January 16, 2025

California Disaster Adds Fuel to the Insurance Firestorm

Dear Subscriber,

|

| By Gavin Magor |

Multiple wildfires raged across California over the past week.

Some 12,300 structures were destroyed across 44,000 acres in Greater Los Angeles.

Two dozen people have been confirmed dead. Another two dozen are still believed to be missing.

The estimated loss is $135 billion to $150 billion in total damage and economic loss for the region.

For the hundreds of thousands of LA residents who evacuated or are in evacuation zones, this nightmare is far from over.

Even though the fires are mostly contained, the Santa Ana winds could prolong these deadly blazes for another few days.

And for those with unimaginable losses, there is no guarantee their insurance policies will be able to provide the renumeration — at least, financially — they need.

Nothing Natural About

Life After Disasters

My heart goes out to everyone on the West Coast. Having just moments’ notice to evacuate … and a potential lifetime of dealing with the losses … is a challenge I wouldn’t wish on anyone.

Where I live in South Florida, we can generally plan for hurricane season and make reasonable preparations.

And, while the weather seems to grow more severe every year, I know for a fact that the situation is bordering on dire for homeowners. And, unfortunately, many of the insurers in the most disaster-prone regions are making recovery nearly impossible.

That’s why we’re making even more data available on the Weiss Ratings website: So, you won’t be blindsided by your insurance company.

Like many of my peers here at Weiss Ratings, I live in the Sunshine State. As a state prone to catastrophic natural disasters, residents rely on their insurance companies.

Without their financial support after hurricanes, floods, tornadoes, fire and earthquakes strike, homeowners who suffer damage must use their own hard-earned money to repair or fix homes or property. For many, that’s not feasible.

Besides, that’s the very reason we pay our premiums: To ensure that — should we suffer such devastation — we won’t have to worry about financial challenges … or at least the bulk of them.

Over the past few years, more than 30 insurers stopped doing business in my state.

Many others simply stopped writing new policies, jacked up premiums to make them largely unaffordable, filed for bankruptcy or … simply denied perfectly legitimate claims.

That’s right. They just don’t pay. And people like you, the policyholder, suffer.

As the nation’s only independent insurance company rating agency, Weiss considers itself an industry watchdog.

That means, unlike many others, we don’t take money from any sources in exchange for a favorable rating.

And, as such, we have no problem whatsoever with spilling the beans on those companies that deny more than their fair share of claims.

You read that right.

After being battered by hurricane after hurricane and paying high premiums month after month, many Floridians with legitimate claims are getting stiffed by their property insurers.

And this very bad habit is spreading nationwide. It is already a problem in Texas and, yes, California, too.

You might be wondering why you haven’t heard about this before.

Well, the information is available to the public, but it's been virtually impossible for policyholders to acquire it from either the companies or their regulators.

Until now.

You can go straight to Weiss Ratings to learn how often your property insurance company denied homeowners’ claims they closed in the most recently reported year.

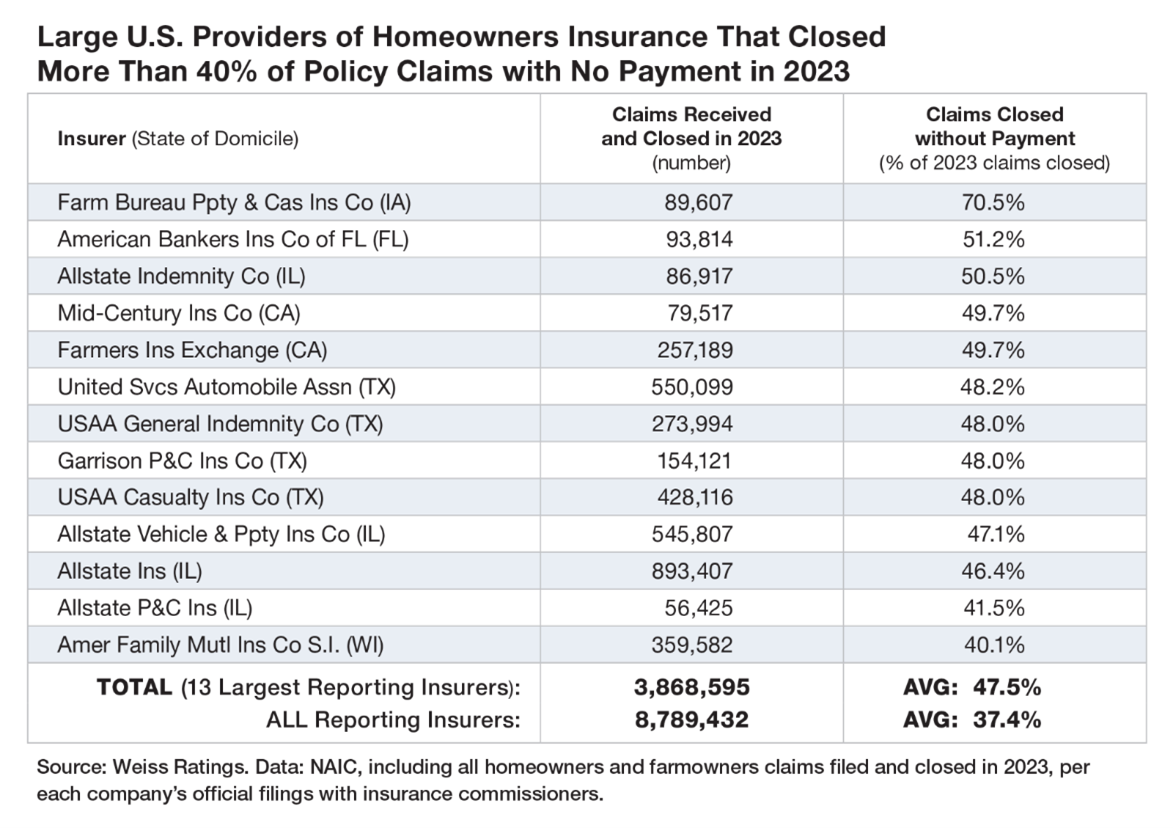

Among those that received and closed 50,000 or more homeowners’ and farm owners’ claims last year, Farm Bureau Property & Casualty Insurance Company (domiciled in Iowa) denied 70.5% of claims with no payment … American Bankers Insurance Company (FL) denied 51.2% and … Allstate Indemnity Company (IL) denied 50.5%.

The nation's largest providers — each with hundreds of thousands of homeowners’ claims closed last year — made zero payments on nearly half of their claims:

- Farmers Insurance Exchange (CA) closed 257,189 homeowners claims in 2023 and denied payment on 49.7%.

- United Services Automobile Association (TX) closed 550,099 and denied 48.2%.

- USAA General Indemnity Company (TX) closed 273,994 claims and denied 48%.

- USAA Casualty Insurance Company (TX) closed 428,116 and denied 48%.

- Allstate Vehicle & Property Insurance Company (IL) closed 545,807 and denied 47.1%.

In total, 13 large providers closed 3.9 million homeowners’ claims, denying any payment on 47.5%.

Meanwhile, including all reporting companies, 8.8 million homeowner claims were closed in 2023. And of those, 37.4% were denied payment, up from 24.9% in 2004.

If you’re thinking this is just the norm, there’s nothing normal about these high denial rates.

They've been creeping up steadily for nearly two decades and have now reached alarming levels.

Here’s How to Protect Yourself

My friend, colleague and founder of Weiss Ratings, Dr. Martin Weiss, believes the new trend is probably an effort to offset the surging costs of storms, floods and forest fires.

He suggested that instead of maintaining adequate reserves to cover the likely potential damage, many insurers distribute the funds to shareholders or move them to other subsidiaries.

Now, to make ends meet, these companies are closing about half of homeowner claims with no payment whatsoever.

However, our fight to bring the insurance crisis to an end and make people aware of their provider’s business practices … and raise red flags when appropriate.

You can click here for the full list of insurance companies that closed claims to learn how often your property insurance company denied homeowners’ claims they closed in 2023.

It’s free and available to anyone today but not for too much longer.

Cheers!

Gavin Magor

P.S. Rising premium rates and having claims denied puts pressure on everyone’s wallet. Finding alternative streams of income is more and more paramount.

I urge you to view this special presentation on exactly that. The source might be unexpected. But the income and yields are very much game changing. Check it out here.

Tidak ada komentar:

Posting Komentar