January 21, 2025

Generate Income the Utilitarian Way

Dear Subscriber,

|

| By Gavin Magor |

Investors are nervous about the future.

That’s not just my opinion. It’s also what the “investor fear gauge” — the CBOE Volatility Index — is showing us.

The VIX is at a three-week high because of things like:

- Geopolitical tensions — despite the temporary ceasefire in the Middle East …

- The potential tariffs, maybe even a trade war …

- Even the growing federal deficit.

All of these are sending long-dated bonds lower and their yields higher.

Last week, the 10-year Treasury yield hit its 14-month high. It’s since retreated a few basis points.

But the largest uncertainty of all, at least among investors, might just be the future of rate cuts.

Almost from the minute the Fed first cut rates by 50 basis points in September, investors have been trying to guess the size and timing of the next one.

Recently, those same investors are concluding that they won’t be coming fast enough or large enough.

That could tip in a hurry, however. Any kind of economic shock, problem in the banking system or other unforeseeable roadblock in the market could send the Fed scrambling to pick up the slack and make deeper, faster cuts.

Smart investors will need to have a plan in place if rates come down in a hurry. Here’s why that’s more important than ever …

The Generational Cost of Low Rates

When the Federal Reserve finally lowers rates, many people will feel a big relief.

You can’t blame them. They can’t wait for a return to cheap, easy money — something they grew accustomed to in the decade following The Great Recession in 2007-2008.

10-Year Treasury yield (2007-present).

Source: CNBC.

Click here to see full-sized image.

But not everyone will be relieved.

In fact, the 76.4 million baby boomers living in the U.S., the largest demographic group, face a large challenge.

Low interest rates might be great for the 55-and-unders still working and able to grow their wealth aggressively.

But for seniors charged with safely generating monthly income from investments, collecting interest from savings accounts or CDs or looking for high-yielding bonds … low rates can derail retirement plans in the blink of an eye.

Traditional fixed-income investments in a low-rate climate simply can’t meet the needs of everyone planning for or wanting to stay in retirement.

Estimates vary, but T. Rowe Price suggests that people looking to retire at age 65 should have saved between 7.5x and 13.5x their pre-retirement income.

That’s a tall order. So, it generates monthly income to pay living expenses and preserve wealth.

That’s why interest rates and yields are so important in our later years.

Today, the national average for CD rates is higher than in years past (as high as 7.20% in mid-2024) but is starting to fall. The average 12-month CD earns around 4% today, according to FDIC data.

However, it can get much worse. In June 2013, CD yields hit historic lows. One-year and five-year CDs paid a pitiful 0.24% and 0.77%, respectively, according to Bankrate.

That happened, you guessed it, during that decade-long crusade to keep rates near zero and stimulate the economy after the Great Recession.

So, the number of good investments in a low-interest rate climate shrinks for baby boomers as traditional tools offer less upside.

But the good news is that one sector that has been out of favor for nearly a decade is showing signs of life.

The Alternative to Fixed Income

That sector is utilities.

To understand why utilities are starting to show signs of life again, let’s look closer at the relationship between them and interest rates.

Historically, utility stock prices and the 10-year Treasury yield have tended to have an inverse relationship.

So, when interest rates rise, utility stock prices tend to move down, and vice versa. Although, there have been exceptions to this.

In 2023, rising interest rates negatively influenced utility stocks as many investors turned to high-yielding bonds and dividend-paying stocks that paid more.

As a result of the huge rise in rates over the past two years, utilities are priced very attractively.

When the Fed cut rates after the subprime crisis (2008) to stimulate the economy, investors flocked to utilities for safety and income.

In fact, “utes” as a sector have, on average, outperformed in the six- and 12-month periods following the end of the last five Fed tightening cycles.

There is no reason why history will not repeat itself. While the sector ended in the red by 7.17% in 2023, as measured by the Utilities SPDR (XLU), it bounced back last year with a 23.28% gain.

Utility stocks’ dividends are dependable and consistent. And for savers and retirement-age investors, “utes” provide steady income.

On top of that, we’re seeing big increases in electricity demand generally expected from the electrification of buildings and transportation, a good U.S. economy, crypto mining and especially energy-hogging AI models.

A recent estimate by ICF is that after decades of little to no growth in electricity demand in the U.S., it is expected to increase by 9% by 2028.

With the tailwinds of lower interest rates combined with AI and the demand for electricity, the sector could offer a unique investment option for baby boomers.

XLU is a great ETF with a 2.9% quarterly yield. It offers simple, low-cost exposure to 34 S&P 500 utility stocks, with a relatively low expense ratio of 0.09%.

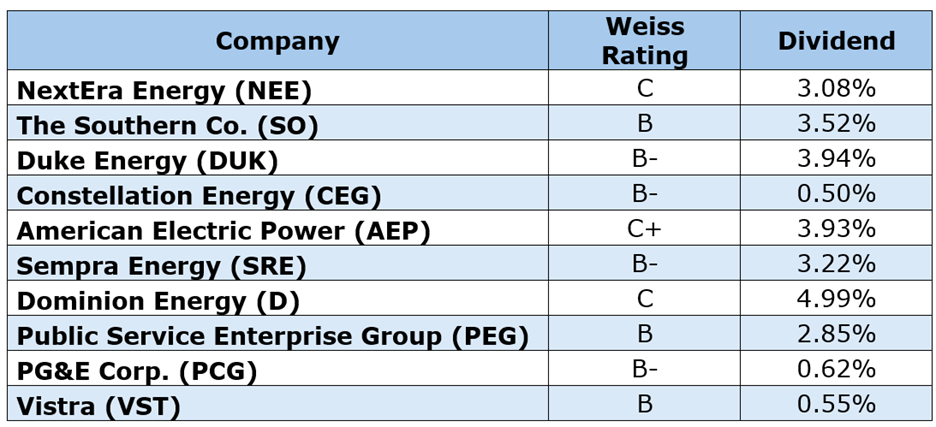

Its top assets, which comprise 60% of the ETF, include some of the companies best positioned for the boom in energy demand.

While the XLU experienced a 10% pullback to start the year after hitting a new 52-week-high last November — likely profit-taking — I see it as a good buying opportunity.

As such, income investors are likely to enjoy decent dividends and growth in utilities as a part of a diversified portfolio.

Cheers!

Gavin

P.S. Another way for investors of all ages to boost their income is to check out what my colleague, Marija Matić, calls “Supersized Crypto Royalties.” Check them out here.

Tidak ada komentar:

Posting Komentar