Prices already rebounded 56% in H2 2025, climbing from $10,800/mt to $16,900/mt by December.

The price crash did real damage to future supply.

- Arcadium Lithium and Core Lithium shut down mines in Australia.

- Albemarle paused its global growth plan.

In August 2025, CATL halted its Jianxiawo mine in Jiangxi province after a permit expired.

That single site held 3-6% of global lithium supply. And when the news broke, Albemarle jumped 17%, Pilbara 16%, and lithium futures hit the daily limit on the Guangzhou exchange.

The pipeline got gutted during the exact window when future demand was compounding.

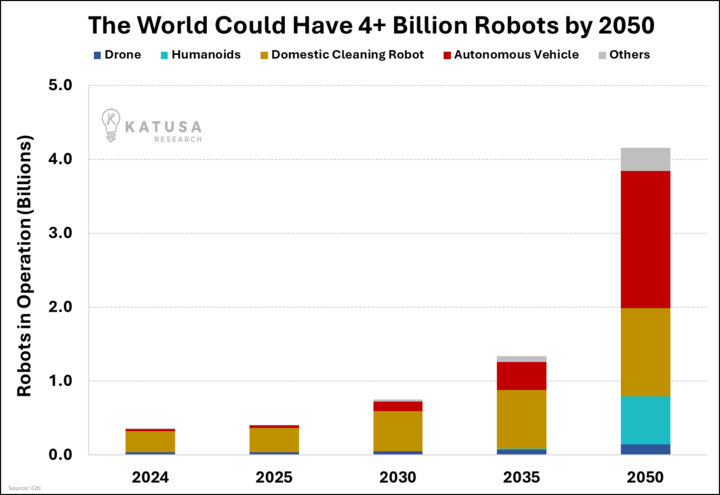

- Citi projects that 1.3 billion AI robots will be operational by 2035, increasing to 4 billion by 2050.

Re-read that.

Scaling to Musk's 10-billion-unit projection and Adamas Intelligence says you'd need 10 times current global lithium production just for robots.

The IEA projects lithium demand from clean energy will grow 5x by 2040. That model was built before robots entered the picture.

Every bump in robot forecasts is a bump in lithium demand that most supply models haven't priced in.

85% Of Refining Runs Through One Country

China controls roughly 85% of global rare earth refining and 40-50% of copper smelting.

When MP Materials, the only active rare earth miner in the U.S., stopped shipping raw ore to China last year, NdPr oxide prices jumped 40% in weeks.

One company's supply shift moved a global market. Now, western governments are spending to close the gap.

The DOE put $1 billion toward rare earth supply chains. MP Materials is expanding Mountain Pass in California.

The EU passed its Critical Raw Materials Act. But Mountain Pass has been "expanding" since 2022, and the average new mine takes 18 years to reach output.

Policy and physical production run on very different clocks.

Three Metals, One Math Problem

Neodymium is up 113% in a year.

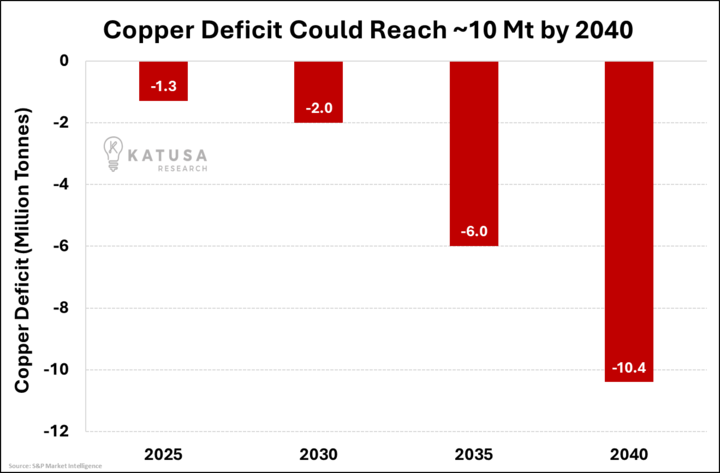

Copper is at all-time highs with a 10-million-ton projected deficit.

Lithium's surplus is evaporating just as a new demand source enters the picture that most supply models haven't accounted for.

- These three supply gaps share the same root cause: demand from robots, EVs, grid storage, wind, defense, and AI is scaling all at once.

The mines needed to feed that demand were never built when they should have been.

The companies on the right side of these gaps — with permits in hand, production growing, and costs locked below spot…

Are the ones we've been building positions in for the past two years inside Katusa's Resource Opportunities.

Each one was picked using Katusa's framework for telling which miners actually gain from supply crunches and which ones just talk about them.

See What's in the Portfolio →

Regards,

Marin Katusa

Tidak ada komentar:

Posting Komentar