In partnership with |  |

|

|

5 Investment Ideas - November 2025 |

Welcome to the November edition of Investment Ideas. |

Each month, I spotlight a select mix of businesses I am following closely. |

As a reminder, this report is concise by design. |

It does not capture every risk in full but highlights the key dynamics shaping each business and why they merit close attention. |

Let's dive in. |

Note: This report is for informational purposes only and is not investment advice. Please see the full disclaimer at the end. |

|

|

The Vault Just Opened on a $2T Market Opportunity |

|

Elf Labs owns 100+ priceless trademarks for icons like Cinderella & Snow White. They've already earned $15M+ in royalties, and are now using AI to turn these legends into living, interactive worlds for the next generation. With patented tech & a $2T market opportunity ahead, the next chapter of entertainment is being written in real time. |

Invest in Elf Labs |

This is a paid advertisement for Elf Lab's Regulation CF offering. Please read the offering circular at https://www.elflabs.com/ |

|

5/ Porsche AG |

Ticker: $DRPRY Market Cap: $46B

|

|

Porsche AG, founded in 1931 and headquartered in Germany, is a global manufacturer of high-performance vehicles. |

The company operates across automotive manufacturing and financial services, including vehicle production, engineering development, parts and accessories, financing and leasing solutions, and certified pre-owned sales through its global dealer network. |

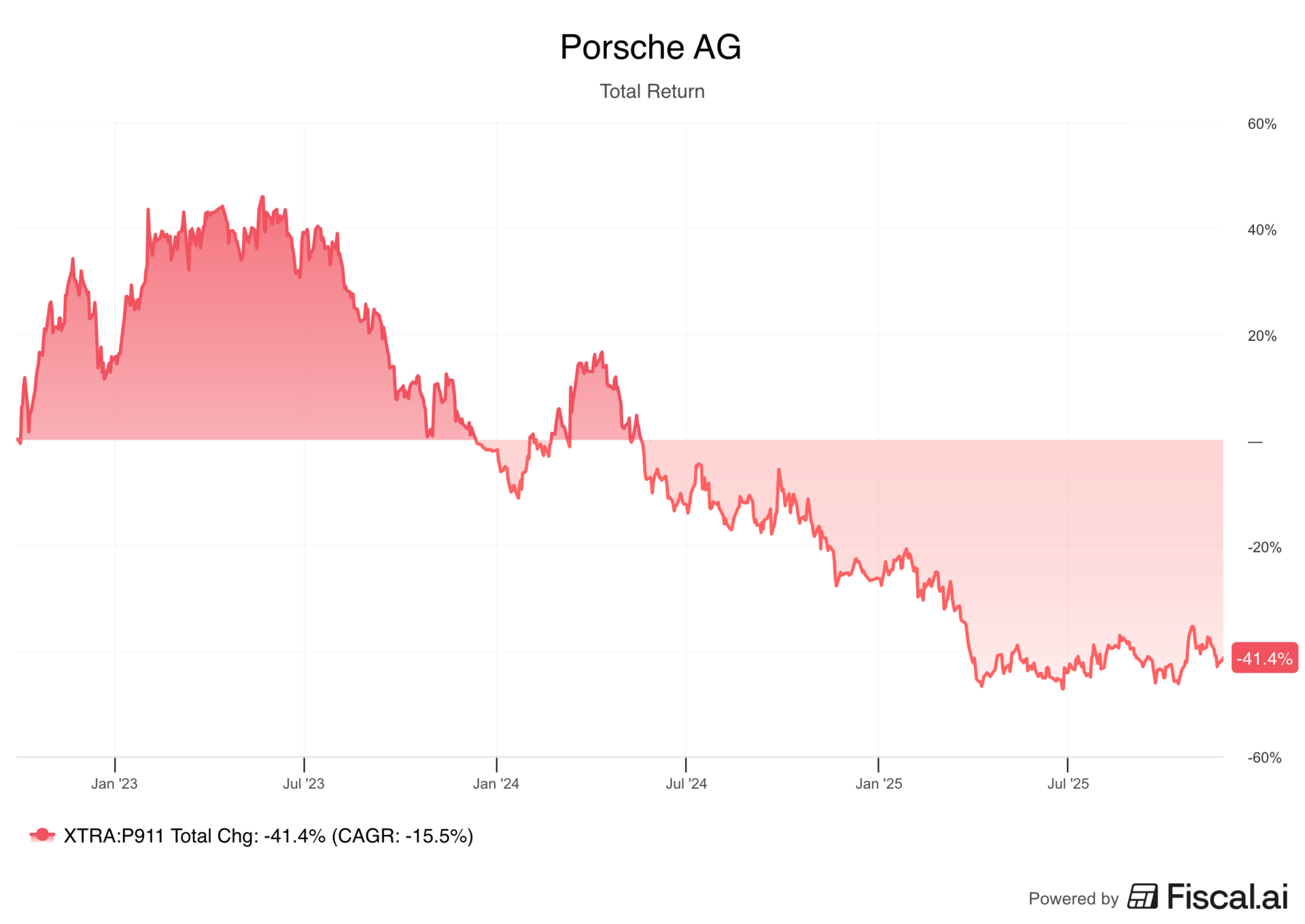

The stock is down 14% in 2025 and has fallen over 50% since its IPO in late 2022. |

Key Metrics: |

|

Outlook (Estimates): |

Forward 2Y Revenue CAGR: -3% Forward 2Y EPS CAGR: -21% Long Term EPS Growth: -11%

|

Recent Developments: |

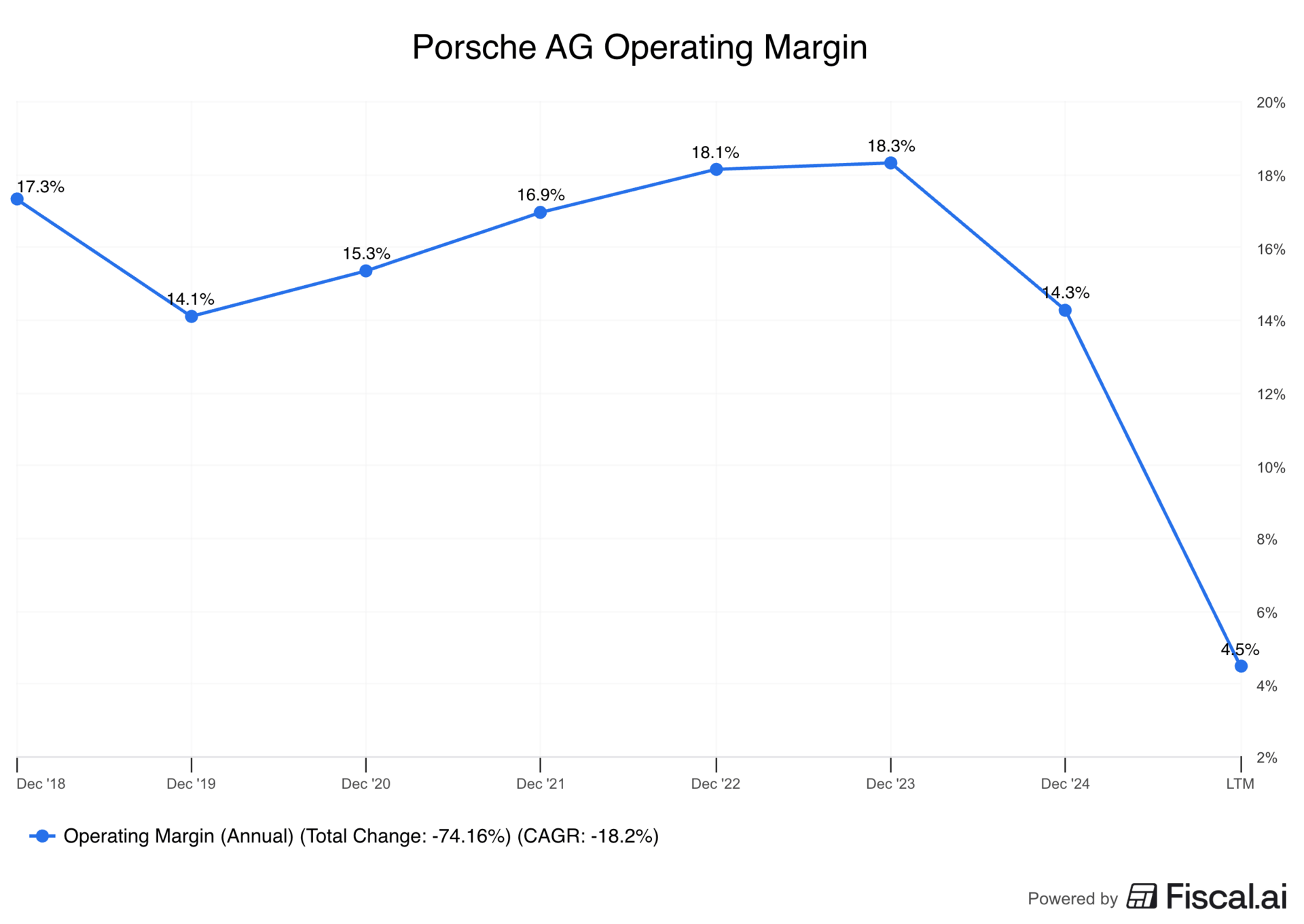

1/ Profitability Under Pressure — Porsche posted its first quarterly loss in Q3, with operating income falling €966M due to a pullback in its EV strategy, elevated tariffs, and weakening demand in China. For the full year, the EV pullback created a €3.1B profit hit, while U.S. tariffs were projected to cost another €700M. EV penetration reached 23% this year, well below the company's prior 50% target, highlighting weaker demand and slower execution than planned. |

2/ Sharp Decline in China — China, one of Porsche's most important markets, saw demand fall sharply. Deliveries dropped from nearly 96,000 vehicles in 2021 to just under 46,000 over the last twelve months, representing a 52% decline. Competition from BYD, Geely, Chery, Xiaomi, and other value-focused brands have intensified. |

3/ Divided Leadership Focus — Volkswagen, the majority owner of Porsche, had its CEO Oliver Blume overseeing both Volkswagen and Porsche simultaneously, which likely divided focus and limited leadership capacity. |

|

Why This Might Be An Opportunity: |

1/ EV Strategy Pivot — Porsche recognized that EV demand was weaker than expected and made a costly pivot that allows it to focus on selling what customers actually want. The company is expanding its lineup of combustion engine and plug-in hybrid models while continuing to invest in electrification, aiming for a more balanced drivetrain mix. |

2/ China Strategy Reset — Porsche is restructuring its China strategy by reducing its planned dealer network from 150 locations to about 80 by 2027. This reflects a more disciplined, profitability-focused approach in a market that has become highly competitive. |

3/ Margin Recovery Efforts — To offset tariff pressure, Porsche is introducing price increases in the U.S. market. Tariffs fell from 27.5% to 15% after a new U.S.–EU trade agreement, and management expects restructuring efforts, operational adjustments, and cost controls to support a return to high single digit profit margins next year. R&D spending is expected to peak this year and next, followed by a decline, and the company is shifting toward partnerships and licensing to improve flexibility and reduce capital intensity. |

4/ New Leadership — Volkswagen's CEO Oliver Blume is stepping down from his role at Porsche, and the company will now have a dedicated CEO in Michael Leiters, the former McLaren Automotive CEO and former Ferrari CTO. This brings more focused leadership during a critical turnaround period. |

5/ Strong Brand Equity — Porsche remains one of the most desirable automotive brands globally, with strong loyalty and broad cultural recognition. Nearly 60% of owners repurchase another Porsche, the brand has over 30M social media followers, and it consistently ranks highly in JD Power awards for quality and sales satisfaction. |

TLDR: Porsche has faced significant challenges from a costly EV reset, weaker China demand, tariff pressure, and diluted leadership focus, all of which drove its first quarterly loss. The company is now repositioning its model mix, restructuring China operations, and working to restore margins under a new dedicated CEO. Its brand strength and product strategy shift provide a solid foundation for recovery, though execution risk and competitive pressure will likely make the turnaround story volatile. |

My Take: Porsche is working through several short-term headwinds, many of which were self-imposed. The opportunity is clear if management can execute as operating margins could meaningfully recover toward historical levels. I have not taken a position yet, as I want to further evaluate competitive pressures in China, which remains an important market and has shifted dramatically over the past few years. However, I'll be following the company closely as the turnaround unfolds. |

|

4/ Celsius |

Ticker: $CELH Market Cap: $11B

|

|

Celsius, founded in 2004 and based in Florida, develops and markets functional energy drinks and liquid supplements globally. |

The company sells a range of carbonated and non-carbonated performance drinks, on-the-go powders, and recovery blends through retailers, convenience channels, gyms, health clubs, and major e-commerce platforms. |

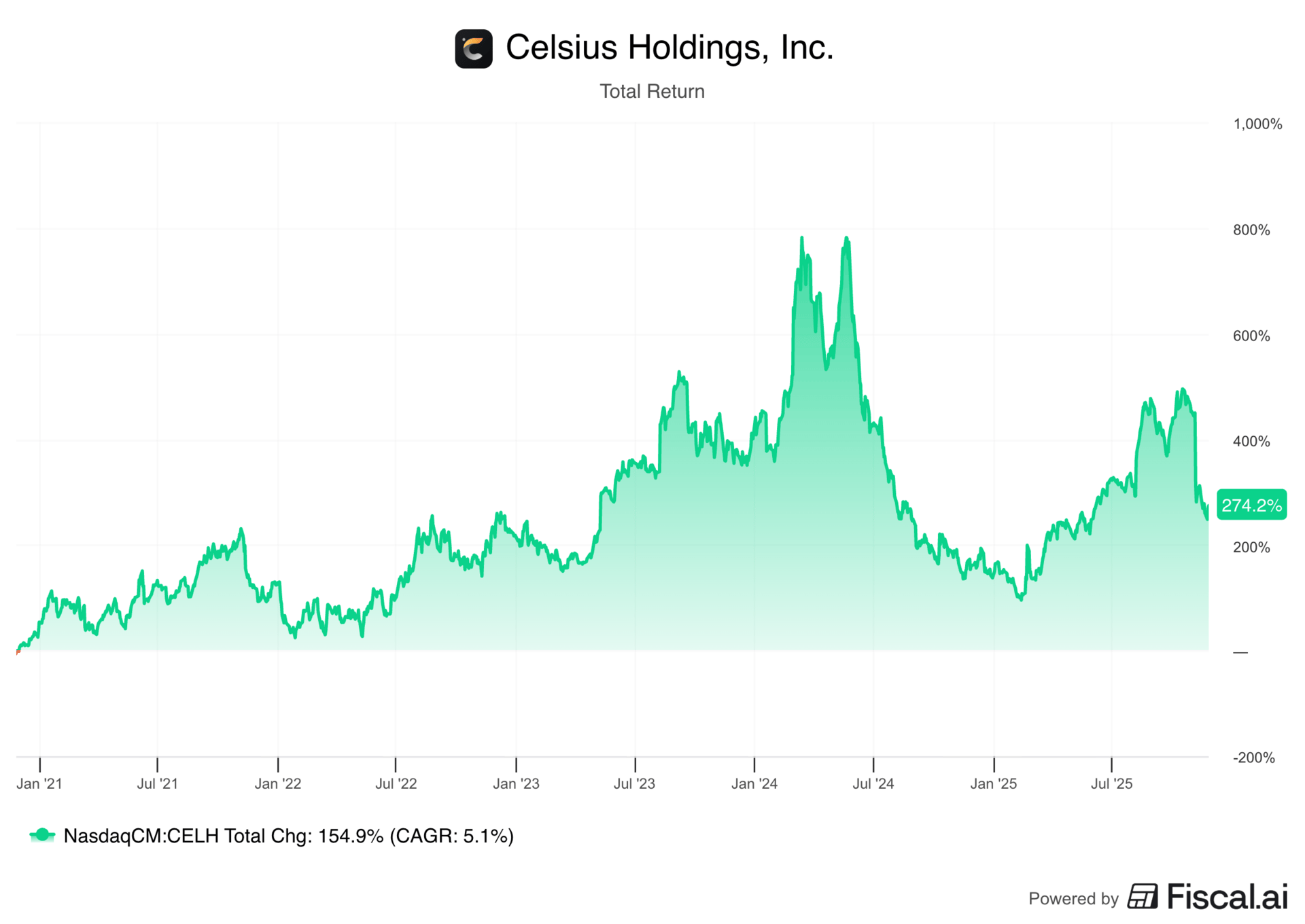

Over the past month, the stock is down roughly 35%, but is still up 50% on the year. |

Key Metrics: |

|

Outlook (Estimates): |

|

Recent Developments: |

1/ Lower Core Brand Demand — In the most recent quarter, Celsius reported 44% revenue growth in its core brand, but retail sales grew only 13%, which is a more accurate gauge of real consumer demand. PepsiCo serves as the exclusive U.S. distributor for Celsius, and is the preferred global distribution partner. The gap reflects PepsiCo increasing its orders this year after cutting them sharply in 2024 to correct an earlier overstocking issue in its warehouses. |

2/ Integration Noise & Margin Pressure — Celsius recorded a $247M one-time charge tied to transitioning Alani Nu (which it acquired in April 2025) into PepsiCo's distribution network, which pushed Q3 to an 11% operating loss. Management expects the next few quarters to remain "noisy" as integration work continues, marketing spend stays elevated, and freight costs remain pressured. Profitability will likely stay constrained until these moving pieces stabilize. |

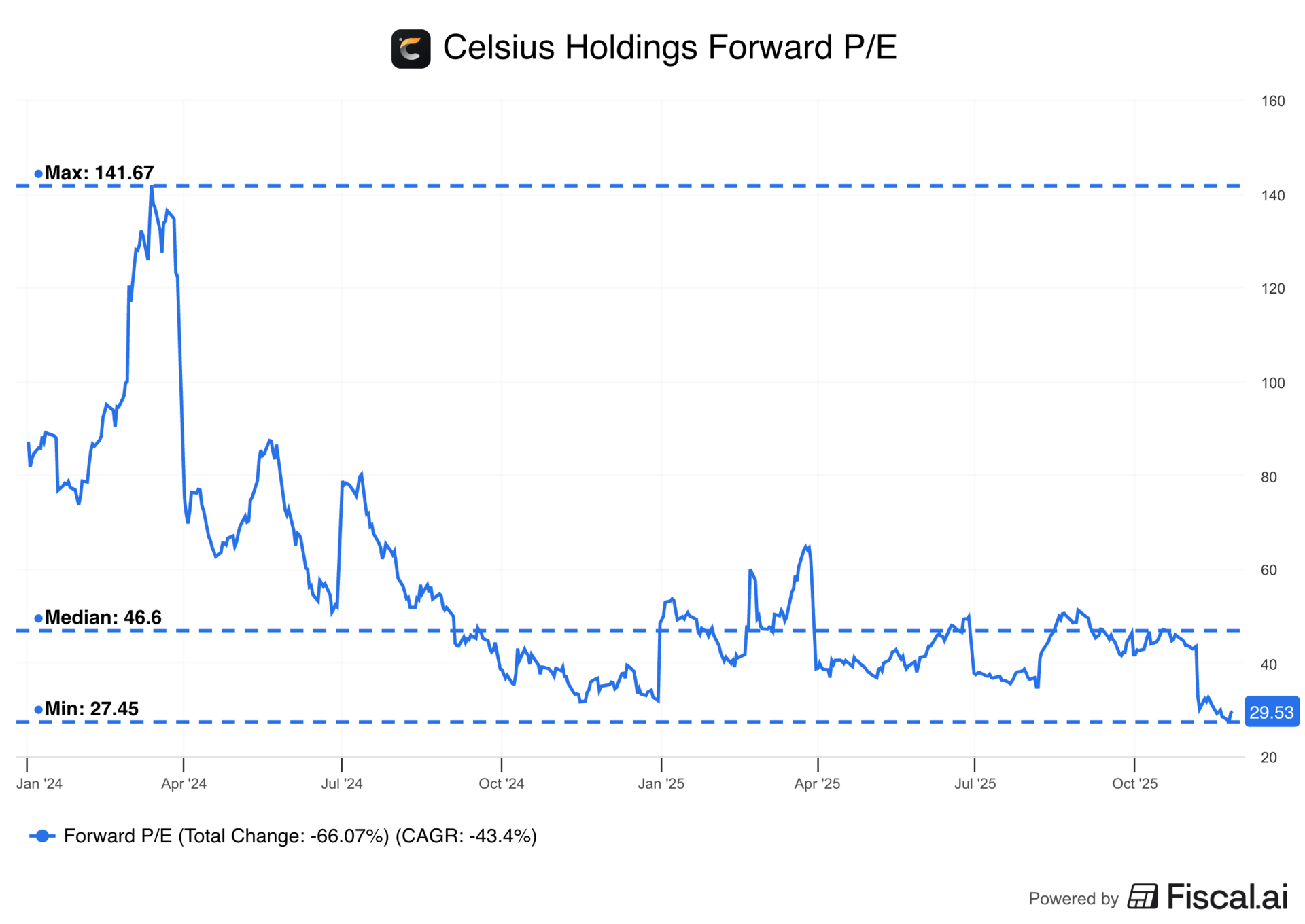

3/ Elevated Valuation Resetting — Before the recent pullback, Celsius stock had surged more than 120% this year and traded at roughly 50x forward earnings and 5x forward sales, which left little room for any blemishes. |

|

Why This Might Be An Opportunity: |

1/ One-Time Costs Covered — The $247M distribution termination charge is fully funded by PepsiCo and does not impact Celsius' cash position. Adjusted earnings beat expectations in Q3, and many of the current gross margin pressures are temporary. Management expects benefits to begin as early as next year and is evaluating pricing actions to offset cost headwinds. |

2/ Rapid Market Share Gains — Celsius has grown its U.S. energy-drink market share from 5% three years ago to 21% today, driven by strong core brand momentum and the additions of Alani Nu (acq. April 2025) and Rockstar Energy (acq. August 2025). In the most recent quarter, the full portfolio grew 31% at U.S. retailers. This positions Celsius as a strong competitor to Monster and Red Bull in a $25B U.S. energy drinks market projected to grow 7.2% annually through 2030. |

3/ More Synergistic Partnership — Celsius acquired the rights to Rockstar Energy in the U.S. and Canada, creating a more streamlined partnership with PepsiCo. Pepsi previously owned Rockstar, which competed directly with Celsius. Consolidating the brands under Celsius allows Pepsi to focus on distribution while Celsius manages and grows the full energy drink portfolio. Rockstar is currently seeing sales decline, but Celsius has room to reposition the brand. Meanwhile, Alani Nu delivered triple-digit growth in Q3, and is joining the PepsiCo distribution system on December 1st, 2025, enabling broader distribution. |

4/ Affordability & Health Tailwind — A Celsius can generally costs under $3, far below the $5 to $10 price tag for specialty drinks at major coffee chains. Combined with its "clean" and functional perception, Celsius is well positioned to benefit as consumers seek more affordable and healthier alternatives. |

5/ Management Signals Confidence — Celsius authorized a $300M share repurchase program on November 10th, signaling confidence in long-term value. Days later, COO Eric Hanson and director Hal Kravitz made the first insider purchases in more than five years, buying a combined 14,558 shares worth $652K. |

TLDR: Celsius is dealing with short-term noise and one-time charges, but the core business is still growing rapidly and gaining share. The pullback appears more sentiment-driven than fundamental, and the current valuation offers a solid risk/reward. A stronger PepsiCo partnership supports long-term upside if execution remains solid. |

My Take: I have initiated a small (<5%) exploratory position, given that this is not a wide-moat compounder. That said, I do see a credible long-term thesis with strong growth prospects, and this could evolve into a larger position over time if execution remains strong and its moat continues to widen. I am also a fan of the energy drink. |

|

Want to see the rest of the list? |

|

|

Disclaimer |

This content is for informational and educational purposes only and should not be construed as financial, investment, tax, legal, or other professional advice. It does not constitute a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. You are solely responsible for any investment decisions you make, and you should consult with a qualified financial advisor before making any investment or financial decisions. |

The author may hold, or may in the future acquire, sell, or otherwise change positions, long or short, in any of the securities, investments, or financial instruments mentioned in this content, without notice or obligation to update this information. Any such holdings or transactions should not be construed as an endorsement of any security or strategy. |

The author and publisher make no representations or warranties, express or implied, as to the accuracy, completeness, or timeliness of the information provided, and assume no liability for any losses or damages of any kind arising from or related to the use of this content. Past performance is not indicative of future results. This report contains forward-looking statements that reflect current expectations and are subject to risks and uncertainties that may cause actual results to differ. All investments carry risk, including the potential loss of principal. |

This content is intended for a general audience and may not be lawful or appropriate in certain jurisdictions. Readers are responsible for ensuring compliance with all applicable laws and regulations in their country or region. |

This report was optimized using AI for clarity, structure, and conciseness. AI tools also assisted in research organization, idea generation, and analytical stress testing. All analysis, conclusions, and opinions remain the author's own. |

This newsletter is sponsored by Elf Labs. Sponsorship does not influence our editorial content. We do not endorse the sponsor's products, services, or views, and we are not responsible or liable for any interaction or transaction between readers and the sponsor. |

Tidak ada komentar:

Posting Komentar