In partnership with |  |

|

|

5 Investment Ideas - October 2025 |

Welcome to the October edition of Investment Ideas. |

Each month, I spotlight a select mix of businesses I am following closely. |

This edition highlights companies navigating turnarounds or near-term challenges, alongside durable operators that appear fairly valued but underappreciated. |

As a reminder, this report is concise by design. |

It does not capture every risk in full but highlights the key dynamics shaping each business and why they merit close attention. |

Let's dive in. |

Note: This report is for informational purposes only and is not investment advice. Please see the full disclaimer at the end. |

|

|

When Thor Speaks, Investors Pay Attention |

|

Topgolf revolutionized golf by turning it into a social, tech-driven game for anyone. And they've made billions in annual revenue doing it. Surf Lakes is applying that same model to surfing, and investors can still join them until 10/30 at 11:59 PM PT. |

This is a paid advertisement for Surf Lakes' Regulation CF offering. Please read the offering circular at https://invest.surflakes.com |

|

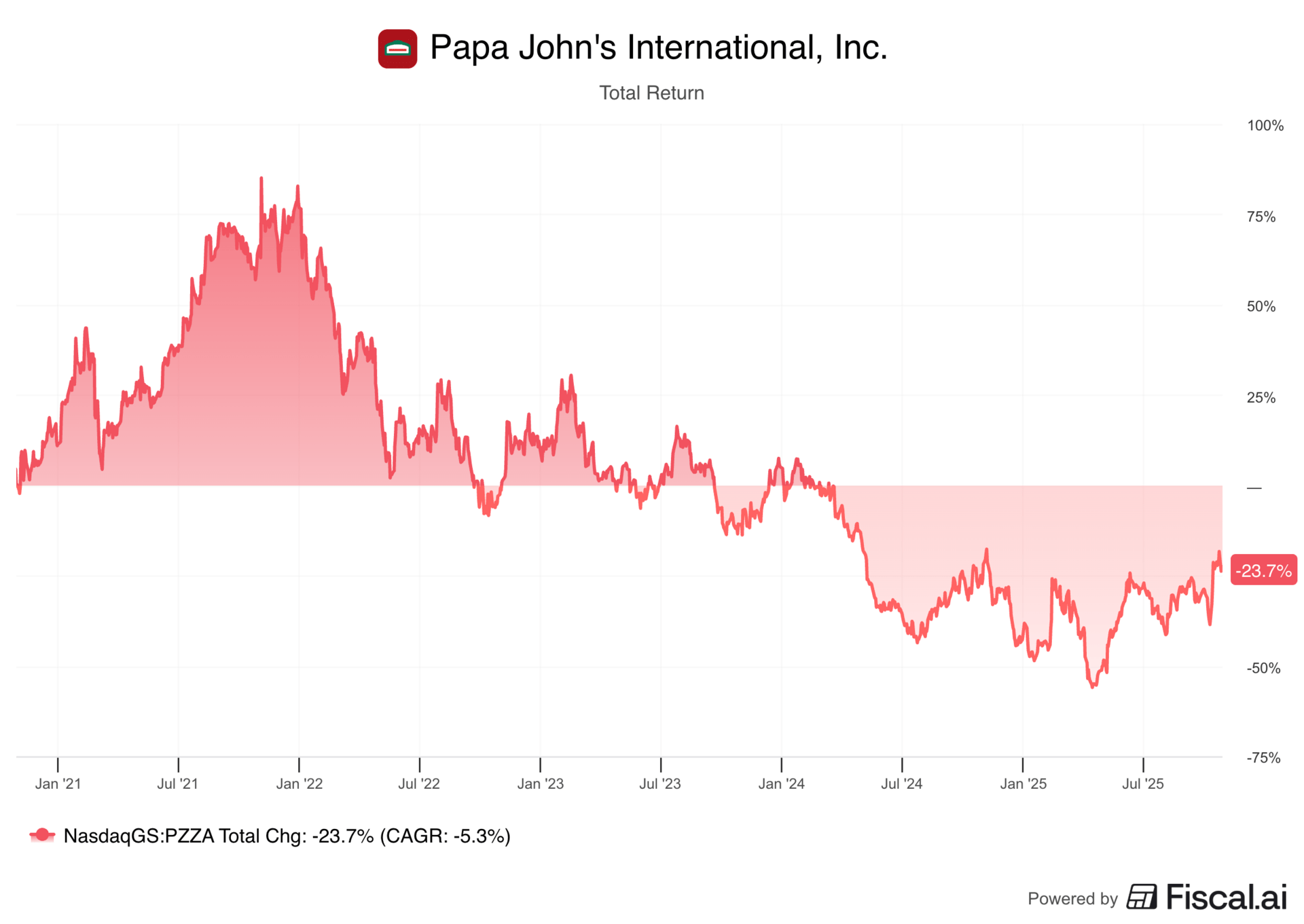

5/ Papa John's International |

Ticker: $PZZA Market Cap: $1.7B

|

|

Papa John's, founded in 1984 and based in Kentucky, operates and franchises pizza delivery and carryout restaurants across more than 50 countries. |

The company manages a mix of company-owned and franchised stores under its core brand, supported by regional commissaries that supply dough and ingredients to franchisees. |

Key Metrics: |

|

Outlook (Estimates): |

Forward 2Y Revenue CAGR: 1.7% Forward 2Y EPS CAGR: -2.8% Long Term EPS Growth: 6.6%

|

Recent Developments & Key Headwinds: |

1/ Acquisition Rumors — Reuters reported that Apollo Global Management submitted a new bid to take Papa John's private at $64 per share just a few weeks ago, up from a prior joint offer with Qatari-backed Irth Capital Management at $60 per share in June. Multiple activist investors have also reportedly shown interest in the company, which could lead to strategic changes or additional takeover interest. |

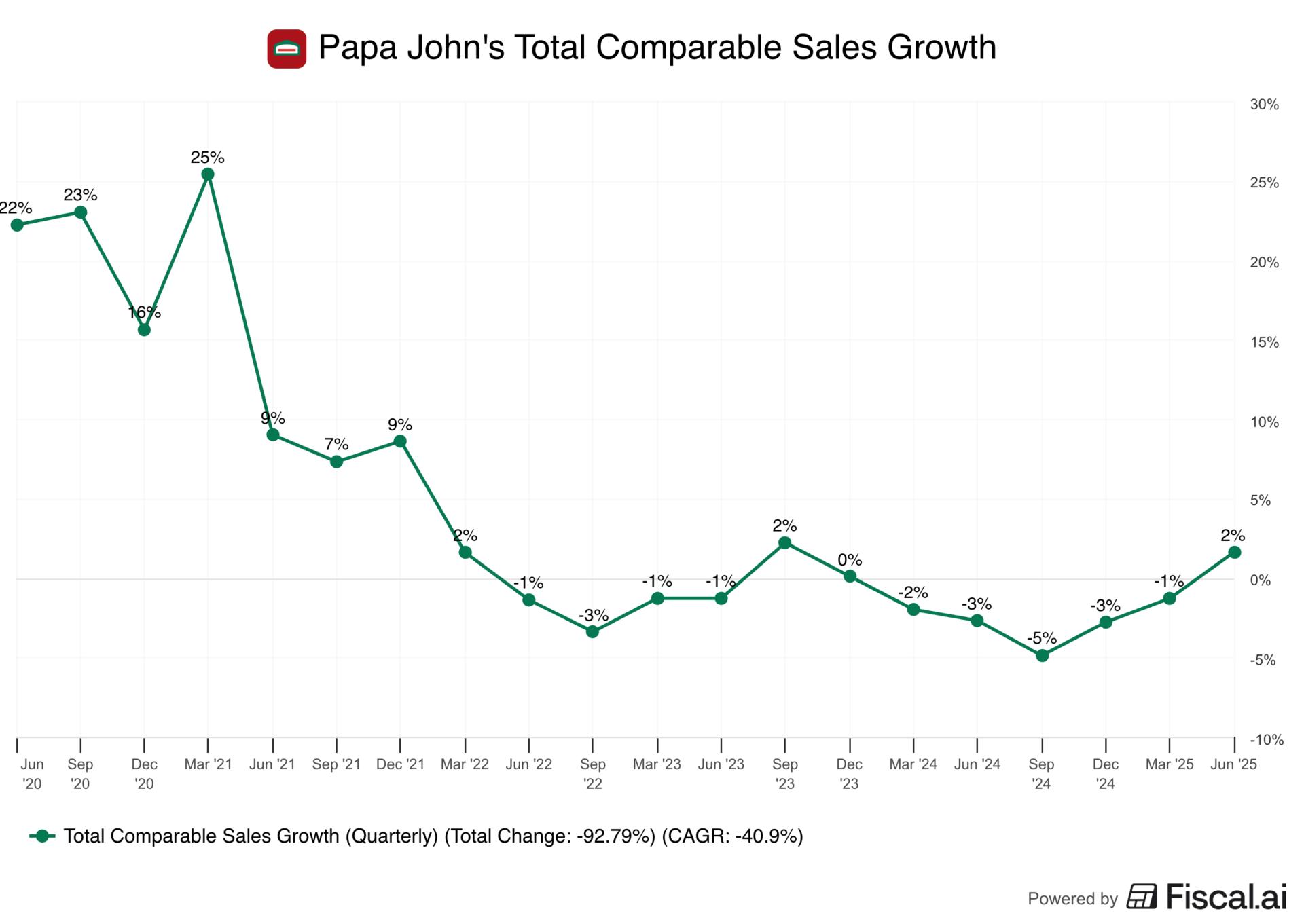

2/ Prolonged Sales Weakness — After strong growth during the pandemic, comparable-store sales have since declined in nine of the last twelve quarters, with one flat and only two showing growth. The company's complex menu, inconsistent pricing, and lack of value positioning have hurt demand amid inflationary pressures, while competitors like Domino's continue to maintain steady sales growth due to greater scale and operational efficiency. |

3/ Leadership Turnover and Brand Legacy Issues — Founder John Schnatter's 2018 controversy, which included racially insensitive remarks and public disputes with the board, damaged brand perception. The incident initiated a series of executive turnovers, with Todd Penegor taking over as CEO in August 2024 to lead stabilization efforts. |

|

Why This Might Be An Opportunity: |

1/ Buyout Upside — An Apollo-led buyout would represent roughly a 25% upside from the current stock price if completed. A higher bid could deliver even greater returns, while the entrance of a major activist could still drive operational changes and accelerate a turnaround if no deal materializes. |

2/ Private Equity Appetite — Private equity firms have been active in acquiring and restructuring restaurant chains. These include Subway, Tropical Smoothie Cafe, Dave's Hot Chicken, and Jersey Mike's. Even large brands like Burger King were taken private in 2010 before later merging under RBI. Papa John's could fit this pattern, with strong brand recognition and room for margin enhancement under private ownership. |

3/ Operational Turnaround In Motion — Management has launched a five-priority plan focused on product quality, pricing balance, marketing, technology, and supply chain efficiency. In the most recent quarter, North America returned to 1% positive comparable sales and international markets rose 4%. Additionally, since late 2014, 2.7M new members have joined the loyalty program. Planned supply chain optimizations are expected to lift margins by at least 1 percentage point by 2028, laying groundwork for improved profitability. |

TLDR: Papa John's remains a turnaround story with ongoing sales and operational challenges. While longer-term fundamentals could improve over time, renewed private equity interest and activist pressure have created a near-term, event-driven setup for investors seeking buyout-style opportunities. |

|

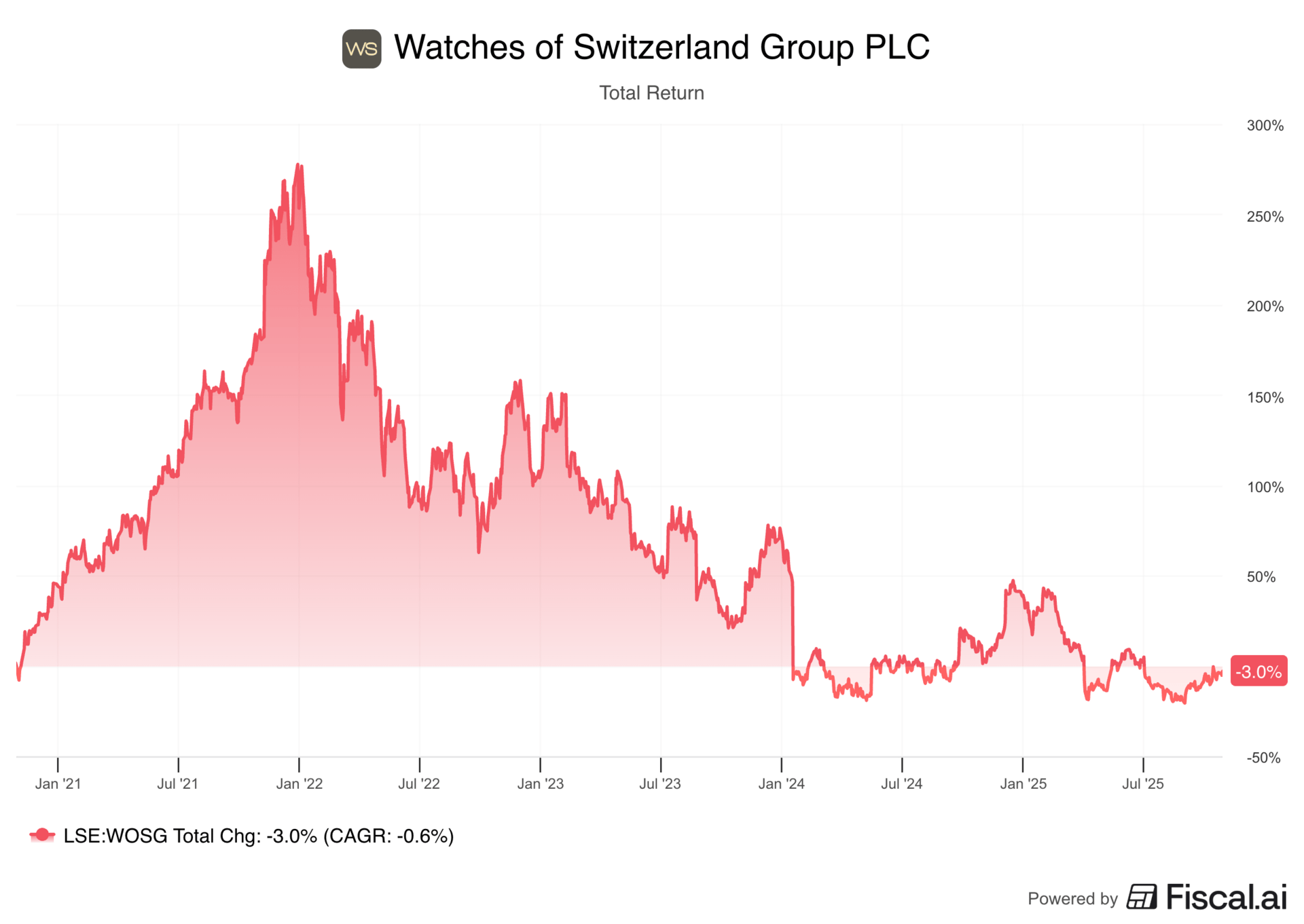

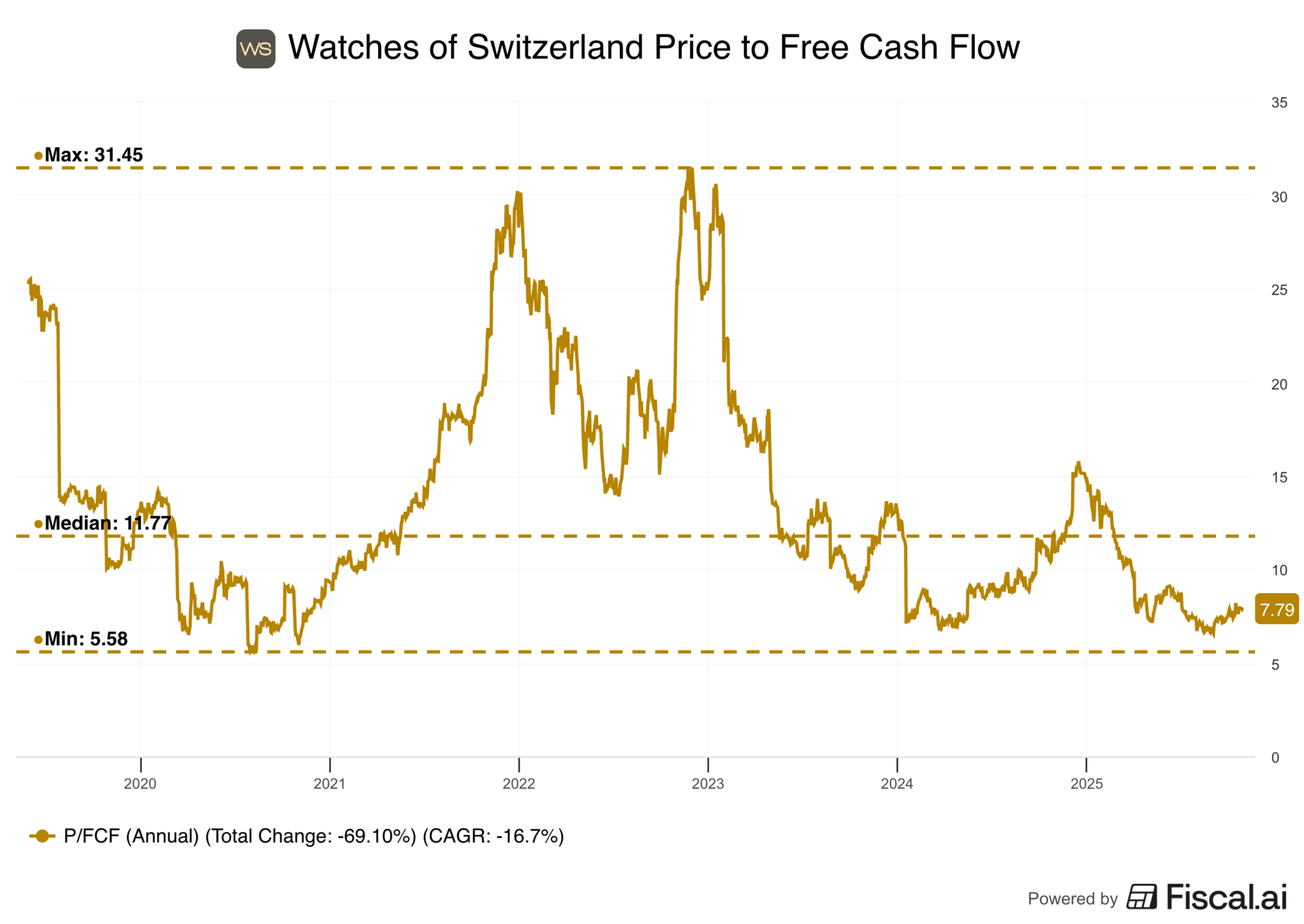

4/ Watches of Switzerland Group |

Ticker: $WOSGF Market Cap: $1.2B

|

|

Watches of Switzerland, founded in 1924 and based in the United Kingdom, is a leading luxury watch and jewelry retailer operating across the U.K. and the U.S. |

The company runs nearly 200 showrooms in the U.K. and U.S., and is known for its close partnerships with Rolex, Patek Philippe, and Audemars Piguet. |

This idea was brought to my attention by my friend Compounding Quality. I definitely recommend you check out his work! |

Key Metrics: |

|

Outlook (Estimates): |

Forward 2Y Revenue CAGR: 5.1% Forward 2Y EPS CAGR: 2.8% Long Term EPS Growth: 4.2%

|

Recent Developments & Key Headwinds: |

1/ Post Pandemic Slowdown — The luxury market surged during the pandemic but cooled sharply as inflation rose and interest rates reached decade highs in the U.S. and U.K. Consumer spending has since tightened, pressuring discretionary categories such as watches and jewelry. The U.S. market has held up better, while the U.K. continues to experience softer demand. |

2/ Rolex's Acquisition of Bucherer — Rolex's 2023 acquisition of retailer Bucherer raised concerns that the watchmaker could move toward vertical integration, potentially squeezing out partners like Watches of Switzerland and putting them in direct competition. Investors also worry Rolex may grant Bucherer preferential access to high-demand models, which could weaken Watches of Switzerland's product allocation, overall appeal to collectors, and distribution exclusivity. |

3/ Macroeconomic Pressure — The U.S. imposed a 10% baseline tariff on imported Swiss goods in April 2025 and raised it to 39% in August. Watches of Switzerland had guided assuming a 10% rate would persist, meaning the higher tariff introduces additional margin pressure and potential guidance risk if extended. The company currently expects its fiscal 2026 EBIT margin to decline by up to 100 basis points from 9.1% in fiscal 2025, reflecting the near-term impact. Tariffs are a continuing headwind for the broader Swiss watch industry and could impact the company if further hikes ensue or last longer than expected. |

|

Why This Might Be An Opportunity: |

1/ Sector Wide Reset — The luxury market's weakness has been broad, with names like LVMH and Kering also seeing slower demand. However, in a September trading update, Watches of Switzerland recently noted that the U.K. market has stabilized near pre-COVID growth trends, while U.S. performance remains resilient. |

2/ Exposure To The Highest-End Consumer — Luxury watch buyers tend to be more insulated from macro headwinds, with average purchase prices often exceeding $10,000. This positions Watches of Switzerland within a more resilient segment of the luxury market. The group continues to invest and expand flagship locations, including a Rolex boutique on Old Bond Street, London, a Patek Philippe salon in Greenwich, Connecticut, and an Audemars Piguet House in Manchester, reinforcing brand positioning and customer experience. |

3/ Guidance Maintained — Despite the tariff escalation, Watches of Switzerland recently reiterated its fiscal 2026 guidance for 6%–10% constant-currency revenue growth, signaling confidence in near-term performance. The company doesn't expect a material impact from tariffs in the first half of fiscal 2026, supported by inventory front-loading and strong brand relationships. Moreover, tariff discussions and recent trade frameworks offer potential for policy relief, leaving room for a more constructive medium-term outlook. |

4/ Partnership Stability With Rolex — Watches of Switzerland has maintained a century-long partnership with Rolex, dating back to 1919. Following the Bucherer acquisition, Rolex emphasized that Bucherer would operate independently and that its broader retail partnerships remain unchanged. The decision was reportedly driven by succession planning rather than competitive strategy, suggesting continuity rather than disruption in Rolex's retail relationships. |

TLDR: Watches of Switzerland serves as a pure-play proxy for Rolex and the broader luxury watch market. Despite tariff pressures and softer demand, the company reaffirmed guidance and continues to expand its flagship network. With shares down sharply and trading at just 8x TTM free cash flow, valuation looks undemanding for investors seeking exposure to a resilient, brand-backed segment of the luxury space. |

|

Want to see the rest of the list? |

|

|

Disclaimer |

This content is for informational and educational purposes only and should not be construed as financial, investment, tax, legal, or other professional advice. It does not constitute a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments. You are solely responsible for any investment decisions you make, and you should consult with a qualified financial advisor before making any investment or financial decisions. |

The author may hold, or may in the future acquire, sell, or otherwise change positions, long or short, in any of the securities, investments, or financial instruments mentioned in this content, without notice or obligation to update this information. Any such holdings or transactions should not be construed as an endorsement of any security or strategy. |

The author and publisher make no representations or warranties, express or implied, as to the accuracy, completeness, or timeliness of the information provided, and assume no liability for any losses or damages of any kind arising from or related to the use of this content. Past performance is not indicative of future results. This report contains forward-looking statements that reflect current expectations and are subject to risks and uncertainties that may cause actual results to differ. All investments carry risk, including the potential loss of principal. |

This content is intended for a general audience and may not be lawful or appropriate in certain jurisdictions. Readers are responsible for ensuring compliance with all applicable laws and regulations in their country or region. |

This report was optimized using AI for clarity, structure, and conciseness. AI tools also assisted in research organization, idea generation, and analytical stress testing. All analysis, conclusions, and opinions remain the author's own. |

Tidak ada komentar:

Posting Komentar