet insights that help you see the bigger picture.

No rush, no hype — just clarity for your financial journey. | | | | In partnership with ALTIMETRY RESEARCH |

|

|

|

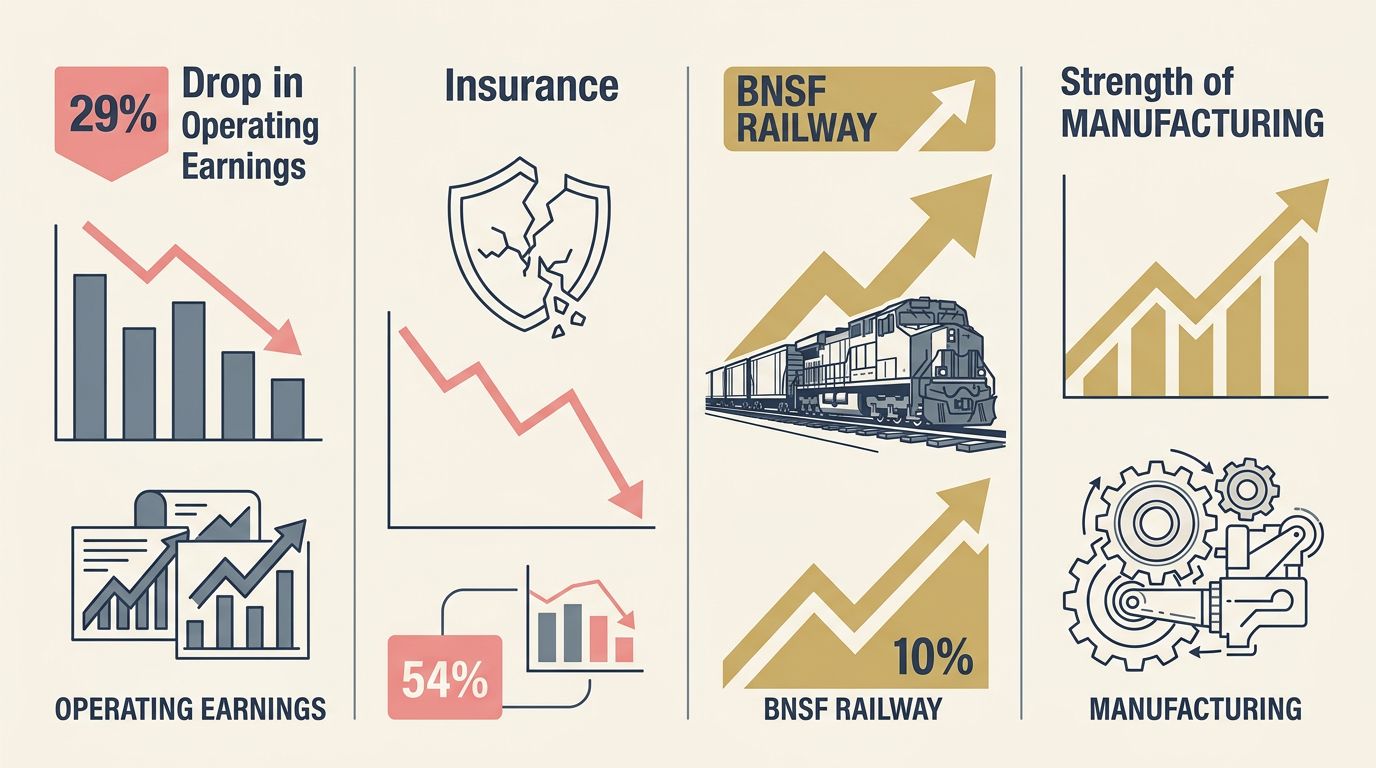

| | | | | There is a particular kind of quiet that settles over a room when the person everyone came to hear stops talking. | That is the feeling inside Berkshire Hathaway right now. On December 31, 2025, Warren Buffett stepped down as CEO after nearly sixty years—handing the controls to Greg Abel, a man who has run Berkshire's non-insurance businesses for years but has never once written a shareholder letter. On February 28, 2026, Abel posted his first. No aphorisms. No Midwestern parables. Just business. | The fourth quarter operating earnings came in at $10.2 billion, down 29% from a year earlier. Insurance profits fell 54%. Write-downs on Kraft Heinz and Occidental Petroleum dragged results further. And yet the company ended the year sitting on $373 billion in cash—a record—after thirteen consecutive quarters of selling more stock than it bought. | This is not a crisis story. It is a regime change, and the signals are structural. |

| |

| | |

| | | | | The Engine Room: Why a 29% Drop Is Not What It Seems | You hear a number like "29% decline" and the instinct is alarm. That instinct, in this case, is wrong. Operating earnings measure the health of Berkshire's actual businesses—the railroads, the retailers, the insurance underwriters—not the fluctuations of its stock portfolio. The engine room took a hit, but the hull is intact. | The insurance segment tells most of the story. Underwriting results softened significantly in late 2025, driven by higher claims and lower premiums in a competitive cycle. GEICO and Berkshire's reinsurance arms saw margins compress. Add a $4.5 billion impairment tied to Kraft Heinz and Occidental Petroleum, and you have a quarter that looks far worse than the underlying machine warrants. | Here is where the first signal emerges. BNSF Railway and Berkshire's manufacturing operations actually delivered margin and cash flow improvements during the same period. The energy segment held steady. The weakness was concentrated, not systemic—a distinction that matters enormously when you are evaluating a conglomerate with over sixty operating subsidiaries. | Buffett himself embedded a warning in Berkshire's reports for years: focusing on any single quarter's results can be "extremely misleading." His compounded annual gain from 1965 to 2025 was 19.9%, nearly doubling the S&P 500's 10.4% over the same window. One soft insurance quarter does not rewrite six decades of compounding. But it does create a convenient narrative for those who want to declare the magic gone. | The magic was never magic. It was plumbing—disciplined, boring, relentless capital allocation. And plumbing does not retire when the plumber does. | | The Cash Fortress: $373 Billion and the Art of Saying No | There is a pattern that repeats in Berkshire's history with the regularity of a metronome. Before the dot-com bust in 2000, Berkshire sat on an outsized cash position. Before the global financial crisis in 2007, the same. And now, in early 2026, the company holds $373 billion—more than the GDP of most nations—while refusing to buy back its own stock for six consecutive quarters. | Abel addressed this directly in his first letter, insisting the cash hoard is "not a sign of an investment retreat" but rather disciplined patience in a market where the S&P 500's CAPE ratio averaged 39.8 in February—a valuation not seen since the dot-com peak. Berkshire sold a net $187 billion in stock over the last thirteen quarters. That is not portfolio trimming. That is a fortress being built in plain sight. | The institutional signal here is unmistakable. When the most successful capital allocator in modern history spends his final years converting equities to cash—selling 75% of his Apple stake, dumping 50.8 million shares of Bank of America—and his handpicked successor continues the posture, you are not watching indecision. You are watching preparation. | What Berkshire is preparing for remains the open question. A deep recession, a market correction, or simply a world where asset prices have outrun fundamentals for too long. The cash is not idle. It is ammunition, sitting quietly in the magazine, waiting for the moment when prices finally meet rationality. | | | Let me ask you... | Why did Buffett step down as the CEO of Berkshire Hathaway now? | You might have your own theory... | But a private research group with links to the FBI might make you think twice. | You see, Buffett didn't step down in 2008, when the banks collapsed (though he was already 78 years old by that point). | And he didn't retire in 2020, when the pandemic brought chaos to the markets (again, he was 23 years past retirement age by then). | No… | He's chosen 2026 as the time to finally hand over the reins. | How come? | Well, after analyzing over 3,000 stocks and 40,000 data points, our institutional research — which all of the top ten money managers in the world pay thousands to access — suggests the real reason the Berkshire CEO stepped away is because of a shockwave that is about to pulse through the market. | Make no mistake... | Massive gains—and huge losses—are coming in the next six months. | And it seems like Buffett knew. | | ...and learn about the one specific stock you should consider buying because of what's about to happen. | By the way, it won't cost you a cent to find out which stock it is—it's all revealed (including the ticker) in this presentation. |

| |

| | |

| | | | | The Abel Regime: Continuity Wrapped in a Different Temperament | Greg Abel's first shareholder letter landed with the weight of expectation and the texture of restraint. The New York Times described it as "straight commentary"—no folksy wisdom, no cherry-picked anecdotes from a Nebraska childhood. Just operational clarity. That shift in tone is itself a signal worth reading carefully. | Abel comes from the operational spine of Berkshire. He ran Berkshire Hathaway Energy and oversaw the non-insurance subsidiaries—the railroads, the utilities, the manufacturing lines. His background suggests comfort with large industrial transactions, energy infrastructure, and capacity expansion. This is an operator, not an oracle. The character of capital deployment may change even if the philosophy does not. | One detail that deserves more attention: Buffett is not gone. He remains chairman, reportedly in the office five days a week, still consulted on insurance underwriting and equity investments. Abel and Buffett speak daily, according to multiple reports. This is not a clean break—it is a layered handoff, designed to reduce transition risk while the "Buffett premium" slowly converts into an "Abel track record." | Berkshire shares have lagged the S&P 500 by more than 27 percentage points since Buffett announced his departure in May 2025. The stock dipped another 5% after the Q4 earnings release. That gap represents the market's uncertainty about whether Berkshire's advantages are personal or institutional. The answer, quietly, is mostly institutional—the $160 billion insurance float, the decentralized operating model, and the culture of rational restraint exist independently of any single mind. | The Real Question: Personal Magic or Institutional Architecture? | Here is the mental model that matters. Berkshire Hathaway is not a hedge fund that happened to buy railroads. It is an infrastructure—a network of moat-protected businesses generating cash that flows upward to be redeployed by a disciplined allocator. The allocator has changed. The architecture has not. | The insurance float mechanism still generates $160 billion in investable capital at effectively zero cost. The subsidiaries—from BNSF to See's Candies to Precision Castparts—still operate with minimal interference from Omaha. The fortress balance sheet, as Abel emphasized, remains "never compromised." These are structural advantages, not personality traits. They do not fade when a 95-year-old steps out of the corner office. | What does fade is the market's willingness to grant patience. Buffett earned decades of trust by compounding at 19.9% annually. Abel inherits the machine but not the goodwill. Every soft quarter will be scrutinized more harshly. Every large acquisition will be measured against Buffett's legendary restraint. The margin for error is thinner, even if the underlying business is no weaker. | The convergence of a record cash position, a historically expensive market, and a leadership transition is not coincidence. It is architecture. Buffett spent his final years arranging the pieces so his successor would have maximum optionality and minimum obligation. The $373 billion is not a warning—it is a gift, handed over in a hushed room, with the quiet instruction to wait for the right moment. | For executives, builders, and investors watching from the outside, the practical takeaway is this: watch what Berkshire does with the cash over the next twelve months, not what the market does with Berkshire's stock price. The plumbing will tell you everything the headlines cannot. |

| |

| | |

|

|

Tidak ada komentar:

Posting Komentar