June 26, 2024

How to Play the Housing Bottleneck

Dear Subscriber,

|

| By Sean Brodrick |

The latest housing data is in, and it’s not pretty.

May is usually the best season for buying and selling houses. But not this year.

Fewer existing homes were sold last month than in April.

And sales were down 2.8% from a year ago, according to the National Association of Realtors.

Why? Well, one reason is that tight supply means prices keep going up.

U.S. home prices hit an all-time high in May, as the median home price nationwide jumped 5.8% from the prior year. The median home price across the U.S. was $419,300 in May, up from $396,500 in May 2023.

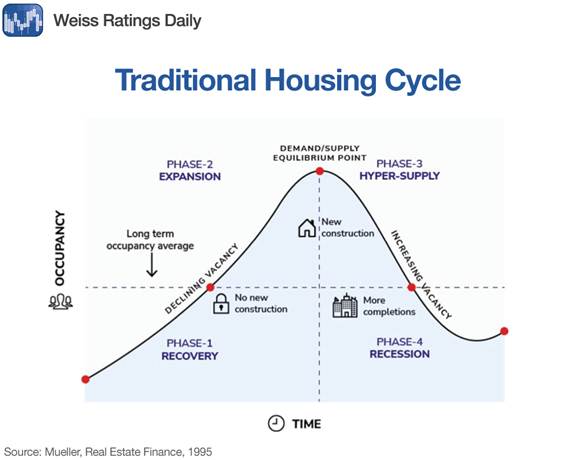

There’s also the 18-year housing cycle in play.

I pay close attention to cycles because they can really help you make sense out of things that can appear truly nonsensical on the surface.

The latest housing cycle started in 2012. That means we are more than halfway through it.

Each property cycle has four phases: recovery, expansion, hypersupply and recession.

Knowing how to spot … and ride … these cycles can really help you keep emotions at bay while boosting your profit potential along the way.

That’s true even when some anomalies are in play, like there are right now.

After years of rising prices and declining vacancies, America should be past the peak of the traditional housing cycle.

Yet even though we are clearly in the “increasing vacancy” part of the above chart, supply remains skintight.

How tight?

According to data from online realtor Zillow (ZG), the U.S. is now short 4.5 million homes.

Here’s the really crazy part …

Despite the supply shortage, homebuilding in May actually fell to its slowest pace in four years.

This is due to higher interest rates — more on that in a bit — labor shortages and zoning restrictions that put the brakes on multifamily construction.

The crux of any housing market is supply and demand. And the worsening housing deficit is a significant cause of the housing affordability crisis.

Zillow says that only 15.1% of American households that don’t currently own a home can afford a typical mortgage.

Along with not having enough homes built, higher-for-longer interest rates make home prices unaffordable to many Americans.

The average interest rate for a 30-year fixed mortgage hit 7.37% on Tuesday. That’s down slightly from last month. But it’s still too damned high.

The Fed has shown it’s in no rush to lower interest rates. It has hinted at one rate cut this year, and it would take an economic slowdown to get more rate cuts, faster. So, it seems like homebuyers are stuck between a rock and a hard place.

Uncle Sam’s Financing Spree

Can Uncle Sam change that?

During the pandemic, the U.S. Treasury injected $8.57 billion into community lenders, who, in turn, invested $1.2 billion in 433 affordable housing projects.

And then on Monday, U.S. Treasury Secretary Janet Yellen announced $100 million to finance potentially “thousands” of affordable housing projects over the next three years.

But will it be enough?

Sure, the right investments can push around any cycle. But the U.S. housing market is worth a whopping $47 TRILLION!

The sheer size of the market makes Yellen’s efforts look like a burp trying to push around a hurricane.

Neither major political party has a short-term solution for this crisis.

Steps like the one Sec. Yellen is taking will take years to play out when people are clamoring for affordable housing NOW!

How You Can Play It

If we see more govt investing in housing, or lower interest rates — or both — then we get more homebuilding activity.

States are already investing in housing. The Fed seems to be moving toward housing investment on a grander scale. And that could give builders a boost. But even if the politicians don't get it right, lower interest rates could still provide that boost.

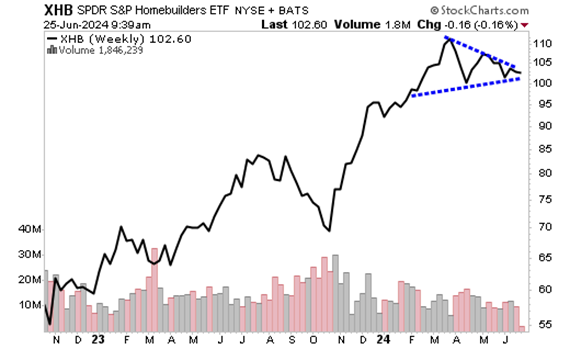

There are ETFs that will let you potentially profit from that investment. The one I like the most is the SPDR S&P Homebuilders ETF (XHB).

XHB has an expense ratio of 0.35% and a dividend yield of 0.69%.

It uses an equal-weight, blended strategy with a mix of growth and value stocks. The fund invests in home builders, building product suppliers and home improvement retailers.

Its biggest holdings are KB Homes (KBH), Carlisle Companies (CSL) and Home Depot (HD). Here’s a weekly chart …

You can see that XHB has been consolidating since April. It’s probably coiling up for a big move. But in which direction?

With the housing market as tight as it is, I believe the next move could be higher … to $150 or more.

From XHB’s current price of $100 and change, that could represent almost a 50% increase from here.

All the best,

Sean

P.S. While higher-for-longer interest rates might be making fixed-income investments seem more attractive than they’ve been at any time this century, there’s more to the story.

In fact, as we recently laid out, there’s another “keep-safe” opportunity at high yields. So high, it’s almost unfathomable.

Right now, there’s a “keep-safe fund” that is paying a 17% yield. That’s nearly 12x more than banks are paying on the average 5-year CD.

Click here to find out more about this and other high-yielding “keep-safe funds.” But hurry, we’ll be pulling down this presentation tomorrow.

Tidak ada komentar:

Posting Komentar