If You Keep Cash In A U.S. Bank Account… Read This NOW (From Banyan Hill Publishing)

Key Takeaways

- Ulta Beauty is on track to rally higher in 2025 and 2026 because of its growth, operational quality, and market share gains.

- Analysts' trends are positive, supporting a sustained rally in this stock.

- Institutional investors are accumulating Ulta and providing a solid support base and tailwind for price action.

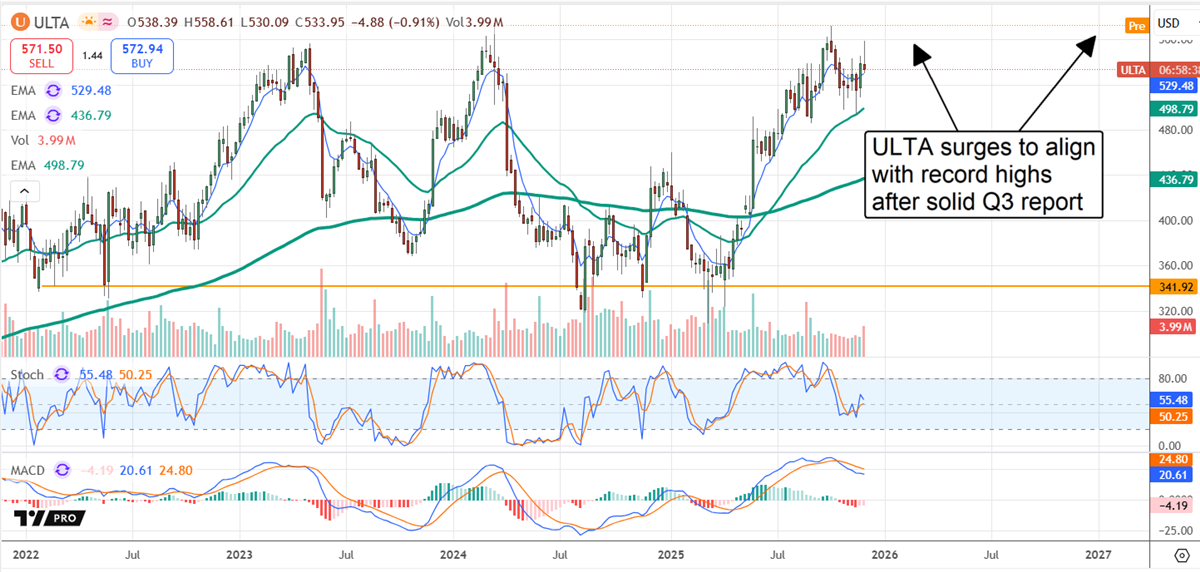

Ulta's (NASDAQ: ULTA) fiscal Q3 earnings report proves that its appeal is more than skin deep. The rally, which began in April 2025, is no short-term phenomenon. It is on track to reach new highs in 2025 due to its growth and operational quality, and is likely to continue rallying in 2026.

Among the critical takeaways from the release is the analysts' bullish response to the news. They view the results as not only strong but also the guidance as potentially cautious, setting up a catalyst for early in 2026.

Between then and now, the price-target revision trend has been supporting the action and pushing this market to new highs. While the consensus aligned with the market ahead of the release, trends, including post-release activity, suggest a price range of $650, which is sufficient for a nearly 20% upside expected to be reached within the next few quarters.

Many have already secured their free Bitcoin reward offered by our esteemed guest. How about you?

In an effort to spread the word about our upcoming workshop, he's generously offering $10 in Bitcoin (BTC) to participants.

Absolutely no strings attached.

Secure Your Spot Now

Ulta Has Beautiful Quarter, Issues Robust Guidance With Cautious Tone

Ulta had a strong quarter, given the macroeconomic headwinds and analysts' forecasts. The company's $2.9 billion in net revenue grew by 12.9% year-over-year (YOY), outpacing MarketBeat's reported consensus by nearly 750 basis points. Strength was driven by comp-store sales, an increase in store count, and acquisitions, all of which are expected to drive growth in the current and subsequent quarters.

Comps increased by an impressive 6.3%, driven by a 3.8% traffic increase and a 2.4% improvement in transaction size. The data indicate that Ulta's customers not only visit the store more frequently but also spend a greater portion of their beauty and skin-care dollars there as the company gains market share.

The margin news is also impressive. The company widened its gross margin and controlled operating costs, resulting in solid bottom-line outperformance. Gross margin increased by 70 basis points due to lower costs, while operating margin decreased because of higher selling, general, and administrative expenses related to wages, incentives, and store-level expenses that are driving the revenue in.

Salaries and incentives are here to stay, but store remodeling won't be, creating an opportunity to improve margins in the upcoming fiscal periods. The bottom line for Q3 is that earnings of $5.14 are flat compared to the prior year but more than 1170 basis points better than expected.

Ulta's Debt Increase Not a Worry for Investors, Capital Return Is Safe

The worst news coming out of Ulta's Q3 report is an unexpected increase in short-term debt. The company leaned on its revolving credit facility for working capital, significantly increasing its debt, but ultimately did no damage to itself or its outlook.

The net result is that cash remains healthy at roughly 0.5x debt, while increases in receivables, inventory, and prepaid expenses offset the debt. Regarding leverage and equity, the company's total liabilities are approximately 2.2x its equity; there is virtually no long-term debt beyond lease liabilities, and equity is increasing, up 9% YOY.

Ulta's capital return is attractive, underpinning the long-term stock price outlook. The company doesn't pay dividends; instead, it aggressively buys back shares. The FQ3 and YTD activity resulted in a 4.66% average quarterly and a 5.36% year-to-date decline in share count, and the pace is likely to continue over the next year. The company has $2 billion left under the current authorization, sufficient for more than two years at the FQ3 pace.

A Millionaire With SEVEN Clicks?

$1,000 in just seven stocks in 2004 could have turned into a million-dollar portfolio today…

Back then… one financial expert begged people to look at Nvidia -- when it was trading at just $1.10!

Now… he's urging you to look at a new group of seven stocks…

Check this Out (The NEXT Magnificent Seven)

Ulta's New High Is Imminent: 20% Gains Could Be Seen by Year's End

The post-release action put ULTA stock in line with record-high levels, positioning it on track to set new highs in the opening session.

Assuming the market follows through on the signal, those highs are likely to be followed by a rally that could take this market up by 18% to 20% from the critical resistance point within a few weeks.

The risk is that gains will be capped at the existing high, keeping Ulta range-bound, but that seems unlikely, given the results, outlook, and institutional activity.

The institutions own more than 90% of this stock and are accumulating in Q4 2025.

Read this article online ›

Tidak ada komentar:

Posting Komentar